Sabitlenmiş Tweet

jakee

1.4K posts

@VannaCharmer Rare bad Mosi take… it’s okay I’ll still take you to Mumbai when we’re back to aths

English

Tell me you don't understand crypto without telling me you don't understand crypto

No volume is going to come from the Believe mobile app and this is probably just Pasternak's web2 fixation of 'we should launch a mobile app'. A mobile app for a launchpad focused on 'higher quality' coins vs quantity of coins will probably be useless (?)

I don't see how a mobile app increases the chances of attracting 'new creators' or reduces the stigma of launching a coin. People who think launching a coin is a scam will keep thinking the same thing either on mobile or desktop

English

Bonkfun coins don't even need to be artificially propped up by whales anymore. They are just outright winning the ticker pvp wars on new deploys over and over again.

MechaHitler on Bonk at 1.2m vs 80k on pumpfuns deploy

jakee@0xjakee

Trend reversals can happen in the blink of an eye in crypto but as it currently stands I don't know who would invest 600m into pumps TGE with numbers like these In the past 24hrs the highest mcap coin launched on pump is only at 158k mcap and they only have 4 of the top 25 coins in that time frame Losing the deployers is losing losing the war Pumps tokenomics need to be perfect

English

Trend reversals can happen in the blink of an eye in crypto but as it currently stands I don't know who would invest 600m into pumps TGE with numbers like these

In the past 24hrs the highest mcap coin launched on pump is only at 158k mcap and they only have 4 of the top 25 coins in that time frame

Losing the deployers is losing losing the war

Pumps tokenomics need to be perfect

English

Markets doing a bad job pricing this in - prob the most bullish announcement hype has had this year. The moat just doubled in size

Phantom@phantom

Introducing: Phantom Perps 👻 ♾️ Go long or short in just a few taps. 100+ markets. Up to 40x leverage. All in your pocket. Powered by @HyperliquidX

English

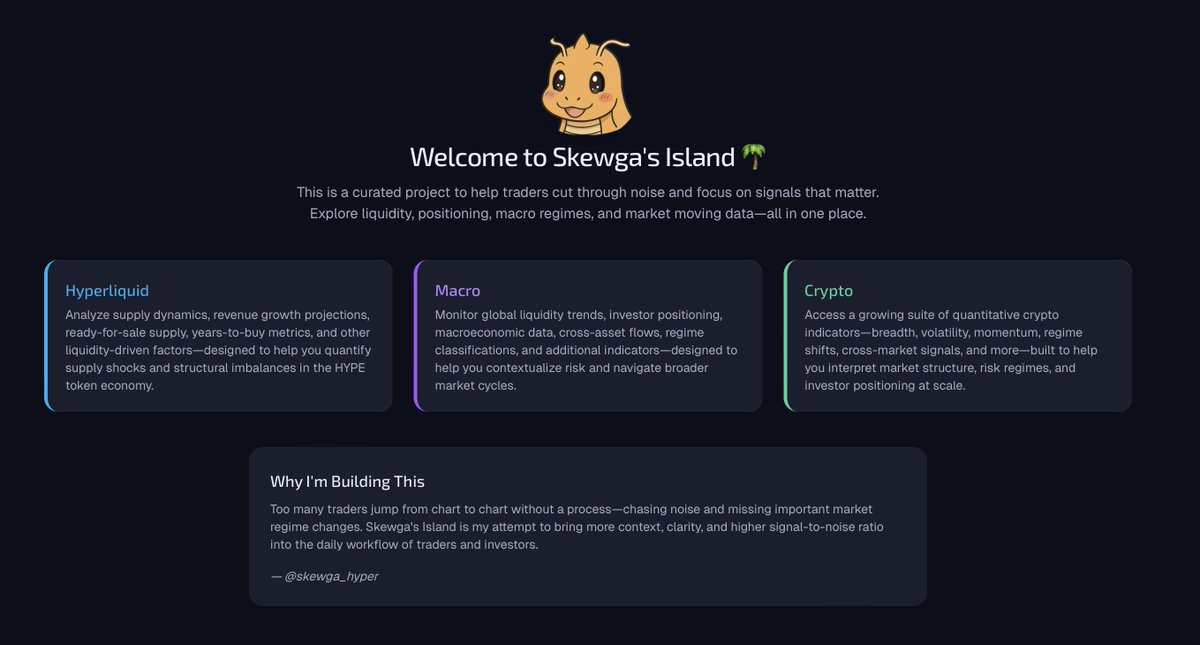

Finally a frontend for all my quant stuff. Starting off with 4 different tools under the Hyperliquid section, pretty sure you guys will find something interesting there...

Link: skewga.com

This is my nights and weekends project so don't expect perfect UI as I'm still learning the art lol. I hope to release a lot more stuff in the coming weeks/months.

What I like the most about this project is that it really keeps me entertained so I avoid overtrading and checking price, kinda like touching grass for me lol.

English

@chairmanda0x @3janexyz @ethereum Great write up ty do you think it’s going to be worth farming it as a lender or is it too risky with default risk?

English

jakee retweetledi

3Jane: Introducing Under-Collateralized DeFi Loans

@3Janexyz is aiming to become the first viable on-chain “credit-based money market” protocol on @Ethereum. Credit-based money markets in DeFi have never worked before because under-collateralized loans don’t work when users are anonymous and have no legal obligation to repay loans. As a result, DeFi loans are currently split into two distinct markets: 1) Over-collateralized loans supported by protocols like @Aave and 2) Under-collateralized reserved for off-chain private credit firms, institutional market makers, or reputation-based social circles like @maplefinance. However, both these options severely limit the potential of on-chain credit, whether its the amount of money able to be borrowed or the people who are able to borrow. 3Jane wants to change this.

How 3Jane Works

3Jane functions as a peer-to-pool credit-based money market that has three primary parties in its protocol: the Lenders, Borrowers, and the 3Jane protocol that manages functions like underwriting, credit scores, and non-performing loan (NPL) auctions.

Lenders

Lending to 3Jane remains permissionless and works by simply depositing USDC to mint USD3, a dollar-denominated yieldcoin (ERC-4626) backed by the pool of credit lines. USD3 has a senior claim on interest repayments in case of default and has real-time liquidity for withdrawals based on the market reserves. USD3 is not a stablecoin, rather a yield-bearing token, and is susceptible to drawdowns in price if an unexpected number of defaults occur. USD3 comprises 85% of the total money market liquidity pool.

Lenders can also stake their USD3 for sUSD3 (ERC-4626) in order to lever their position and generate a higher level of yield. However, in return for a higher level of yield, stakers agree to absorb first-losses in the case of defaults and become a more junior level of debt compared to USD3 holders. sUSD3 also has a cooldown period before it can be withdrawn from the liquidity pool. sUSD3 comprises 15% of the total money market liquidity pool.

3Jane lenders are able to generate a base-level of yield via @Aave because idle USDC is initially supplied to the Aave V3 USDC market. Whenever a borrower borrows USDC, 3Jane withdraws the required amount from Aave.

Borrowers

Borrowing from 3Jane requires users to connect an on-chain wallet, log into their bank account via @Plaid, and sign a Merchant Cash Advance (MCA) legal clause message before being able to borrow up to their credit line. An MCA ensures that the borrower enters into a legally binding contract to ensure that legal recourse under U.S. law is possible in the case of default.

A borrowers credit line and interest rate are determined by the 3Jane Credit Risk (3CA) model after analyzing the borrower profile. The initial interest rate is calculated by summing a base interest rate (Secured Overnight Finance Rate proxy) and a default credit risk interest rate determined by the 3CA’s probability-of-default model.

During the lifetime of the loan, the borrower must make monthly minimum payments in order to maintain good standing with the protocol. Every 30 days, 3Jane reevaluates a borrowers credit limit and interest rate using refreshed bank-cash, CEX balances, and on-chain asset data.

When a borrower reaches a point of repayment, the borrower will enter a grace period in which there are no additional charges but repayment is required. If the loan is not repaid during this time, the borrower will enter a delinquency period where a late-penalty interest rate begins accruing. If the loan is still not repaid, then the borrower will enter a default period where the credit line is frozen and 3Jane initiates an NPL auction to recoup the debt. At the time of writing, the length of each time period has not yet been determined.

3Jane Protocol

Underwriting

In order to underwrite the loans on its platform, 3Jane collects a plethora of data from a user including on-chain and off-chain account numbers and activity to derive an on-chain credit score native to 3Jane called a Jane Score that will determine how much a borrower can borrow and at what interest rate the loan will be priced at.

In spite of the usual, 3Jane is currently only accessible to US-based users due to the requirements for information it holds to generate a Jane Score. When generating a Jane Score, 3Jane incorporates credit score models from @CredProtocol, @TheBlockBureau, and VantageScore 3.0. Cred Protocol and Blockchain Bureau are both on-chain credit risk platforms while VantageScore 3.0 is an alternative credit scoring model to FICO developed by the three major credit bureaus (@Experian, @TransUnion, @Equifax).

To generate a Jane Score, 3Jane uses the 3CA model to analyze a users full financial profile including crypto and cash assets (tokens, @Coinbase assets, banking assets), cash flow positions (LP positions, bank income), wallet and browser history, and credit scores (on-chain credit score, VantageScore 3.0, FICO). This is done via Plaid and @ReclaimProtocol integration, allowing 3Jane to access and verify an individuals off-chain assets, income, and identity. Plaid connects and Reclaim verifies using a zero-knowledge Transport Layer Security (zkTLS) proof, ensuring that user data can be simultaneously verified while remaining secure.

The Jane Score is then used to determine a borrowers credit line and interest. As stated above, this Jane Score is refreshed with new data every 30 days.

An additional note is that 3Jane credit lines are structured as a Merchant Cash Advance (MCA) where financing terms are structured as cash for a percentage of future sales. This means that when a user borrows from 3Jane, the credit line is treated as an advance against the future growth of their portfolio—not as a traditional loan with fixed repayment terms. That means that the amount a borrower is required to repay cannot exceed the total growth in their portfolio (from asset appreciation and incoming cash flows) since they first drew down the credit line. If the borrower’s assets and cash flows have not grown enough, their repayment obligation is capped by that growth. Additional details for this specific mechanism have not been publicly released.

Delinquency

3Jane manages platform delinquencies by slashing the defaulters 3Jane score, decreasing future credit line and increasing future interest rates, and initiating an NPL auction to sell debt to U.S.-based collection agencies. This ensures that the platform is protected from those who have defaulted once before and gives the protocol a process to recoup part of the defaulted loan.

It’s also interesting to note that when a loan is defaulted on, 3Jane does not immediately write it off. 3Jane uses a model to estimate the market value of the loan by calculating the probability of loss and recovery, reducing markdown severity for the protocol but also potentially artificially inflating the health of the protocol.

Financials/History

3Jane initially launched on April 18, 2024, as a crypto-native derivatives protocol on Ethereum. However, 3Jane pivoted to its current credit-based money market protocol announcing a $5.2M Seed Round on June 4, 2025, led by @Paradigm with participation from @wmt_ventures, @cbventures , and @robotventures.

3Jane is led by founder @_yakovsky, a graduate of @Stanford who interned at @CreditKarma before working as an engineer and then Head of Strategy at @Aevoxyz, a crypto-derivatives platform. He left Aevo on March 2024 to launch 3Jane.

3Jane also has team members, @kunst13r (@Base and @nansen_ai) and @VasilhsTaff (@RenzoProtocol).

Potential Risks

As a lender, you will be exposed to smart contract risk (bugs, exploits), credit default risk (higher than expected default rate), liquidity risk (redemption requests exceed available liquidity when withdrawing from Aave and liquidity pool), oracle risk (manipulated price or SOFR feeds distort LTV and rates), and governance risk (protocol parameter changes).

As a borrower, you will be exposed to private & data-leak risk (data leak during KYC and financial analyzation process) and collateral-valuation risk (asset and loan LTV repricing during lifetime of loan).

Loan Example

Total Assets: 932.67K (441K Cash)

3Jane Score: 9300 / 10000

Option 1: Over-collateralized Borrowing

Collateralize 52K ETH and borrow 25K USDC against it @ 5.33% variable APR via Aave (50% LTV)

Collateralize 27K S and borrow 13K USDC against it @ 3.27% variable APR via Aave Sonic(50% LTV)

Result: 38K USDC @ blended 4.63% APR

Option 2: 3Jane Unsecured Borrowing

3CA underwrites against on-chain transactions, off-chain credit score, and entire DeFi/CEX/Bank financial profile. Generates a 141K USDC credit line (15.1% of asset value) at 7.93% variable APR (including a fixed 2.6% credit default risk premium above 5.33% SOFR)

Borrow up to 141K USDC

Result: 141K USDC @ blended 7.93% APR

3Jane Potential

If 3Jane is able to successfully facilitate under-collateralized on-chain loans, it could have a widespread impact across all of DeFi. As of June 5, 2025, @Ethereum currently maintains $62.904B in DeFi TVL and 124.282B in stablecoin assets according to @DefiLlama. If users were able to utilize these assets, alongside off-chain assets, to generate 0% collateral loans, the size of the DeFi industry would expand exponentially.

Although 3Jane has said that the endgame goal is to become the global unsecured credit facility for verifiable AI agents, I think the first users of 3Jane will ultimately be those looking to lever up their farming positions. However, if 3Jane is able to be successful building TVL and remaining solvent, this could spawn the creation of new DeFi verticals such as structured loan products and potentially pave the way for DeFi to be integrated into real life transactions if property/car ownership deeds are eventually processed on-chain.

3Jane is still in its burgeoning stages as it works through initial speed bumps as outlined by @GeorgePBeall’s personal experience. Additionally, 3Jane’s 3CA underwriting algorithm should continue to improve as it recalibrates its probability-of-default bands and credit-limit curves to reduce the risk of default and improve the protocol through the continued use of the protocol. As 3Jane continues to grow, I think it is definitely a protocol to keep an eye on and potentially try out. Mainnet launch is expected in Q3 2025.

3Jane@3janexyz

1/ 3Jane is excited to announce our $5.2M seed round led by @paradigm to enable the first scalable credit-based money market on Ethereum. This funding accelerates our long-term vision of driving cryptonative credit creation & economic growth.

English

In all seriousness, Cobie's sonic looks cool but doesn't seem like a direct competitor to me -

Launchcoin sold off because

(a) Your counterparties don't know how to read

(b) Your counterparties are emotional

or (c) both of the above

@notthreadguy need you dialled for this interview

English