ทวีตที่ปักหมุด

$MSTR Investment Thesis: Outsiders in Corporate Finance

Bitcoin is sitting around $100,000 in 2025 and now $80,000. Two things are holding it back:

1. First, people are scared we’re already in the post-halving bear phase. Some old-timers and retail folks are selling. That pressure is mostly getting soaked up by the Bitcoin treasury companies (like $MSTR) and the ETFs, so supply and demand are roughly in balance.

2. The whole market is nervous. AI bubble fears, quantum computing worries, trade wars, a deadlocked Congress, falling savings rates, slowing global growth, everything makes people hug cash and bonds. Bitcoin is the first thing they dump when they need liquidity because it trades 24/7.

Now to MicroStrategy ($MSTR):The stock is correcting hard for two simple reasons:

1. The crowd has decided it should trade at 1× net asset value or less. Right now it’s around below 1, so the trade of the moment is long Bitcoin / short MSTR. Price drives narrative.

2. A bunch of smaller copy-cat treasury companies have blown up — some down 90%+. Guilt by association drags $MSTR down too. ( $NAKA , $MTPL)

The drop isn’t coming from the fundamentals of the business. It’s the market re-pricing the whole “Bitcoin treasury” model. This is a brand-new industry. It’s immature. The market hasn’t figured out yet what multiple these companies deserve. That will take 3-5 years IMO, this train goes fast.

On the right multiple (MNav):

The “correct” MNav will swing with sentiment. Over the last four years we’ve seen it below 1× and above 3×. One thing is clear: the higher the BTC Yield and global liquidity, the higher the multiple tends to go. In 2025 the yield is already 27% year-to-date and guidance is for ~30%. Saying it must always be 1× is wrong. When you buy the stock you’re buying a claim on a growing pile of Bitcoin per share. That’s real shareholder value. Once the debt is gone in 2029 and they’re running a clean, consistent BTC yield with no leverage, a lot of the debate dies. Until then, fair enough, people worry about management risk, lack of long track record, Michael Saylor is crazy, etc.

The market also pays big premiums for unique businesses with no real competition and near-zero customer churn. Look at Palantir ( $PLTR) trading 200-300× free cash flow. Shorting it makes no sense because the cash flows are visible for decades and they have a quasi-monopoly. (Disclaimer: I’ve never owned $PLTR.)

$MSTR is similar. Yes, copycats exist, but they’re tiny. $MSTR will own the Bitcoin-backed credit market. Not the banks. That monopoly-like position will command a premium >1× we just don’t know exactly how big yet.

What MicroStrategy is actually doing:

Their whole game is to deliver BTC Yield to shareholders. They raise capital two main ways:

1. Regular share ATMs when MNav >1 (opportunistic, not permanent. You can’t forever sell a dollar for three, but you take the gift when the market gives it).

2. Preferred share ATMs, this one is structural and perpetual. It is not debt, it is equity.

They raise money, buy Bitcoin, pay roughly 10% interest + conversion features on the preferreds. As long as Bitcoin compounds >10% a year, the spread between Bitcoin’s return and the cost of capital is pure accretive BTC Yield for common shareholders. This is not some wild invention. It’s the same thing mature vehicles have done forever:

- BlackRock $BLK raises money through ETFs, buys the underlying assets, clips a fee.

- REITs issue preferreds/debt, buy buildings, pay dividends, keep the spread.

- Berkshire ( $BRK) or Brookfield ( $BAM, $BN) uses insurance float, invests it, keeps the profit.

Same product, different wrapper.

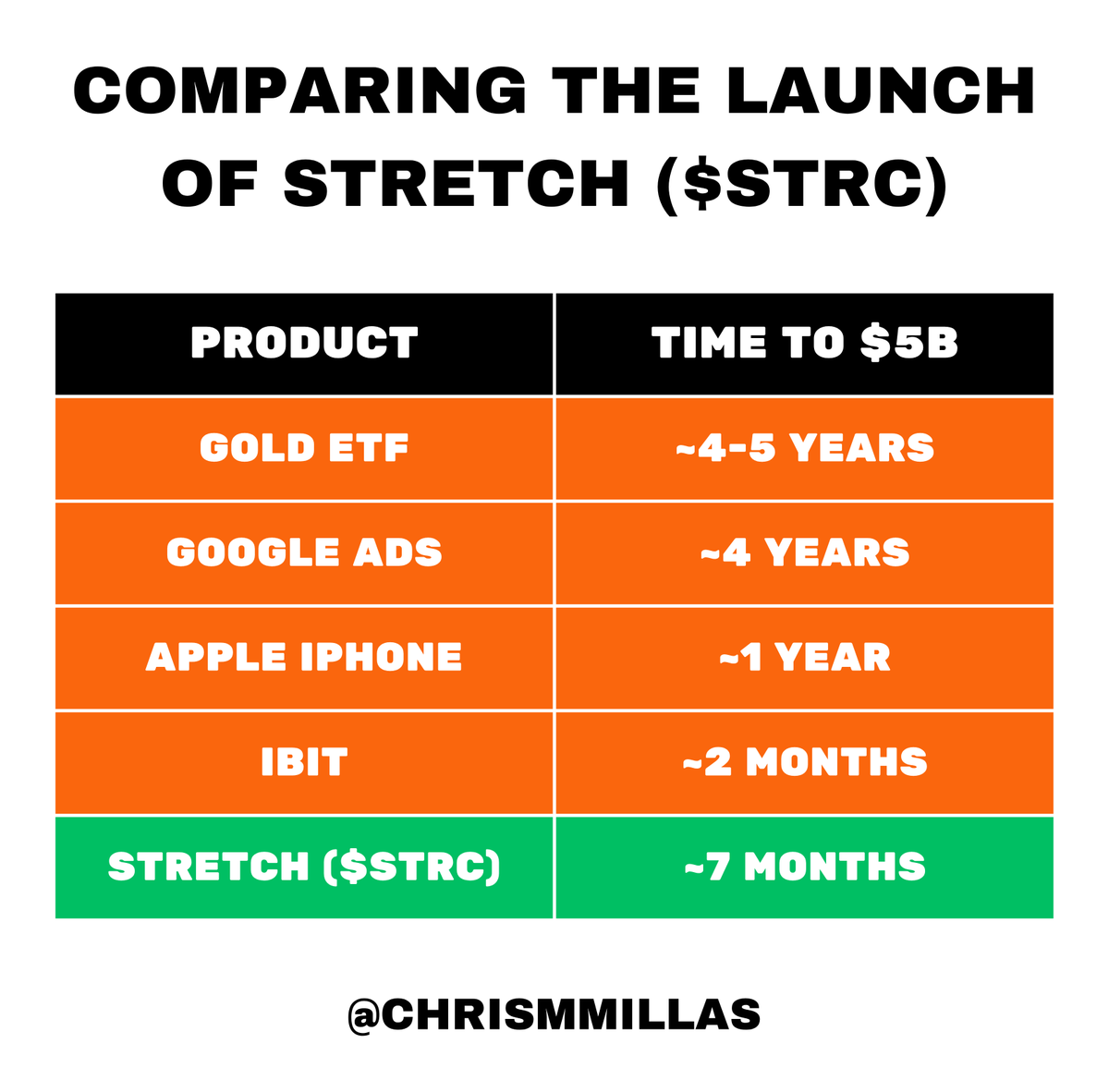

The star product right now: $STRC preferreds

Fully over-collateralized (5×+ assets), pays 2-3× what money-market funds or bonds do, fixed-income style return with no volatility for the holder.

Target customer: retail and institutions who want yield and liquidity but hate price swings. In 2025 they’re already pulling in ~$30 million a week just from $STRC. They’re getting S&P credit ratings on these so institutions can actually buy them. Two clever twists:

1. Floating coupon. If rates drop to 5-6%, they can still issue tons more.

2. One-click issuance through ATM: no branch network, no army of bankers. Fast and easy.

My base case:

$100 million a week from $STRC alone by late 2025, maybe $500 million a week in 3-4 years. That’s real scale, built with six people in an office. The preferred already trades steady around par (90$-100$) and ignores Bitcoin or MSTR stock moves. That is a proof that a conservative, Bitcoin-agnostic buyer is showing up.

Long-term picture:

A few things I think are close to certainties:

- Starting around 2028 MSTR alone will buy $50-100 billion of Bitcoin per year. Add Tether and others: huge structural demand that never re-enters circulation.

- Big individual holders (>1,000 BTC) will have sold down. Retail is mostly priced out. Remaining holders will be convicted long-term players.

- Banks will custody Bitcoin directly: unlocking family offices and institutions.

- Bitcoin market cap ($2T today) moves toward gold ($30T) and eventually past it. Superior monetary properties + fixed supply + growing adoption.

- Game theory is in motion: nation-states are entering BTC for votes, later will be for economic survival.

- New layers on top of $STRC will appear: banks and insurers will wrap these into “risk-off” products because the equity holder ($MSTR) eats all the risk.

Things that won’t happen:

- AI won’t settle in Bitcoin: they’ll use stablecoins or specialized chains.

- Cross-border remittances will stay on dollar stablecoins: people want dollar stability in these countries.

Competitive moat:

$MSTR is widening a ditch no one else can cross:

1. Scale that can’t be replicated without spiking the Bitcoin price and helping MSTR.

2. Lowest cost of capital + credibility to raise tens of billions fast.

3. Fully digital, automated capital-raising: six people vs. thousands of bank employees or investment fund armies.

4. Board and CEO 100% aligned: no career-risk-averse committee blocking the vision.

5. Classic outsider shaking up a traditional industry (finance) from the outside (software guy with deep knowledge in history, monetary theory, Nations theory, complex systems, etc.)

Biggest changes usually come from outsiders who aren’t brainwashed by the industry’s conventional wisdom. Michael Saylor has been public since 1998, understands every capital-markets trick, has an engineering mind, and saw the Bitcoin opportunity when 99.9% of CEOs still thought it was magic internet money.

6. Perfect macro- cocktail.

5–10 year projection (2030):

Assume Bitcoin at $250,000 and MSTR owns 1 million coins (0 debt):

MNav 1× → $250B market cap ($800/share)

MNav 2× → $500B market cap ($1,600/share)

MNav 3× → $750B market cap (~$2,400/share)

That’s without any new rabbits they pull out of the hat (and they will because that what great entrepenours do).

Risks (real ones):

- Bitcoin compounds less than cost of capital → dilution

- U.S. government confiscation (unlikely this decade, possible far out)

- Prolonged bear market (>2 years) → forced dilutive issuance to pay preferred dividends.

Closing thoughts:

"The only way to make 10-100× is to be right when almost everyone else is wrong. That requires real market inefficiency."

"Volatility is just new information the market hasn’t digested yet."

"The Wright brothers built the airplane from the bicycle business because the “aeronautical experts” knew it was impossible."

English