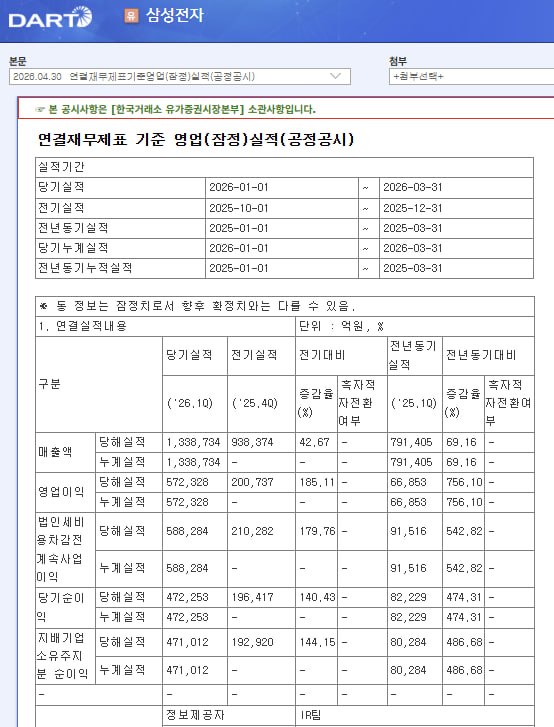

@crux_capital_ @boymanrobshit I agree but on the other hand it’s far from being the craziest valuation in the semis and photonics space. Look at cohr and lite at 300+ fw earnings? Does that make sense either? But they both keep going up….the whole market is a bit insane

English