BM Capital⚡️

1.1K posts

BM Capital⚡️

@BM_Capital_

✋💎🤚 #Bitcoin, $TSLA | 25+ yrs Swing/Instinct Equity Trader | Technology | Blockchain | 30+ yrs Software Engineer + IT Leader

Earth Katılım Ocak 2023

490 Takip Edilen151 Takipçiler

Uber is going to be bought by Google/Waymo, Amazon or Tesla/SpaceX in the next year.

For a “buy it now” price of $250b, one of those three companies gets a $12b a year free cash flow machine with $70b in revenue — and hundreds of millions of global customers

This is the most obvious M&A deal since Instagram, Android and YouTube transformed Meta and Google

Discuss

English

@FinnStockinger Tl;dr : Buy $TRT now before it's too late. For comp look at $AEHR.

English

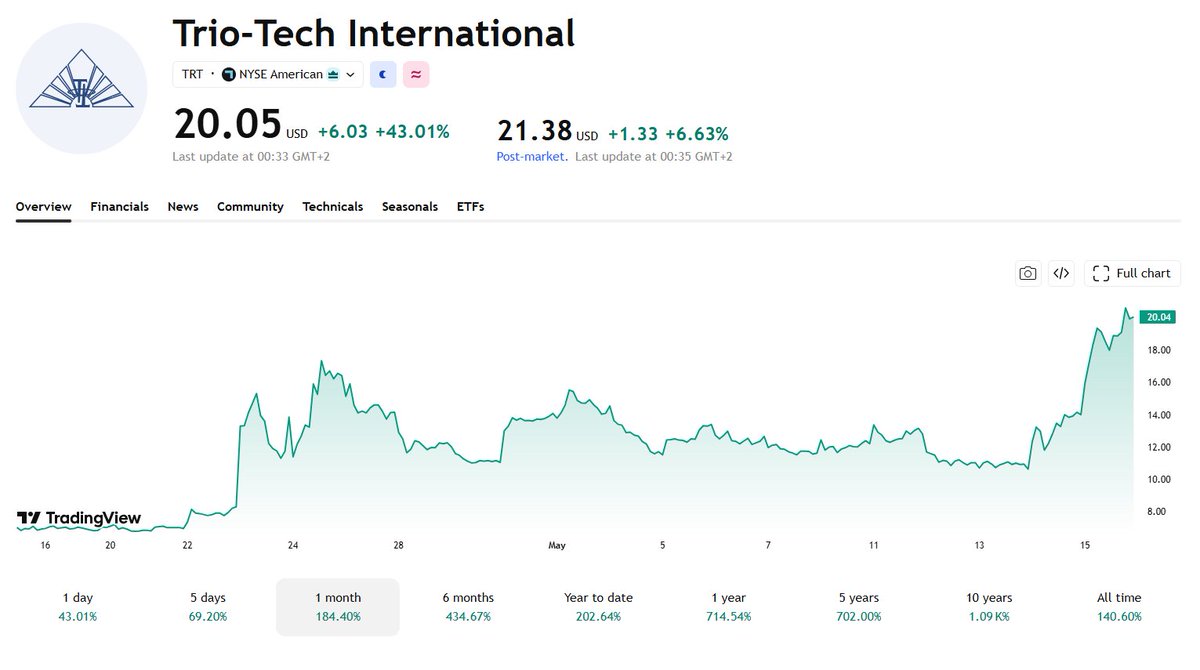

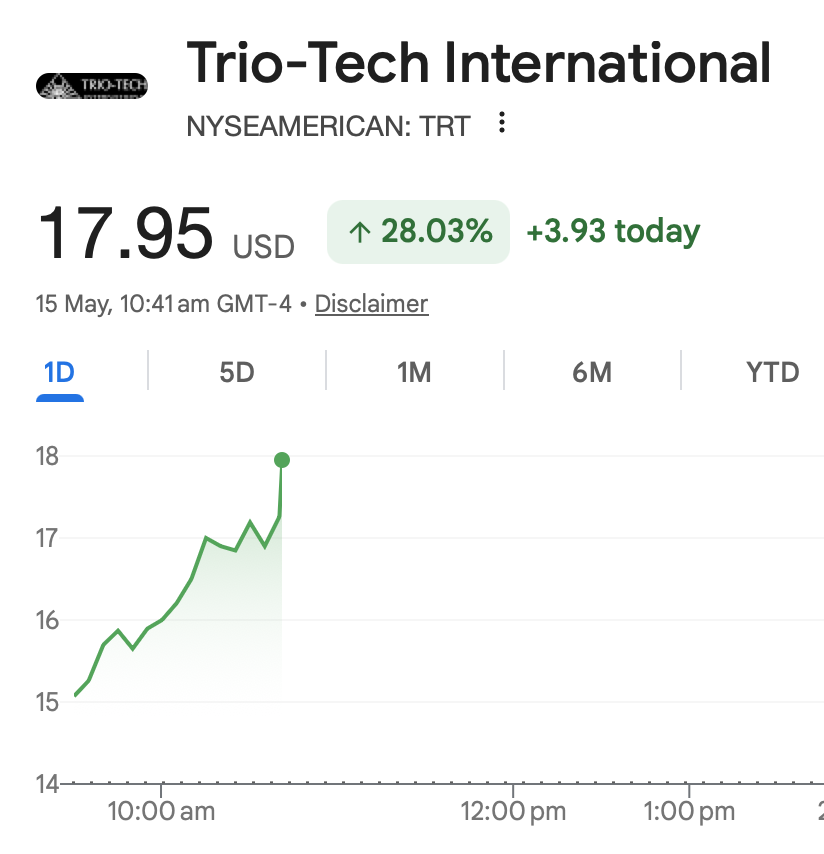

Trio-Tech ($TRT): My Next +100% Bag this Year.

My investing philosophy for 2026 is simple: find the companies that own the un-bypassable infrastructure, buy them cheap, and ignore the daily noise. Trio-Tech ($TRT) fits that description perfectly.

They don't sell hyped-up promises; they run physical back-end labs in Southeast Asia that the tech elite depend on.

After their latest 10-Q filing on Thursday, the stock jumped 40% in a day, locking in a +100% gain for my port.

Let’s look past the sudden price spike and break down the actual balance sheet.

Here is why Trio-Tech International ($TRT) just stopped being an ignored micro-cap and turned into a critical, un-bypassable infrastructure lynchpin for the second half of 2026.

➡️This stock has delivered another +100% for me this year in a relatively short period.

I initiated my first position 23rd April and accumulated on the way up, with a cost basis of ~$10.

I’m not selling a single share.

👇

The Q3 2026 Earnings Anatomy: Numbers Without the Makeup

On May 14, 2026, Trio-Tech published its Q3 FY2026 Form 10-Q on the NYSE American exchange.

The market's reaction was violent - the stock surged over 40% in a single session, tearing past the $20 mark.

To understand if this rally has actual fundamental legs, we need to strip away the market euphoria and dissect the raw financial architecture.

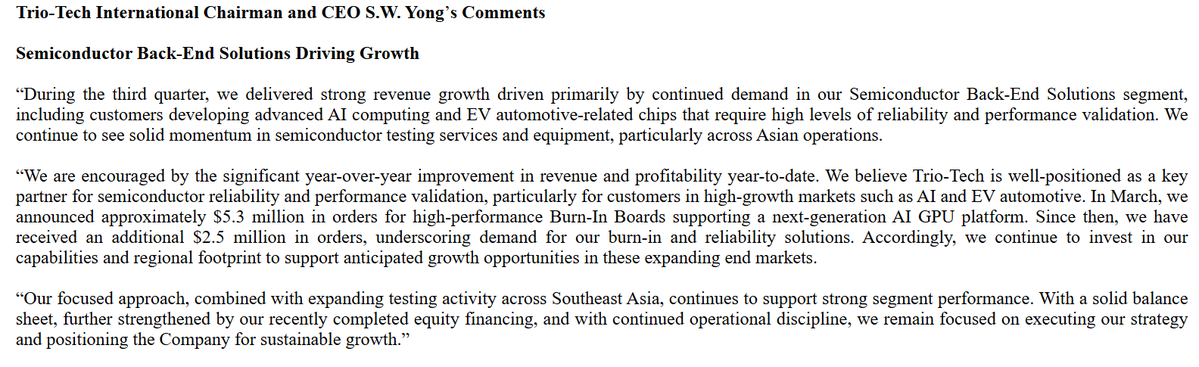

1⃣Top-Line Explosion & Segment Shift

TRT generated $16.51M in revenue for the quarter (ended March 31, 2026) compared to $7.38M in the prior-year period.

That is a staggering 124% YoY growth.

The true magic, however, lies in where this money is coming from:

➡️Semiconductor Back-End Solutions (SBS): $13.08M vs. $5.43M last year (+141% YoY)

➡️Industrial Electronics (IE): $3.43M vs. $2.00M last year (+76% YoY)

Nearly 80% of TRT’s entire business is now concentrated in the SBS segment - specifically final reliability testing and "burn-in" services for packaged silicon.

This is a direct consequence of the insatiable demand for physical validation of AI data center clusters and 800V automotive grids.

2⃣The Gross Margin Paradox: Risk or Scaling Feature?

The bears and basic trading algorithms immediately flagged one metric: gross margins compressed sharply from 27% down to 16%.

In the micro-cap world, a sudden margin drop often triggers panic.

But a granular look at the balance sheet reveals this is a temporary byproduct of massive scaling, not structural decay.

The compression is driven by two highly logical factors:

➡️A deliberate transition into massive, high-volume testing contracts which carry lower unit margins but secure immense aggregate dollar volume.

➡️Mobilization & Ramp-up Costs:

TRT is aggressively preparing its operational footprint for an unprecedented influx of business.

The engineering, logistics, and setup costs are being recognized today, before the new facilities book their first dollar of revenue.

⬇️

Despite this margin pressure, the net loss for the quarter was narrowed to just $38k (compared to a loss of $495k in Q3 FY2025).

The company essentially achieved an operational break-even while expanding at a breakneck pace.

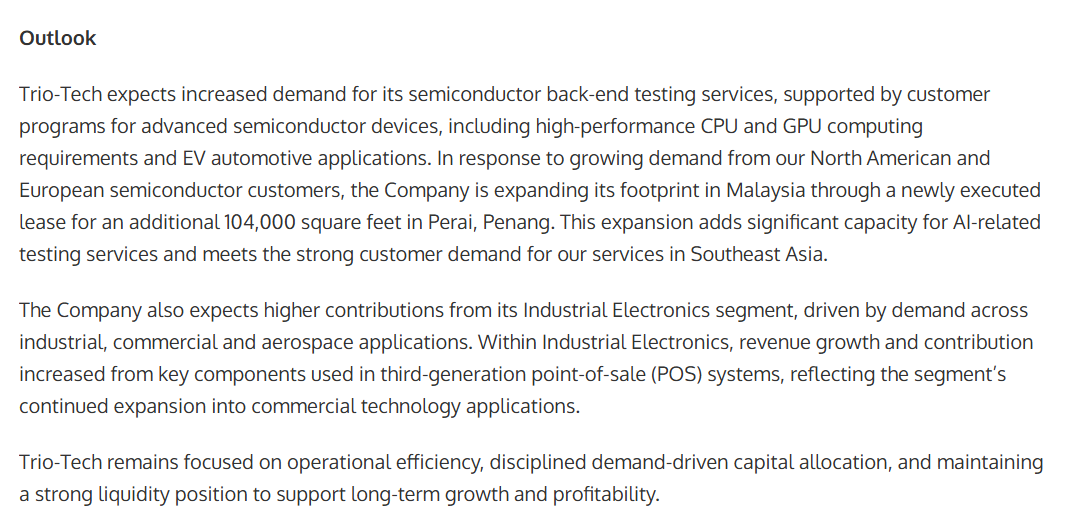

3⃣The Malaysian Masterstroke: Embedding into the Penang Megacluster

The absolute crown jewel of this investment thesis is buried in the company’s regulatory filings from May 2026.

Trio-Tech signed a lease agreement for a massive 104,000 square foot facility in Perai (Penang, Malaysia) at a cost of $115k per month, effectively commencing June 1, 2026.

Let's put that footprint into perspective:

➡️Doubling Global Capacity:

This single facility increases TRT’s global laboratory testing square footage by an estimated 80% to 100%.

➡️The "China+1" Geopolitical Arbitrage:

Western chip designers are desperately trying to de-risk their supply chains by moving back-end processes out of China.

Penang has established itself as the undisputed capital of semiconductor packaging (OSAT) in Southeast Asia.

By placing a 104k sq ft lab right in the heart of this industrial zone, TRT is setting up shop door-to-door with a legendary roster of tech titans.

In fact, $AMD, $INTC, $AVGO, $JBL, $COHR, and $KEYS are all located within a tight 15-to-20 minute drive from new $TRT location.

Instead of packing highly sensitive, multi-thousand-dollar AI modules onto planes to be tested in mainland China or Taiwan, Western tech companies can now complete the entire packaging and final validation loop locally in Penang.

TRT is building the toll booth right outside their factories.

4⃣The Proprietary Moat: Vertically Integrated Hardware

Most testing service companies face a brutal operational bottleneck:

they have to buy their burn-in ovens and test equipment from external vendors, forcing them to pay immense markups and wait in line for tool allocations.

Trio-Tech operates on a fundamentally superior architecture.

They design and manufacture their own burn-in systems, custom Burn-In Boards (BIBs), and hydraulic centrifuges in-house.

This creates a dual advantage:

They don't wait for supply chains.

They can outfit the massive new Penang facility at internal manufacturing cost, dramatically lowering their CapEx requirements.

They do not sell this equipment for a one-time product margin.

Instead, they deploy it internally to sell recurring, high-volume testing services to the biggest names in tech.

This is where the massive operating leverage comes into play.

The lease and fixed overhead costs for the Penang facility are static.

Once the utilization rate of their in-house manufactured machinery crosses the 75% threshold, every additional hour of chip-cooking translates into pure, exponential profit falling straight to the bottom line (EPS).

5⃣A Fortress Balance Sheet Meets Undervalued Multiples

In April 2026, the company executed a registered direct offering, securing $10M in gross proceeds from institutional investors at $9.50 per share.

Retail investors initially lamented the dilution.

In reality, this capital was immediately deployed as the working capital engine required to stand up the Penang mega-lab and execute on their surging backlog, which includes a confirmed $7.8M in firm orders for specialized BIBs tailored exclusively for next-generation AI GPU architectures.

When you look at the balance sheet post-offering, the financial health is pristine:

~$28.3M in total net cash (combining March cash balances with the April raise).

Long-term bank debt: A negligible $255k.

⬇️The Valuation Disconnect

Following the 40% post-earnings surge to around $21, and accounting for the expanded share base (now sitting at roughly 5.1M shares outstanding), TRT's market capitalization rests at approximately $202M.

Over the first 9 months of fiscal 2026, TRT has already locked in $47.7M in revenue.

Even under a highly conservative assumption that the fourth quarter simply matches the current run-rate ($16.5M), the company will comfortably close the fiscal year with $64M in revenue.

This leaves the company trading at a forward EV/Sales multiple of 3x.

Paying a 3x Enterprise Value-to-Sales multiple for a debt-free, asset-owning business that is actively doubling its global physical capacity, while anchoring itself right in the middle of a 15-minute radius shared by AMD, Intel, and Broadcom - is a textbook market mispricing.

At a $10 cost basis, this position offers an immense margin of safety.

The structural fundamentals are moving significantly faster than the stock price.

I am locked in for the long haul, and any macro-driven volatility or short-term pullbacks will be viewed as an open invitation to accumulate more shares.

Finn Stockinger@FinnStockinger

Trio-Tech $TRT: The Final Line of Defense in the AI and 800V Infrastructure Chain Meet Trio-Tech International ($TRT), a company perfectly positioned at the epicenter of the global hardware infrastructure shift. They provide critical high-voltage reliability testing and "burn-in" services for the world’s leading semiconductor manufacturers, ensuring the physical survival of chips powering AI Data Centers and 800V DC grids. Read on to discover why this micro-cap is great opportunity to invest in the 2026 hardware boom. 1⃣Technical Moat: Why $TRT is Not AEHR To understand TRT’s value, one must distinguish its role from market darling Aehr Test Systems (AEHR). $AEHR (Wafer-level): Their systems screen chips while they are still part of a silicon wafer. This is the first stage of filtration—efficient, but not final. $TRT (Package-level): Trio-Tech enters at the Final Stage. They test chips after they have been cut, bonded, and packaged. In the era of AI Data Centers, where a single module costs tens of thousands of dollars, package-level testing is the only guarantee that a chip still holds its parameters after the stresses of the packaging process. TRT acts as the "Final Auditor." They subject finished units to extreme thermal stress (burn-in) and mechanical forces in centrifuges to eliminate latent defects. TRT does not compete with AEHR; TRT closes the loop that AEHR begins. 2⃣Financial Fundamentals: $19M Cash vs. Low Valuation The 2026 balance sheet reveals a rare disparity between market valuation and real capital: Cash Position: The company maintains approximately $19.5M in cash (approx. 32% of its market cap). This provides a massive safety cushion with no significant long-term debt. Inventory Strategy: Inventories have scaled to roughly $11M. This is not "dead weight" but a strategic stockpile of components for their proprietary Burn-in Boards (BIBs) and test systems. TRT has pre-positioned itself for a surge in orders, drastically shortening lead times. Enterprise Value (EV): After stripping out the cash from the $73M market cap, the market is valuing TRT’s global operational business at only $40M. With annual revenues near $40M, you are paying roughly 2.0x Sales (EV/S) for this infrastructure. 3⃣The AI Direction: Infrastructure Over Software AI chips operate under extreme loads and generate record amounts of heat. This drastically shortens their lifespan without proper "seasoning" in the testing phase. Optical Modules & Accelerators: TRT has secured orders for testing boards dedicated to high-speed interfaces and GPUs. Vendor Lock-in: By designing custom test fixtures (sockets) for the specific housing of new AI chips, TRT creates high switching costs for customers, ensuring revenue stickiness for years. 4⃣The 800V DC Standard: Breakout in Automotive & Data Centers The transition to the 800V DC standard is one of the strongest current technological trends, and TRT is positioning itself as a key partner in this shift. ➡️AI Data Center Infrastructure: AI data centers are moving away from low voltages toward 800V DC buses to drastically reduce energy losses when delivering massive power to GPU clusters. Every power conversion module operating at these voltages must pass rigorous reliability tests in TRT’s chambers. ➡️Renewable Energy & BESS: Battery Energy Storage Systems (BESS) and solar inverters are also shifting to the 800V standard to increase transmission efficiency. TRT tests the power semiconductors (SiC/GaN) that manage these flows. ➡️Automotive 800V: In the EV sector, 800V architecture allows for ultra-fast charging. TRT holds unique military-grade certifications (MIL-STD) that allow them to test components for ADAS and high-voltage drivetrains where the margin for error is zero. 5⃣Production Capacity and Cycle Timing The company has completed a period of heavy capital expenditure (CapEx) to modernize its laboratories in Singapore and Thailand. It is now in the monetization phase: ➡️In-House Manufacturing: TRT builds its own centrifuges and burn-in systems. During a boom, they don't wait in line for equipment; they scale their own lines internally. ➡️Operating Leverage: With fixed costs for service centers already covered, any increase in machine utilization above 75% translates into a rapid spike in operating margins and Earnings Per Share (EPS). ⬇️Verdict Trio-Tech is a classic "Deep Value Play" with a massive cash floor. The company has prepared its inventory and infrastructure for the next wave of orders from the AI and 800V DC high-voltage sectors. For the investor, this is a purchase of a critical link in the supply chain at a moment when the market is beginning to realize that without physical reliability, no technological revolution can survive the test of time.

English

@keybodia @farzyness @herbertong @thejefflutz @NickGibbsIAG Everyone will freak out when they book a Robotaxi and instead of Model Y, this one shows up and opens its wings..

English

It really was empty. Real and not generated. not sure how else I can prove it. I can't believe no one is freaking out about this. I was excited to be the first one to see it.

@farzyness @herbertong @thejefflutz @NickGibbsIAG

English

English

$TSLA should integrate Starlink Mini into all cars.. specifically Cybercabs as a standard feature.. very big selling point

Tsla Chan@Tslachan

스타링크 미니, 한국에서 꼭 필요하진 않습니다. 그러나 하나쯤은 소장할만 합니다!

English

@amitisinvesting I thought they would take $X ticker since it was available now

English

SPACEX UPDATES:

- Ticker will be $SPCX

- IPO coming likely June 12th

- Company is focused on expanding retail coverage to international brokerages, not just US based ones

- Looking to raise $80B at around a $2T valuation

Are you a buyer?

I think many other names will be proxies and we are already seeing this with momentum in names like $RKLB.

It’s going to be a historic IPO, question will be where the liquidity comes for it…

English

@yianisz Looks better than $AEHR so it may follow its trajectory now that its discovered

English

$TRT is breaking higher because the market finally realized this isn’t some zero-revenue AI lottery ticket.

You’ve got real semiconductor revenue, operating leverage kicking in, AI/EV testing demand accelerating and a balance sheet that doesn’t need constant dilution to survive.

Small float + real numbers + AI narrative = violent repricing.

Yiannis Zourmpanos@yianisz

$TRT ran hard.. and still looks oddly ignored. You’ve got a ~$120M microcap doing ~$42M+ in revenue, sitting on net cash, basically no real debt pressure and a balance sheet that actually works not one that needs constant funding like most small AI plays. Even after the move, it’s still trading well below typical semi multiples on sales and book, which tells you the market hasn’t fully repriced it yet. Margins are thin revenue dipped in the downcycle… but that’s exactly where the setup comes from. When volumes recover, operating leverage kicks in fast. And now you’ve got burn-in demand tied to next-gen AI GPUs (likely $AMD) showing up in orders. This isn’t a story stock. It’s a real business the market hasn’t fully caught yet.

English

@elonmusk @WatcherGuru and LinkedIn is OnlyFans for Mid-Level Managers

English

@WatcherGuru Obviously.

Sometimes grown men send me their Instagram profiles and I’m like are you transitioning or what?

English

English

Bengaluru just got a little more Electric ⚡

🔋 @Tesla has officially arrived in Bengaluru, Karnataka with its new Experience Center at VR Bengaluru

This marks the opening of the 4th Tesla India Experience Center, another major milestone in @Tesla_India ’s expansion across the country 🌏

You can now experience Model Y & Model YL in person there 🚗⚡

English

@athuinvests Seems like a lot of folks on this thread are just salty they missed this trade..

English

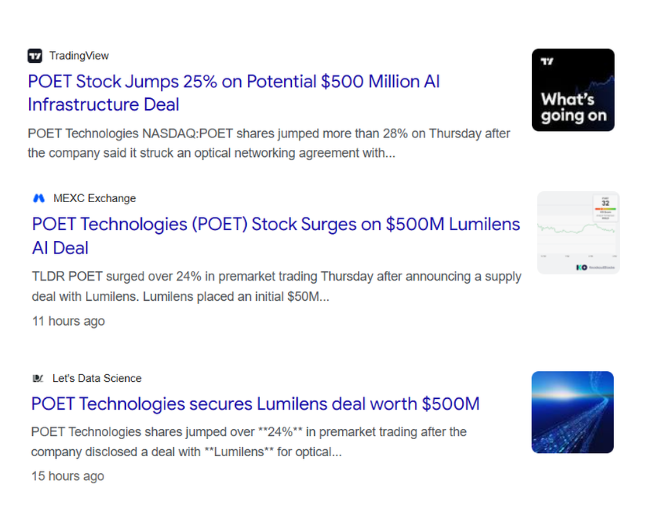

$POET is still a NO for me.

I think you really need to see why.

The stock moved because they signed a $50M initial PO that could scale to $500M over 5 years with Lumilens. But if you see the news headlines, they are already calling this a $500M deal already.

I looked into Lumilens and it is a brand-new 2024 startup: pre-revenue, with no products and no meaningful sales. They just started hiring recently (less than a month). It’s a VC-funded photonics player (raised ~$130M+) promising next-gen AI interconnects.

If you check their website, there is no identifiable product. It is just full of trendy design, words & videos. Have a look yourself if you don't believe me.

$POET already has credibility gaps with a poor track record:

- execution (delayed ramps, canceled deals),

- heavy dilution (share count increase by 4x in 2 years)

- paying $100k to YouTubers to basically manipulate stock price

- it is still a PFIC, and it didn't tell shareholders about that during the 2025 annual report

Two companies with zero mass-production track records signing a big order feels more like mutual hype to me.

Look, the tech narrative is compelling and AI optics tailwinds are real. That is why I am in $SIVE and other photonic companies. But this deal and what I keep looking at makes me even more skeptical.

$POET’s only other disclosed firm order is a modest ~$5M production order from an unnamed systems integrator for 800G engines (shipments H2 2026). Everything else is still in the partnership/qualification stage with no additional firm POs

It is still generating roughly $1M in TTM revenue while sitting at a ~$3B+ market cap. That’s over 2,000x sales. Even if they magically hit $100M this year (which seems unlikely), the valuation is already pricing in perfection.

I just cannot support this until I see actual shipments, real revenue growth, sustainable margins, and - most importantly - better contracts with established customers, not a startup!

Right now it’s still narrative-driven speculation.

Happy to be proven wrong if they deliver, but I’ll wait for real proof.

If I miss out, that’s okay. I’ll take the L.

- AI

English

@tw_crypto_ I have started blocking all who promote their subs/patreons/substacks.. if they are so good at what they say/do, why they need subs?

English

Kevin Xu

- $HIMS was a loss ❌

- $QS was a loss ❌

- Gave up on $IREN ❌

- Multiple pumping post to buy while only risking .5% of his own port

Who is paying $199 a month for this clowns sub? Shameless

Kevin Xu@kevinxu

Call me crazy, but I just made a new trade and its an even bigger banger.

English

It is confirmed. CEO tagging all three (inc. T-Mobile) on their colab..

$ASTS

Abel Avellan@AbelAvellan

Space-based cellular broadband to every American is coming!🤠📶 @ATT @Verizon @TMobile

English

BM Capital⚡️ retweetledi

Palantir-Backed Ondas Stock Jumps. Autonomous Drone Company Sees Revenue Grow 1,065%. trib.al/gHDWJ16

English

Cybersecurity names are starting to break out.

Instead of focusing only on SaaS names, keep an eye on Cybersecurity because this group looks like it may be starting the next leg higher.

$CRWD $FTNT $PANW

Venu@Venu_7_

Cybersecurity names should be on watch here. $FTNT earnings helped lift the entire cyber group and reclaim the 200 day moving average. $CRWD and $PANW - both formed mini bases after the drawdown and reclaimed the 200 day SMA today. $RBRK still needs to do a lot more work.

English

$ONDS 10X revenue beat! I don't own enough..

Revenue: $50M vs. $4.3M YoY (+1,065%) est. $39M beat by 27% ✅

Gross profit: $24.7M vs. $1.5M YoY ✅

Gross margin: 49% vs. 35% YoY ✅

Cash: $1.5B

Backlog: $457M

** FY2026 Revenue: ~$390M 670% YoY increase! **

$PLTR partnership - integrated with newly acquired Skyweaver platform

Ondas Inc.@OndasHoldings

Ondas reported record Q1 2026 results with $50.1 million in revenue, raised its 2026 revenue target to at least $390 million, and expanded pro forma backlog to $457 million. The quarter reflected accelerating demand across counter-UAS, ISR, and autonomous systems markets while advancing Ondas’ global operating platform and AI-enabled multi-domain ISR strategy. $ONDS ondas.com/post/ondas-rep…

English