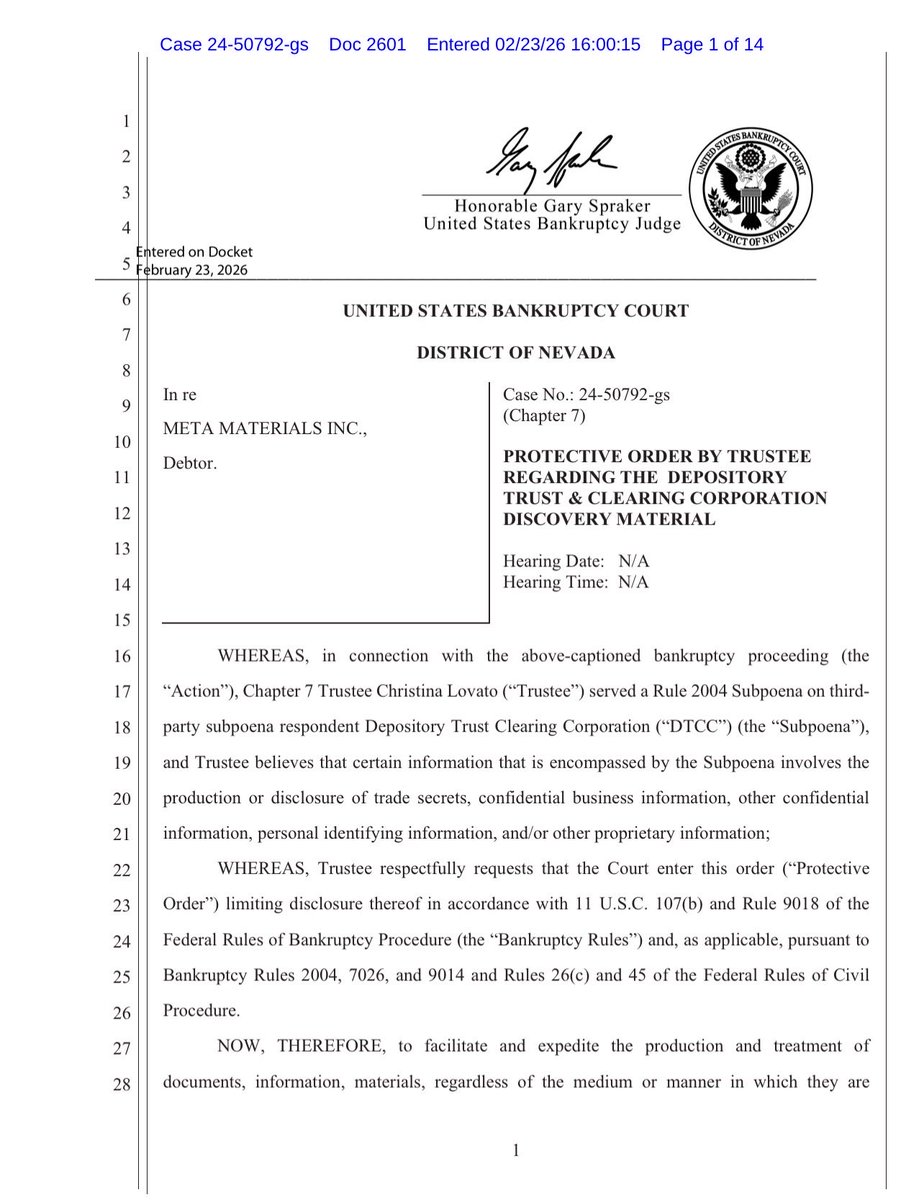

Ann Vandersteel™️@annvandersteel

President Trump,

FINRA and the SEC are moving to allow deletion of CAT data older than three years. This is not routine. This risks erasing critical evidence of market manipulation, naked shorting, and systemic fraud.

At the very moment Americans are demanding transparency, regulators are preparing to shrink the window of accountability.

You have the authority to act.

Sign this Executive Order. Enforce strict T+1 settlement. Criminalize naked shorting. Hold all participants accountable. Preserve all CAT data.

This is about protecting the financial future of every American and restoring trust in our markets.

Do not let the evidence disappear.

Please sign the order.

@realDonaldTrump #MMTLP #GME #AMC #DJT

@KurtOlsen_USA @LegalBrains @RealTheoWold

EXECUTIVE ORDER (proposed)

Strengthening Securities Settlement Integrity, Reforming Regulation SHO, and Combating Fraudulent Market Practices

By the authority vested in me as President by the Constitution and the laws of the United States of America, including the Securities Exchange Act of 1934, 15 U.S.C. 78a et seq., the Securities Act of 1933, 15 U.S.C. 77a et seq., and 3 U.S.C. 301, it is hereby ordered:

Section 1. Purpose

The integrity, transparency, and lawful operation of the United States securities markets are essential to the national economy, the protection of investors, and the preservation of public trust.

Abusive trading practices, including persistent failures to deliver, manipulative short selling practices, and the creation or circulation of securities interests not backed by valid issuance, undermine market stability and may violate federal law.

This Order directs strengthened enforcement of existing law and mandates regulatory reform to eliminate systemic settlement failures and unlawful short selling practices.

Section 2. Policy

It is the policy of the United States to:

(a) Ensure strict compliance with lawful securities settlement requirements

(b) Eliminate persistent failures to deliver and abusive short selling practices

(c) Prevent manipulative or deceptive conduct prohibited under Sections 9 and 10(b) of the Securities Exchange Act and Rule 10b-5

(d) Promote fair, orderly, and efficient markets pursuant to Section 15(c)

(e) Protect investors and strengthen confidence in United States capital markets

(f) Encourage reporting of violations through whistleblower protections under 15 U.S.C. 78u-6

Section 3. Enforcement of Settlement Requirements

(a) The Securities and Exchange Commission shall, pursuant to its authority under Section 17A of the Securities Exchange Act, ensure strict enforcement of the T plus 1 settlement cycle.

(b) Clearing agencies, broker dealers, and market participants shall be required to implement systems reasonably designed to prevent failures to deliver.

(c) The Commission shall require enhanced, standardized, and public reporting of settlement failures and close out activity.

Section 4. Reform and Strengthening of Regulation SHO

(a) Within 90 days of this Order, the Securities and Exchange Commission shall propose and, as appropriate, adopt amendments to Regulation SHO to strengthen enforcement and eliminate systemic abuse.

(b) Such amendments shall, to the fullest extent permitted by law, include:

1.Mandatory Pre Borrow Requirement

Require that, prior to effecting any short sale, a broker dealer must obtain and document a confirmed borrow of the security, eliminating reliance solely on locate arrangements where such reliance contributes to settlement failures.

2.Accelerated Close Out Requirements

Require immediate or same day close out of failures to deliver for all equity securities, including threshold and non threshold securities, and eliminate extended close out timelines that permit repeated failures.

3.Prohibition on Reset Transactions

Prohibit the use of options, swaps, or other derivative or structured transactions designed to evade close out requirements or mask failures to deliver.

4.Enhanced Threshold Securities Standards

Strengthen the criteria for threshold securities and require automatic trading restrictions where persistent failures occur.

5.Real Time Transparency

Require public disclosure, on a frequent and standardized basis, of aggregate short positions, failures to deliver, and securities lending data sufficient to promote market transparency.

6.Strict Locate Enforcement

Clarify and enforce the requirement that any locate must be based on a bona fide and verifiable source of borrowable securities, with liability for false or unsupported locates.

(c) The Commission shall ensure that Regulation SHO is administered in a manner that prevents the creation of synthetic or unbacked share supply that distorts price discovery.

Section 5. Prevention of Unlawful Short Selling Practices

(a) The Securities and Exchange Commission shall take all lawful measures to prevent and prosecute violations involving:

1.Short sales conducted without a reasonable and verifiable ability to deliver

2.Schemes to evade locate or close out requirements

3.Manipulative conduct that creates artificial market supply

(b) The Department of Justice shall prioritize prosecution of willful violations of federal securities laws, including fraud, market manipulation, and conspiracy offenses under Title 18.

(c) Nothing in this Order shall be construed to create new criminal offenses, but rather to direct enforcement of existing law to the fullest extent.

Section 6. Accountability Across Market Participants

(a) Enforcement shall apply to all participants in the securities transaction chain, including executives, traders, brokers, compliance personnel, clearing agents, and operational staff.

(b) The Securities and Exchange Commission and self regulatory organizations shall strictly enforce supervisory obligations under Section 15(b)(4)(E).

(c) Individuals who knowingly or recklessly participate in violations shall be subject to existing civil and criminal penalties.

Section 7. Industry Bars and Remedial Authority

(a) The Securities and Exchange Commission shall fully utilize its authority to:

1.Suspend or revoke registrations

2.Bar individuals from association with broker dealers, investment advisers, and other regulated entities

3.Impose civil penalties and disgorgement

(b) Agencies shall coordinate to ensure that individuals responsible for serious violations are removed from positions of trust in financial markets.

Section 8. Whistleblower Protection and Incentives

(a) The Securities and Exchange Commission shall enhance enforcement of whistleblower protections under 15 U.S.C. 78u-6.

(b) Individuals reporting violations shall be protected from retaliation and may receive financial awards consistent with law.

(c) Priority shall be given to information exposing systemic manipulation or widespread investor harm.

Section 9. Interagency Task Force on Market Integrity

(a) An interagency task force is hereby established, chaired by the Securities and Exchange Commission, with participation from the Department of Justice, the Department of the Treasury, and other relevant agencies.

(b) The task force shall:

1.Coordinate investigations and enforcement

2.Share intelligence and data

3.Recommend additional regulatory or legislative reforms

(c) Within 120 days, the task force shall report its findings and recommendations to the President.

Section 10. General Provisions

(a) Nothing in this Order shall impair the authority granted by law to any executive department or agency.

(b) This Order shall be implemented consistent with applicable law, including the Administrative Procedure Act.

(c) If any provision of this Order is held invalid, the remainder shall not be affected.

Section 11. Effective Date

This Order shall take effect immediately.

Section 12. Statement of National Commitment

The United States affirms that its markets must operate on truth, transparency, and accountability. The protection of investors and the preservation of fair markets are essential to the strength of the Nation and the future prosperity of its people. This Order advances those principles and reinforces confidence in the American system of free enterprise.