@CompoundingLab You’re an idiot who pays for a blue checkmark but can’t figure out that hyperscaler contracts are on the way?

English

Burner

459 posts

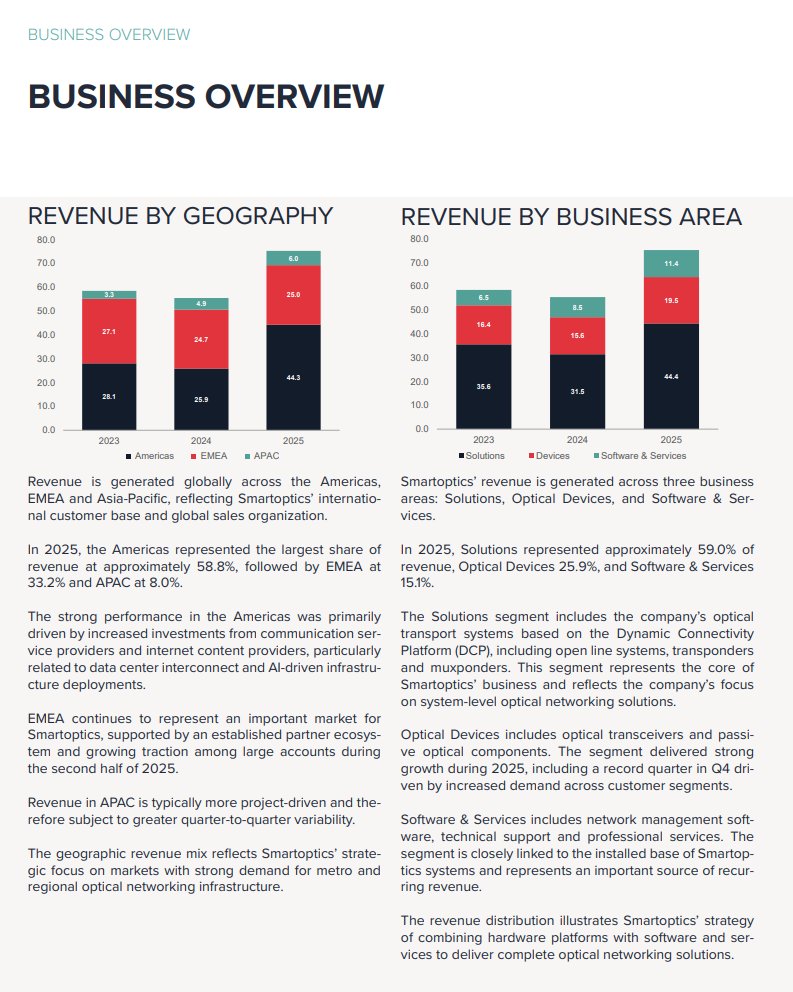

Smartoptics $SMOP.NOL $SMOPF The Other Nordic Undiscovered Optics Juggernaut that may have the most upside since $SIVE Part I Bull Case Thesis: Smartoptics Group ASA (SMOP.OL) – Scaling to a $2B+ Market Cap by 2027-2028 Executive Summary Smartoptics is a high-growth provider of open optical networking solutions (DWDM line systems, pluggable transceivers up to 800G+, and management software) optimized for data center interconnect (DCI), metro/regional networks, cloud providers, and AI infrastructure. Currently trading at ~NOK 4.9B market cap (~$0.52B USD) with 2025 revenue of $75.3M (up 35.6% YoY) and 12.9% EBITDA margins, the company sits at the epicenter of the AI-driven bandwidth explosion. In the bull case, Smartoptics leverages its open, cost-effective, vendor-agnostic platform to capture accelerating share in the exploding DCI/AI optics market. Revenue can compound at 40-60%+ annually through 2027, reaching $200M–$300M+ by end-2027/early-2028, with EBITDA margins expanding to 18-22% via operating leverage and software mix. At a conservative 8-12x sales multiple (well below peers in high-growth AI networking), this supports a $2B–$3B+ market cap within 2 years—delivering 4x+ upside from current levels. This is not a stretch scenario; it aligns with the company’s own 2-3x market share ambition by 2030 and the structural tailwinds already visible in record Q4 2025 bookings and hyperscaler/neo-scaler wins. Company Overview Founded in 2006 and listed on Oslo Børs, Smartoptics delivers disaggregated, open optical networking that breaks vendor lock-in (interoperable with Cisco, Dell, Brocade, etc.). Key offerings include compact DCI-focused line systems (e.g., DCP-M), high-speed pluggable DWDM optics (100G to 800G+), and software for simplified operations. The model is asset-light with high gross margins (~47-49%) and recurring software/upgrade revenue potential. Customers span enterprises, communication service providers (CSPs), cloud/hyperscalers, and governments. 2025 was a breakout year: full-year revenue $75.3M (+36%), record Q4 revenue of $23.2M (+38%), and improving profitability. Massive Market Tailwind: AI Is Redefining Optical Demand The optical transport market reached ~$16.5B in 2025 and is forecasted to grow ~10% in 2026, but the DCI segment (Smartoptics’ sweet spot) is exploding: direct WDM/DCI purchases grew ~40% in 2025, with cloud provider direct buys up ~50%. AI cluster interconnects (scale-out and scale-up) are driving even faster growth—optics for AI fabrics alone hit ~$16.5B in 2025 and are projected to reach $26B in 2026 (60% YoY). Broader optical networking TAM for DCI/cloud/AI is already in the tens of billions and expanding rapidly as hyperscalers build geographically distributed AI training clusters requiring hundreds of fiber pairs and massive 800G+ capacity. Traditional proprietary systems from incumbents (Ciena, Infinera, etc.) are expensive and rigid. Open, pluggable solutions like Smartoptics’ win on cost, speed of deployment, and flexibility—exactly what enterprises, neo-scalers, and even hyperscalers need for rapid AI infrastructure scaling. Competitive Moat and Execution Momentum • Open Networking Differentiation: No vendor lock-in, rack-optimized form factors, and full-stack (transceivers + line systems + software) give Smartoptics a clear edge in enterprise DCI and metro use cases. • Proven Large-Account Traction: Accelerating wins with leading neo-scalers, large operators in EMEA/US, and cloud providers. Customer count and order intake are expanding. • Product Roadmap: 800G+ readiness and software enhancements position it for the next wave of AI bandwidth. • Financial Scalability: Gross margins stable at ~48%, with clear path to 15-20%+ EBITDA as fixed costs leverage and higher-margin software grows. The company has already guided toward 13-16% EBIT margins as it scales share.

Chudthebuilder spends another night out on the town, meeting plenty of free speech-loving Americans 🇺🇸

Everyone’s Using Retatrutide to Lose Weight… He’s Not. Listen to This. 📺: Dr Gabe Alizaidy/insta