GregInvest 💵@GregInvestFr

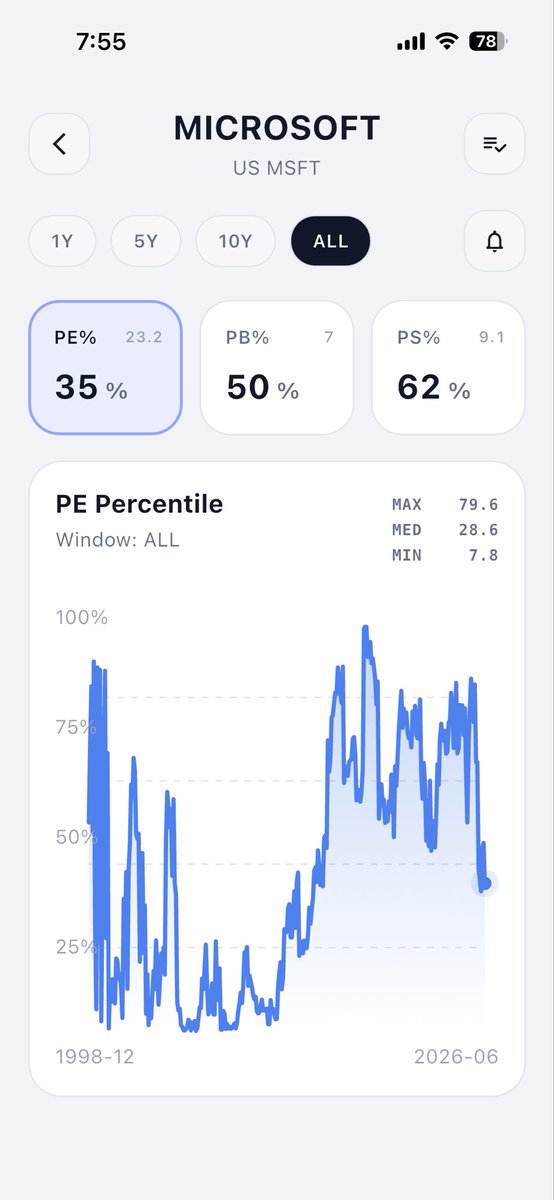

Microsoft $MSFT 🇺🇸

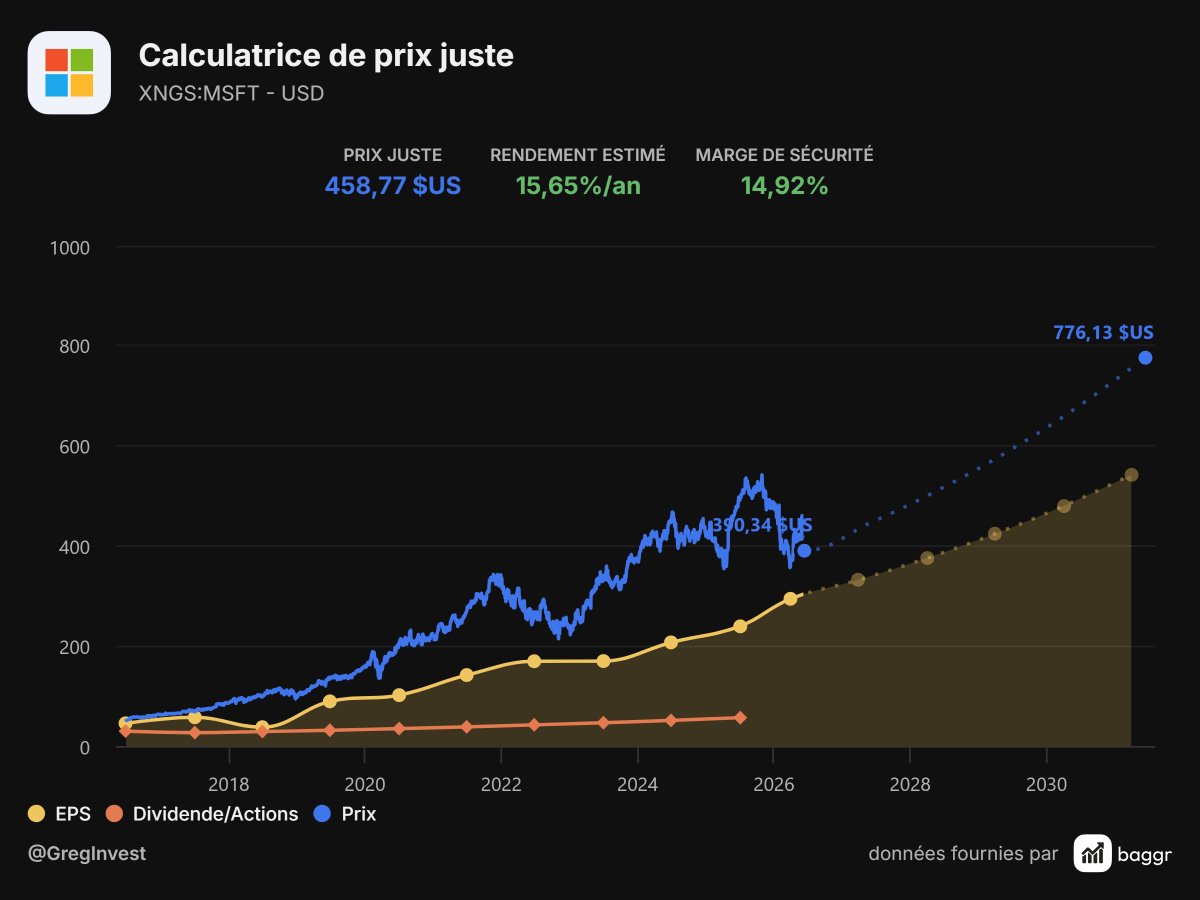

Le marché traite actuellement Microsoft comme une entreprise en ralentissement.

Pourtant, les chiffres racontent une autre histoire.

• CA actuel : 318 Md$

• CA estimé en 2030 : 651 Md$

• soit plus du double en moins de 5 ans

Et malgré cela :

• PE actuel : 23x (vs moyenne à 32x)

• forward PE : 21x

• forward PE 2030 : 11,6x

Autrement dit :

Le marché valorise aujourd'hui Microsoft comme si sa croissance future était déjà compromise.

Pourtant, l'entreprise est idéalement positionnée sur :

• l'IA

• le cloud

• les logiciels professionnels

• les infrastructures de données

Difficile de trouver une entreprise de cette qualité qui se paie à un multiple aussi raisonnable.

Techniquement, le titre est actuellement sur sa MM200 hebdomadaire.

Personnellement, je prévois de renforcer entre 350 et 360 $ si le marché m'en donne l'opportunité.

C'est aujourd'hui ma plus grosse position en portefeuille.

Alors selon vous, Microsoft est-elle l'une des meilleures opportunités du marché actuellement ?