The God Particle@_Sgr_A_Star

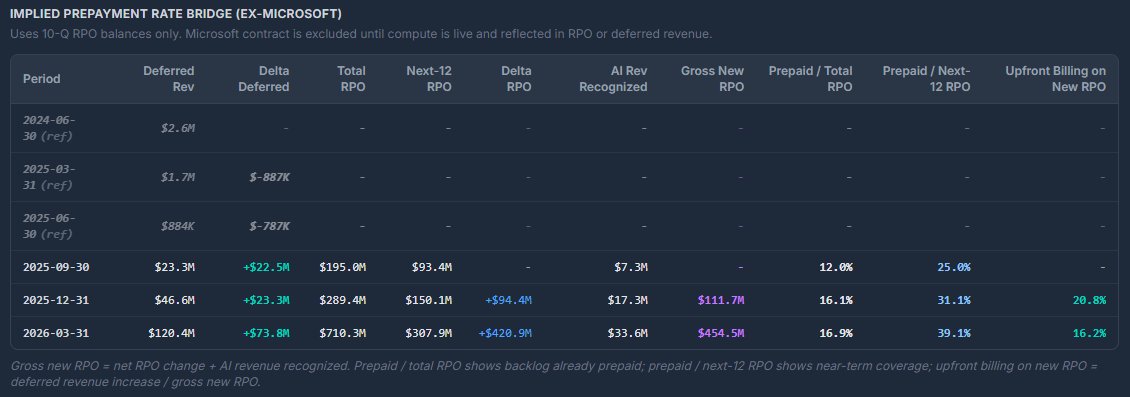

$IREN

I've shared previously that I like to do analysis of RPOs (Remaining Performance Obligations) because it allows me to glean a lot about the business. RPOs are:

- a good proxy for period ending ARR

- insight into size of RPOs

- insight into the shape of RPOs

- insight into contract lengths and avg. remaining recognition

As a reminder, RPOs are the remaining part of a commenced contract that will be recognized as revenue sometime in the future. A contracts value is only added to the RPO totals until the GPUs are delivered.

As an example, the Microsoft deal which is very much legally binding contracted capacity has not commenced and would therefore not be included in RPO totals.

It means that current RPOs only include the contracts associated with the current operational GPUs. Think Prince George and the roughly ~14k operational GPUs as of the end of the quarter.

The 10Q breaks out the RPOs total in 3 time buckets, 1.) future revenue in the next 12 months, 2.) future revenue in months 12-24, and 3.) future revenue in months 25-60,

The table below is my analysis of the RPOs totals over the last three quarters. A few things stand out to me:

1. Although expected, RPOs are growing fast. IREN added 421M to the totals in the last period.

2. The shape of RPOs this quarter shifted. The first two quarters listed had a short(er) duration contract book. Most of all RPOs (95-98%) were within 2 years.

This last quarter changed that. The long-tail mix (25-60 months) now accounts for 19% of RPOs. This signals that for the GPUs that were installed last quarter and their associated contracts, those contracts were longer in length on average than previous quarters. This is likely due to the "lock in" effect going on in the market with how constrained compute is. Customers are much more likely to want to lock-in supply as long as possible, and the long-tail component (3-5 year contracts) is the tell.

3. Because the contract book the last few quarters was so "short dated", it's likely the company will benefit from the recent significant increase in GPU-hourly rates as these contracts end and GPUs re-contracted.

It's early (only 14k GPUs) yet, but this last quarter showed a marked improvement in both the scale and tenor of IREN’s commenced revenue book. While Q1 and Q2 RPO was overwhelmingly concentrated within 24 months, Q3 saw a meaningful 25–60 month tail, suggesting an increase in contract duration and customer "lock-in effect".