@EhrmantrautCap_ Who you reckon has the bigger upside from here, MU, SK Hynix or SanDisk?

English

Fabri

17.5K posts

Abstract of SanDisk (SNDK) Note, Implications Near Term Pricing: we believe that Samsung/SK/SNDK expect ~30% qoq for eSSD for CY3Q which suggests ~0.45, vs ~0.35 in CY2Q LTAs : We believe that Samsung’s floor price of LTA is above 0.5! #SNDK #SSD #NAND

Boooooooom!!💣 Lännen APT 3140 USD/MTU!! 🔥🔥 (3000-3280) Nousu jatkuu edelleen, aivan mahtavaa! #Tungsten $EQR.AX $GMET 🍀

In 2018, I worked on the $VIAV ONT and benchmarked it against a solution that my former employer offered that was easily at 1/3 of the price point. I won that deal for manufacturing, and it still remains one of my proudest achievements as I had to work with the team to build a whole new product from scratch in a short period to complete the test matrix. I still think optical transceiver companies can't scale manufacturing with $VIAV products. Yes, Viavi will sell their products like hot cake in this market and under these favorable circumstances, every optical transceiver module manufacturer or R&D test lab will use their systems + a combination of a either a $TDY scope to a $KEYS scope (real time or sampling scope) + the expensive software licensing + you need a separate clock recovery unit (CRU) to capture the PAM4 signal at 100G per lambda data rates and above, which is another win for Keysight as their sampling scope + CRU only work together - like a Catholic marriage, no external party poopers allowed). The real money being made in this area of test and measurement will be in mass manufacturing of optical transceivers for all these test and measurement firms, so unless Viavi slashes prices for bulk orders and offers very advantageous terms, same for Keysight $KEYS, I don't see it my dudes. That is just my honest take.

Futebol de verdade … 👏🏾👏🏾

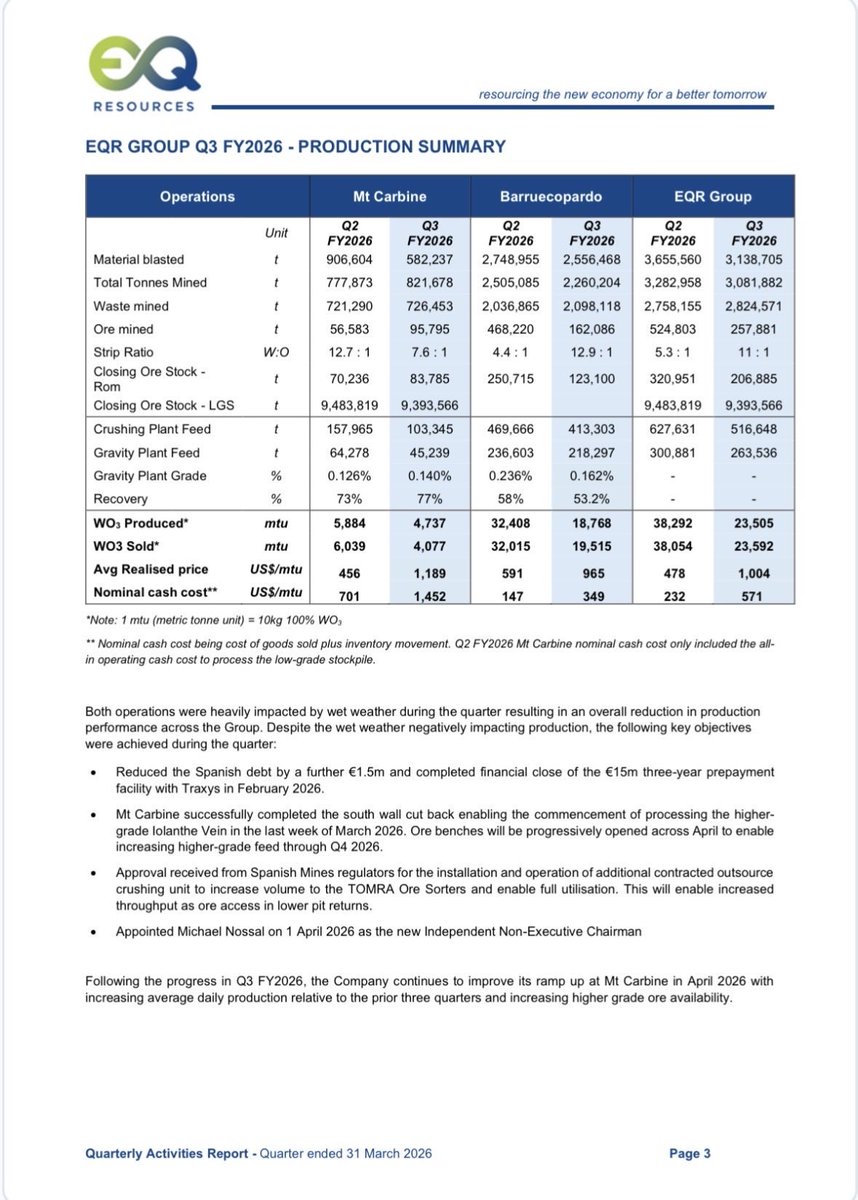

The quarterly results from $EQR.AX are already out! Quarterly production was a bit on the low side, partly due to weather conditions. Nevertheless, due to skyrising tungsten prices revenue was up QoQ. I hope to elaborate more on the quarterly results later today. $EQR.AX traded slightly up last night with 1.72%.

@Stephen11198316 But even Wolfram Camp alone, under another company’s ownership, would probably be worth more than EQR’s entire current valuation. $EQR.AX

In the end, WSB was right again. I really didn’t expect POET to actually be a supplier to Marvell…

I’m long $IQE If you missed out on this stock, like me, now is a good day to load the boat. Down 12% today on no news. Makes for a compelling entry point. Company is a compound semiconductor wafer supplier sitting right in the middle of AI photonics + data center buildout. 2025 revenue came in at ~£97M, top of guidance. Q1 2026 order book already strong. From @ParadisLabs modeling: Rough valuation math at current ~£600M market cap: Base case (7x EV/rev): £727M → £802M → £884M over 3 years Bull case (10x, photonics tailwinds fully priced in): £1.1B → £1.4B → £1.7B No takeover premium in either scenario – and the board is already fielding acquisition offers. If execution holds + AI photonics demand keeps compounding, this could still 2x from here organically. Dips like today are how you build a position.