Schiele

73 posts

$SPIR Update⁉️

Overall looking very strong. Panes are curling up BIG time and could get extended here soon.

Price is far above it's EMA's, so no need to chase here. Price did turn previous high into support today.

Called the add below $18 last week with my subs. And we're thriving right now.

$SPIR is running one of the cleanest balance sheets in small cap tech right now.

They retired all debt after the maritime divestiture and are sitting on $82M in cash while building AI-powered weather prediction with NVIDIA's Earth-2 platform.

Very strong formula. 🔷🔷🔷

TheGentleTraveler@LeaderInvests

Do we call this strength - $SPIR?

English

Schiele ری ٹویٹ کیا

You have to understand. Whether you want to hear it or not. Your life is solidifying. And premature solidification is what kills dreams. Yeah it's never too late to break the concrete but damn does it harder as time goes by. So shape it how you want while it's still liquid.

Justin Skycak@justinskycak

The longer you delay building the life you actually want, the more likely you are to normalize a weaker substitute. Drift hardens into identity faster than people realize.

English

@MisterMCAP saw its your biggest position. Care to explain why this over $SIVE ? very curious

English

Never got to making an official thesis thread on $SHT, here is one in swedish.

SlarkTrader@SlarkTrader

NYTT CASE 🧵 $SHT Smart High Tech 1) AI-case. Jag har följt detta bolag under 2 års tid men avvaktat med att investera tills nu. Bolaget tillverkar kylningskomponenter till högpresterande elektronik såsom GPU, CPU och AI-chipp. Otroligt relevant i vår tid med ai.

English

Schiele ری ٹویٹ کیا

As recounted by Steve Jobs. We're almost there, Paul, almost there...

English

@daniel_koss trimmed $AEHR but planning on going in when it pulls back?

thats my plan at least

English

@ParadisLabs whats about $VPG and Tesla humanoids? if Elon sticks to schedule *very rare* VPG could rise sooner

English

It's wayyy too early to be investing in Robotics.

Even if they can sprint as fast as Usain Bolt and wield dual MP5K's instead of hands.

ETFs like $BOTZ ($3.2B aum) or $ROBO ($280M aum) are just marketing wrappers bloated with legacy industrial firms + startups with no path to profitability.

$TER semis revenue rose to $883M on AI compute demand. But its Robotics segment contributed only $89M and cut 400 jobs last yr.

Says a lot that leaders in the space need to restructure to account for the hardware lag.

Then you've got $ABB spinning off its robotics division since its 12% margin drags down the group’s 18% average.

So you know it's serious when the world's largest automation players exit hardware to protect profitability.

Humanoid ASPs remain at $200k+, while mass utility requires a drop to $50k-$75k - a target projected for 2050...not this decade, let alone 2026.

AI infrastructure spend is crowding out the capex needed for a robotics boom.

It's pretty obvious that the alpha rn lies in the AI supply chain, not Robotics and well-marketed ETFs.

English

@MisterMCAP @FinnStockinger how did you even find this company? the potential is crazy if they close a deal

English

@FinnStockinger Digging and holding $SHT for the heat bottleneck. Graphene pads producer out of Gothenburg Sweden. Very close to closing a deal as a supplier to what I believe is Nvidia, thru Henkel. Management has hinted on it, but not confirmed. I see a deal being closed within 8 weeks.

English

Alpha is a social sport.

Everyone asks how I caught $SIVE at 4.12 SEK (now almost 350% up) hours before Serenity or how I flagged early $IQE and many others great asymmetric pick.

The truth?

I treat my comments section like a high-level research desk.

A significant amount of my best ideas come directly from you.

While I spend my days filtering through the noise, the "pearls" are often hidden in the replies of sharp retail investors who are grinding harder than the institutions.

Here is how I see it:

By the time a major account "discovers" a ticker, this community has usually been dissecting the filings for days.

My job isn't just to find stocks; it’s to listen to the right people and verify the thesis.

To my followers:

Thank you for the due diligence you share.

There is world-class talent on this platform, and I’m proud to be part of the conversation with you.

I don’t have all the answers, but together, we’re seeing the moves before the rest of the market even wakes up.

Let’s find the next one together.

Repost this to help us reach the sharpest minds on this platform - the more eyes we have, the more "undiscovered" picks we find.

Bookmark this thread, as the comments below will likely become a goldmine of research over the next 24 hours.

➡️What are you digging into right now?

Drop a ticker and a one-sentence thesis. 👇

I’ll pick the most compelling ones and write a deep dive on them soon.

English

@Blinklebloop JCU looks very very good despite the smartphone exposure. nice…

English

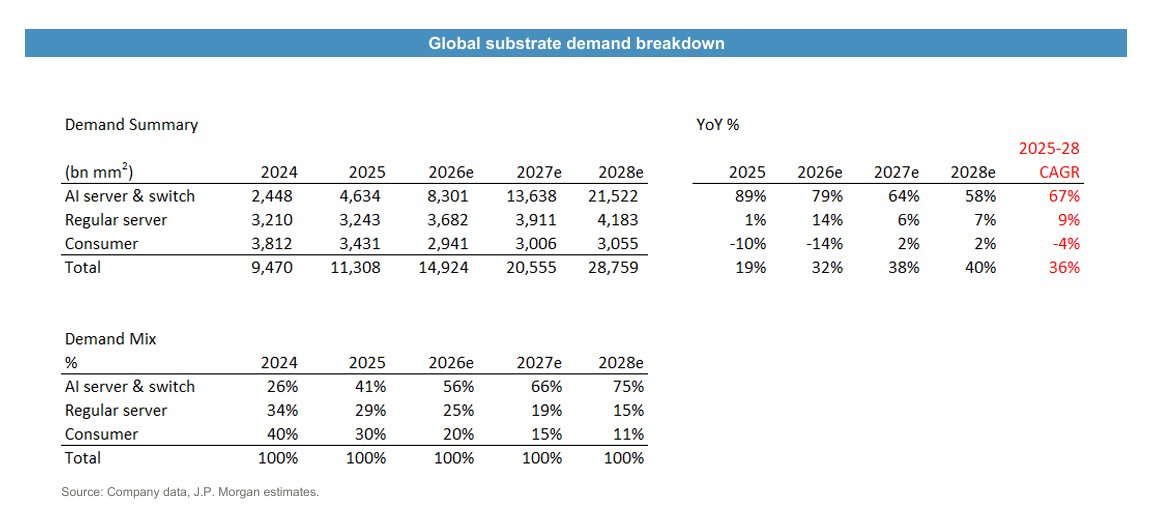

Two adjacent players come to mind here. In the ABF Substrate 'bottleneck'.

C. Uyemura (4966.T) and JCU Corporation (4975.T)

C. Uyemura chemicals are essential for the "seed layer" in SAP. They also provide the automated plating equipment used in substrate factories.

Trading at a PE of around 25x. The revenue has been showing up, but I believe the ramp will start later- becaues the new lines need to be qualified first, and so there is a 'qualification lag' before companies (like Ibiden and Unimicron) start ordering more chemicals.

You will notice that C. Uyemura is outperforming JCU.

C. Uyemura is more "pure play" exposed.

JCU is a great company, but is heavily exposed to high-end smartphone PCBs. Smartphones are forecast to have a terrible year due to the memory shortage.

But this will bounce back when that eventually subsides.

Right now C. Uyemura is a different expose to JCU. Even though JCU chemicals (CU-Brite) is still used to make ABF substrates for high-end PCBs for Datacenters too.

I believe both companies will see a real ramp in AI/Datacenter later on.

It is possible there is a bottleneck in these chemicals too, if they don't expand capacity fast enough.

JCU Corp is also an exposure to Hybrid Bonding through their TiPhares chemical. Still negligible as a % of revenue, but Tiphares R&D plant is located in Kumamoto, near TSMCs gigafab.

Jukan@jukan05

A striking sentence I read today: We don’t think power is the constraint for TSMC’s chip demand, at least for 2027, but ABF substrate and HBM supply are major gating factors. -Morgan Stanley

English

Schiele ری ٹویٹ کیا

@bubbleboi plan from the start was probably to use this 2 weeks ceasefire to get more assets. war in ME will happen as long as Israel exists with their idea of Greater Israel, and the US will be dragged to war with them every single time lol..

English

@HyperTechInvest small question, but whats the difference between Nan Ya PCB 8046.TW and Nanya technology corp 2046.TW ?

English

Taiwanese media Commercial Times reports the region’s worst semiconductor supply shortages

1. HVLP4 copper foil

Demand is rising from Rubin upgrades and higher switch specifications. Supply is constrained by process difficulty and unstable yields, which keeps effective capacity below planned capacity. Prices have already increased around 5% to 10% and can move higher.

Co-Tech Development (8358.TWO)

Unimicron (3037.TW)

Nan Ya PCB (8046.TW)

Kinsus (3189.TW)

2. T-Glass fiberglass cloth

Supply is limited by capacity and yield constraints at key producers. Demand is being driven by advanced FCBGA substrates. Expected price increase is around 30% to 40% this year.

Nitto Boseki (3110.T)

Taiwan Glass (1802.TW)

Unimicron (3037.TW)

Nan Ya PCB (8046.TW)

Kinsus (3189.TW)

3. Low DK fiberglass cloth

Demand is rising for higher-performance AI and networking boards. Supply remains tight despite process improvements. Expected price increase is around 20% to 30% this year.

Elite Material (2383.TW)

Unimicron (3037.TW)

Nan Ya PCB (8046.TW)

Kinsus (3189.TW)

4. Drill bits for high-end PCBs

Higher-end PCB materials such as M8 and M9 reduce drill life to around one-sixth of traditional materials. That sharply increases drill bit consumption. AI-specific coated drill bits are priced around 20% to 30% above standard ones, and for boards above 7.5mm thickness they can cost more than 6x as much.

Topoint Technology (8021.TW)

5. ABF substrate inputs

Larger CPU and GPU packages are increasing substrate area and layer counts. Rubin substrates are around 75% larger than the prior generation and have reached 18 layers. That tightens upstream ABF-related materials and supports further price pass-through.

Unimicron (3037.TW)

Nan Ya PCB (8046.TW)

Kinsus (3189.TW)

Nitto Boseki (3110.T)

Taiwan Glass (1802.TW)

Elite Material (2383.TW)

Co-Tech Development (8358.TWO)

6. High-end PCB and substrate manufacturing capacity

The constraint is also in qualified production capacity. Not all suppliers can meet the process requirements, certifications, and yields needed for advanced AI carrier boards and substrates. The shortage is in both materials and manufacturing capability.

Unimicron (3037.TW)

Nan Ya PCB (8046.TW)

Kinsus (3189.TW)

English

@zephyr_z9 wouldnt an even essier trade be $SOI due sto substrate demand? or am I mixing concepts here

English

Schiele ری ٹویٹ کیا

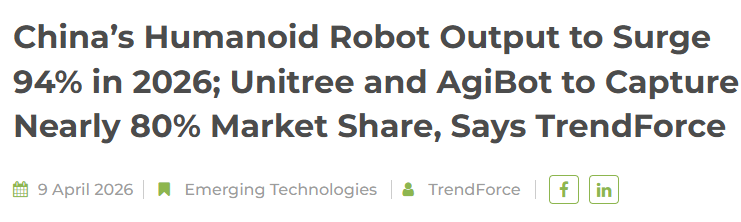

$MU $DRAM China’s humanoid robot output is projected to surge by up to 94% in 2026

"Vehicles with L4 autonomy require over 300GB. Humanoid robots powered by a compute platform that rivals a high-end L4-capable automobile" - @MicronCEO

Unitree Robotics and AgiBot are expected to dominate, together capturing nearly 80% of total shipments in China thanks to strong progress in monetization and mass production scaling.

-Unitree:Humanoid robot revenue accounted for over 51% of its total revenue in 2025.

-Combined gross margin (humanoid + quadruped robots) reached 60%.

-Planned annual production capacity: 75,000 humanoid robots and 115,000 quadruped robots.

AgiBot:

-Rolled out its 10,000th general-purpose embodied robot (Expedition A3) in late March.

-Rapidly scaled production in 2025–2026: from 1,000 → 5,000 → 10,000 units within a short period.

Trade Whisperer@TradexWhisperer

$MU Signs of structural memory transformation during earnings today. Must Read 👇 Automotive: "The average car today has less than L2 ADAS capability, containing approximately 16GB of DRAM, while vehicles with L4 autonomy require over 300GB." Robots: "Humanoid robots will be AI-enabled and powered by a compute platform that rivals a high-end L4-capable automobile, requiring significant memory and storage. We expect this exciting new category to further underpin the long-term favorable dynamics shaping our industry." PC: "PCs with on-device agentic AI have recommended memory specs of at least 32GB, twice the average PC." Workstations: "The fast-growing category of personal AI workstations, such as NVIDIA DGX Spark and AMD Ryzen AI Halo, come in 128GB configurations, ideal for running large language models on device." Mobile: "The mix of flagship smartphones shipping with 12GB or more of DRAM increased to nearly 80% in Q4, up from under 20% a year ago." Data Center LP DRAM: "We sampled the industry's first 256GB LP SOCAMM2 product, built on our 1γ node, enabling 2TB of capacity per CPU. Quadrupling content from just a year ago." Data Center Demand: "AI server demand (vs. traditional server) is driving DRAM and NAND data center bit TAM to exceed 50% of industry TAM for the first time in calendar 2026." The AI Shift is Here

English

@HyperTechInvest i agree. but in the case that someone could take in more risk, wouldnt the play probably be going for $AAOI , just because of the huge difference in mketcap it has with $COHR and $LITE

English

$LITE makes $COHR look cheap

I understand $LITE has the best tech and yields at the moment

However, $COHR is a very competent company, and its financials are stronger right now

I can’t imagine this gap lasting in the long term, at least not at this scale

Any thoughts?

English

@HyperTechInvest agree. people "panicking" over missing $AEHR or $AAOI , by 2028 it won't matter if you went in at 30 or 80USD lol. they are just starting..

English

If you think photonics is big, you aren’t prepared for what’s coming next

Few understand

English

@ThematicTrader same :( haha. anyway I expect this company to perform incredibly well during the next years. I’ll just wait for a pullback(if it ever happens lol) and go in again. people have forgotten that Iran-US war is not finished and ceasefire is not going well… we still in for surprises..

English

$AEHR running away from me after selling at $51 pre earnings has been brutal 🥲

9 Ventures@ThematicTrader

$AEHR Strong earnings report. Anyone that looks at current revenue is an idiot and doesn't understand the story. - $37M quarterly bookings and a 3.5x book to bill - Backlog guidance is at high end of the range. - Received follow-on orders from their leading SiPho customer. - Follow-on orders of Sonoma Systems expected during FY27 from their largest hyperscaler customer for their AI processors ASICs. - They are scaling their co-man to produce 20 additional Sonoma Systems per month, implying ability to support $360M - $480M of Sonoma revenue ($1.5M-$2.0M ASP) All good news. Stock likely got a little ahead of its skies though and chasers might get caught here. I'll be looking for a re-entry this week. Will update in real time as always.

English

@ParadisLabs @FT do you see Intel gaining much more share of the market in the future due to security reasons?

English

I'm very bullish on Taiwan.

Following on from my Browave thesis:

> @FT report that "the US tech industry will remain critically dependent on Taiwan for the immediate future."

> " $AAPL, $NVDA, $AMD, $QCOM and $AVGO have no viable alternative manufacturer of advanced chips at the scale they need."

Taiwan's GDP growth will be crazy high for the next ~5 years given the AI supercycle and near monopolies e.g. mass production of 2nm from $TSM.

Also CoWoS - where $NVDA Blackwell & Rubin and $GOOGL TPUs require this specific packaging to function.

Taiwan has raised CoWoS capacity targets for 2026–2027 to meet "urgent orders" from $GOOGL and $NVDA.

No other country has the scaled infrastructure to perform CoWoS.

Also, geopolotics aren't really a concern to me:

There's huge global reliance on Taiwan's technology. All major powers (including China) benefit more from Taiwan’s continued operation than its destruction.

Paradis Labs@ParadisLabs

Relatively unknown CPO long idea: Browave (3163.TWO) at ~$2.4B market cap Decided to research more, and have decided to go long (small position) as the story seems pretty compelling. Just some very top level notes that are hopefully digestible. ----- Browave provides the fiber arrays and internal interconnects necessary for CPO to bridge the gap between AI chips and optical signals. Their Fiber Shuffle Box is a key CPO enabler that organizes massive complexity inside AI servers. With mass production scaling 10x units per month by early 2027. Partner with $GLW for high density assembly. ----- As AI data centers transition from 800G to 1.6T and look toward 3.2T, they face a physical crisis: Because CPO system and chip designs vary significantly (e.g. $NVDA vs. $AVGO vs. Hyperscaler custom ASICs), off-the-shelf connectors are failing. Traditional MPO architectures are too bulky for the 1U switch trays of the Vera Rubin and Feynman. Integrating optics inside the package makes them nearly impossible to service if a fiber breaks, unless a detachable mechanical interface is used. > Browave is scaling CPO production from an initial 1,000 units/month in Q4 2024/2025 to a targeted 10,000 units/month by Q1 2027. This indicates a massive secured order book, likely tied to $NVDA's Spectrum-X Ethernet rollout scheduled for H2 2026. > Browave has also launched MMC jumpers, which offer 3x the density of traditional MPO solutions. This lets $NVDA and others to fit 1,000+ fibers into a single 1U tray without blocking airflow. Browave anticipates that initial 2026 deployments will focus on scale-out switch architectures (rack to rack), with scale-up adoption (GPU-to-GPU) becoming the driver by 2028 A market that could be 10x larger than the current scale-out TAM. In terms of suppliers: Browave relies on Landmark for the InP and GaAs epiwafers used in the lasers they pig tail and assemble. $SIVE also collaborating on ELS modules to separate lasers from 1000W GPUs. Risk disclosure: > Browave itself admits that meaningful scale-up CPO adoption (the 10x multiplier) won't materialize until 2028. This creates a potential investment valley in 2027. > LPO remains a viable, lower cost bridge for 1.6T. If hyperscalers choose LPO over CPO for another 24 months, Browave’s growth targets will be deferred. ----- Tldr: While logic companies fight over chips, Browave owns the "shuffle" that makes those chips useful. The recent 10x capacity surge target is the strongest fundamental indicator that a regime change in AI networking is underway. Am Watching for the official announcement of the private placement subscriber in May/June 2026. This will determine if Browave is a "protected asset" in the $NVDA / $TSM supply chain. Note, I have not looked into financials yet as have been travelling, so investing purely on the story for now. But as mentioned, just a small speculative position for now. More focused on the likes of $TSEM, $AAOI, Samsung, $AEHR, $LITE / $COHR

English