The retardant business is basically one of most moated in existence. A plus mgmt have owned it from 10 to 3 to today. Had large chunk of my net worth in it around 5-6. Will probably own it forever. FWIW.

Sell side pretty good for getting up to speed. Stock is choppy but you can just own it basically at any price here.

@patienceisking@haloaerospace I thought their earnings were pretty strong. Think it was bid up on the increased wildfire activity YTD, but as they have demonstrated, their earnings are increasingly uncorrelated with acres burned.

@haloaerospace $PRM No one likes the compensation structure. That said, they have gifted shareholders with fat returns. Q1 is structurally weak too. My cost basis is fairly low so I can stomach the volatility.

@Sher_East_ Ever since they suspended calls their earnings have been a snoozefest. The only notable event this Q is the Somalogic cash hits their books, so it will finally screen as cash rich vs proforma.

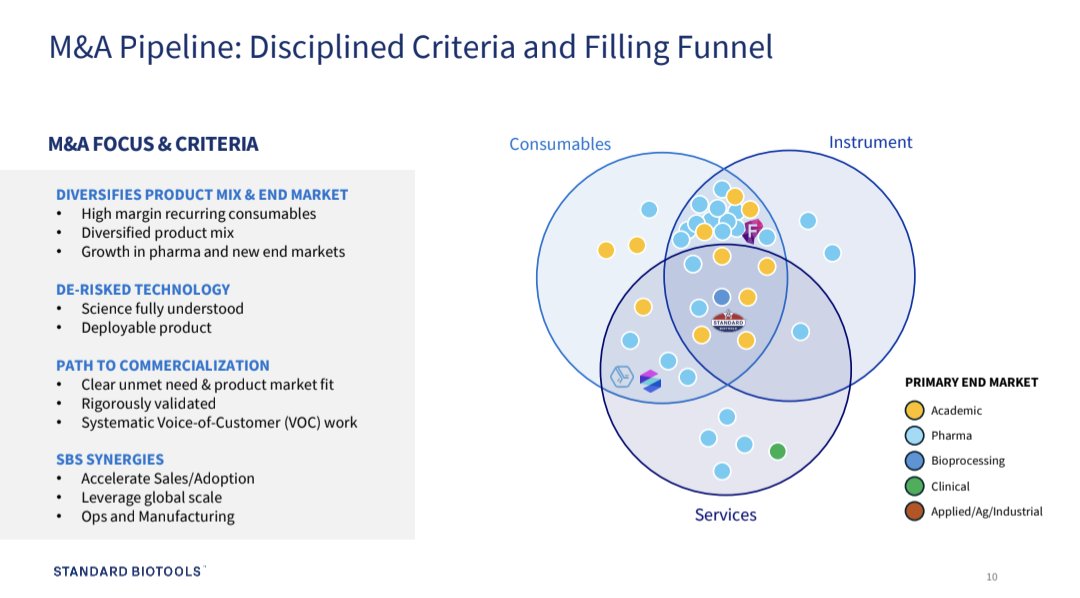

Any $lab owners out there? Standard Biotools, f/k/a Fluidigm, was recapped by Viking and Casdin in April ’22 after a failed sales process. Viking/Casdin backed a private vehicle led by Dr. Michael Egholm (former CTO of Danaher LS) to build a platform for high-impact, sub-scale tools. Their first deal was injecting $250m to reset the business and pursue M&A. 1/

@xiangtaner Couldn't really speculate. They can go in a lot of directions from here. They disclosed a small stake in a VC backed co last Q, otherwise very little info on targets.

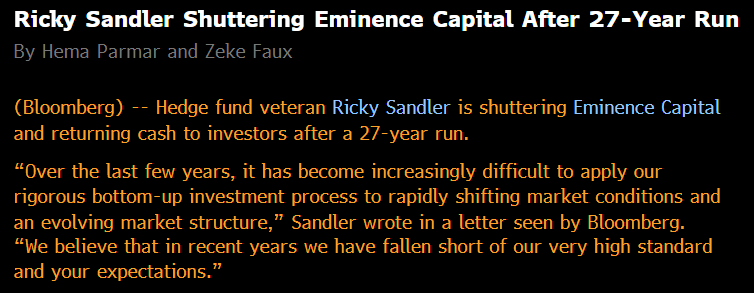

@unciacapital@rsandler21969 I cold emailed @rsandler21969 as a badger alum ~15 years ago to get advice on how to break into investing. He was one of the few alums who called me and was super generous and helpful. Thanks Ricky, great run.

We're launching Sleuth today.

The intelligence platform for biopharma's highest-stakes decisions, in use at top companies in the world.

To celebrate, we broke down the Chinese landscape: 18K+ assets & a map of the strategic white space. RT + comment "Sleuth" for access.

New episode is out! @ElliotTurn and @mihaljevic sit down with Shaun Heelan, CIO of MAAT Investment Group, for a masterclass in PE-style diligence and value investing. Shaun explains passing on Vistry Group and shares a current high-conviction idea. Enjoy!

podbean.com/eas/pb-eiup9-1…

Hard to lose money *permanently* - we're down to 98 cents, 30-35% discount to cash per share inclusive of 2026 burn. Exiting '26 at breakeven on flat revs and already operationalized cost outs.

The key factor is what do they buy and could they destroy so much value via M&A that the margin of safety erodes? I think unlikely given the depth of their pipeline, years of cultivation, the multi-year slog in LS tools putting pressure on balance sheets and bringing in bid/asks.

More likely they buy cash burning tools that take time to work to breakeven, and valuation remains depressed through the digestion period. This sideways case is my downside case, I can't imagine capital impairment from these levels.

I think their experience with Somalogic will push them towards underwriting where the cost outs / lean outs do the heavy lifting.

$lab

The debt agreements impact the event path here. The key provisions are: 1) a cash redemption of the pref is a restricted junior payment under the Alcon term loan to which Alcon must consent. This puts Alcon in in two seats. It is LFCR’s biggest lender and its biggest customer. This means the pref has to jump through another hoop to force liquidation. 2) In a sale of the company, Alcon would receive 115% of obligations due, with a floor of obligations plus $20 million.

So on the margin Alcon’s incentives are likely 1) preserve continuity of $LFCR as a vendor, 2) ensure that the debt is money good, 3) make money in upside from a takeout. This means that they have no interest in letting the pref sweep cash from under them, as it negatively impacts [1] and [2] above.

How does this impact my view on the event path?

If a pref holder gives notice, the clock starts. Payment falls due 180 days later. If LFCR does not pay on that date, the unpaid shares earn 1% per month and dividends keep accruing on shares that remain unredeemed. So absent Alcor consent, any pref holder that gives notice will get more PIK accrual. This is some leverage but avoids the big issue the market fears.

I still think that it is in 22NW interest to provide notice of redemption. But other pref holders care more about upside. So let’s assume 22NW gives notice. What would Alcon do? Possibilities:

1. Alcon says no to a broad cash redemption and lets the clock run. That keeps cash in the business for longer and pushes the fight into a negotiation.

2. Alcon uses a narrow amendment or settlement package to solve for one holder. That could include some cash, some continued accrual, and a litigation settlement. I would not assume this path avoids class-wide issues. The public docs do not give that answer.

3. My most likely case: The exhausted shareholder base + Alcon decide that the rest of the transformation should happen in private and try to sell the company. That would hand Alcon a premium on the term loan, so the sale clause matters. But a sale also turns the question into total enterprise value, not just pref leverage. On a change of control, the pref gets the greater of liquidation preference or as-converted value. Common gets the residual after the stack gets paid.

So my updated view is:

• 22NW is still the natural holder to push

• the other big pref holders have much more common to protect

• the pref can force a process, but it cannot force a cash pull without Alcon

• the debt docs do give Alcon extra take in a sale

• that creates some sale incentive, but not clean proof that Alcon wants a near-term fire sale

• the cleanest “pay off one noisy holder and move on” version of the story looks less certain once you read the pref docs

• this still looks more like negotiation than an instant cash crunch that breaks the common

On the margin I think this all makes a sale more likely than not in the near term. It’s the simplest answer for most parties.

LifeCore $LFCR is up after earnings for at least 3 good reasons

1) EBITDA Margin Improvement - raises floor on EBITDA margins

2) Revenue Growth Coming - Business Wins raise ceiling of medium-term revenue

3) Balance Sheet Improvement - reduces risk

Long Term Path to $40+ ($8 today)

We own it – not a recommendation – do your own work. Share price has a history of poking above $8 and retreating, this time may not be different.

Introducing my new cookbook, Mindful Cooking! Very excited to share that it will be out October 6th, with pre-order available now (link in bio)! This book is all about how cooking with the right mindset can bring gratitude, intentionality, compassion, and ultimately, joy. I hope the simple, delicious recipes, along with gorgeous photographs from my friend and legendary photographer @nigelparryphoto, will inspire you to explore mindfulness and wellness through cooking 📚 🙏 @randomhouse

@Calvsams@GreenhavenRoad i think if the pref holders really thought this was a likely case then they'd be more aggressive and the common would get less.

I agree with your take. I think the most interesting part of this set-up is that you can kitchen sink their guide and still get to $7-8 per share in 2029.

Assumptions:

-HA revs decline $20m and stay flat

-Dev rev small step up, then flat

-Base FF ~inflation like growth -7m lost customer

-Alcon contracted step-up is pushed out and feathered in through '30

-ZERO Phase III trials converting

-ZERO new business

Gets me to ~$160m in revs / $36m in EBITDA in 2029. Implies only 35-40% utilization and thus a higher multiple would be appropriate to compensate for the under utilized lines. But even 15-17x multiple gets you to $7-8/share. + a call option on execution to their base case.

If $LFCR management's 2029 revenue target is even close to reality, the equity is worth more than where the stock traded before the recent drop. I say it in this pessimistic framing because this same price range ($6-7 per share) sits roughly around the current conversion price of the pref.

The stock traded down for some combination of a) some large holder(s) blew out after seeing the push back of timeframe to $200M+ revs or b) the mkt fears that the recent guidance will create a cash crunch driven by forced pref redemption in June 2026. In this scenario the company would be raising equity at distressed prices. This cuts some of the right tail off of the stock.

If it's just (a) and not (b) this is an interesting buying opportunity. I think (b) is an unlikely outcome because it is unlikely to be economically optimal for the pref holders. More below but first the terms of the pref.

The pref PIKs at 7.5%. Conversion price at $6.53 (after the 2024 anti-dilution reset). The liqpref is ~$50m in June of 2026 (when holders can demand redemption). If pref holders demand redemption, payment is due 180 days after notice. Every year of PIK that accrues implies ~$3.6M added to the liqpref which at stable conversion price adds about 550k shares or ~1.3% of current F/D share count.

Four funds control ~90% of the preferred: 22NW (~35%), Legion (32%), 325 Capital (~13%), and Wynnefield (8.4%). This group also owns a large amount of common. Legion, 325, and Wynnefield each have meaningful standalone common exposure beyond what comes from preferred conversion.

22NW has the most relative incentive to play hardball on the pref since its reported exposure is more pref tilted than that of the other large holders.

So long as the prefs (individually and as a class) believe that the long-term value is above the redemption value it makes sense to not redeem. Because 22NW has more pref exposure in absolute terms and in proportion to their common exposure they have the most incentive to take action that harms the common. They will have leverage and I'd expect them to use it. But the pref overall has incentive to preserve common upside.

So long as the pref thinks that the common can get to prices roughly above ~$7 ish in the next few years they should prioritize their position as converted to common. The longer the stock stays near current levels, the more incentive the pref has to act aggressively. This is somewhat tempered by the fact that the majority of the pref as a class has material upside exposure to the common.

So, assume the company achieves its low end 2029 guidance of $212M revs. I give them credit for 26% EBITDA margins since a) mgmt has shown solid cost discipline and b) this revs level means higher utilization means op leverage. So, $55M of EBITDA. Likely conservative given Q4 margins were at 24% with much lower utilization (albeit with dif HA mix). 15x $55M ebitda = $825M EV (-) rough $180M net debt = $645M market cap. Assume 50M shares to credit that pref extracts a hefty fee plus more dilution for mgmt incentives and we're still at $12.90 per share. Importantly the pref holders likely believe the bull case (they own stock, $LFCR can force conversion at higher prices, etc.). So do they have an incentive to take a toll? Sure. But to impair common? I think no.

I think it plays out like this:

- $LFCR performs as described above in 2026. Pref fund provides notice of redemption to start a clock and gain leverage.

- Other pref holders have an incentive to not force $LFCR to raise equity at prices below the conversion price

- This triggers a negotiation that results in a push back of the forced redemption window in exchange for continued PIK, perhaps at a higher rate

- Pref likes this deal because it gives them more upside exposure to the common

If the stock stays persistently below conversion price as the year progresses the pref likely acts more aggressively.

DYODD but I've increased my position meaningfully in the past few days.

@TheNarrenschiff@DivinelyLevered They also have 8 Ph III programs? And a commercial base business with contracted step-up. One med-device program with higher PoS that could do +$25m in revenue by 2030...you can really kitchen sink this thing and still get to $8-10/sh.

@DivinelyLevered $4.50 might be cheap. I don't know. I do know what they're attempting to do building a clinical stage pipeline with small sponsors and bringing the curve forward with larger commercial tech transfers is tricky. I have direct private co experience doing it. Not impossible.

Imagine if people stopped thinking $LFCR was a great business idea that were definitely going to execute in 18 months perpetually into the future and didn't want to pay 20x NTM for it anymore.

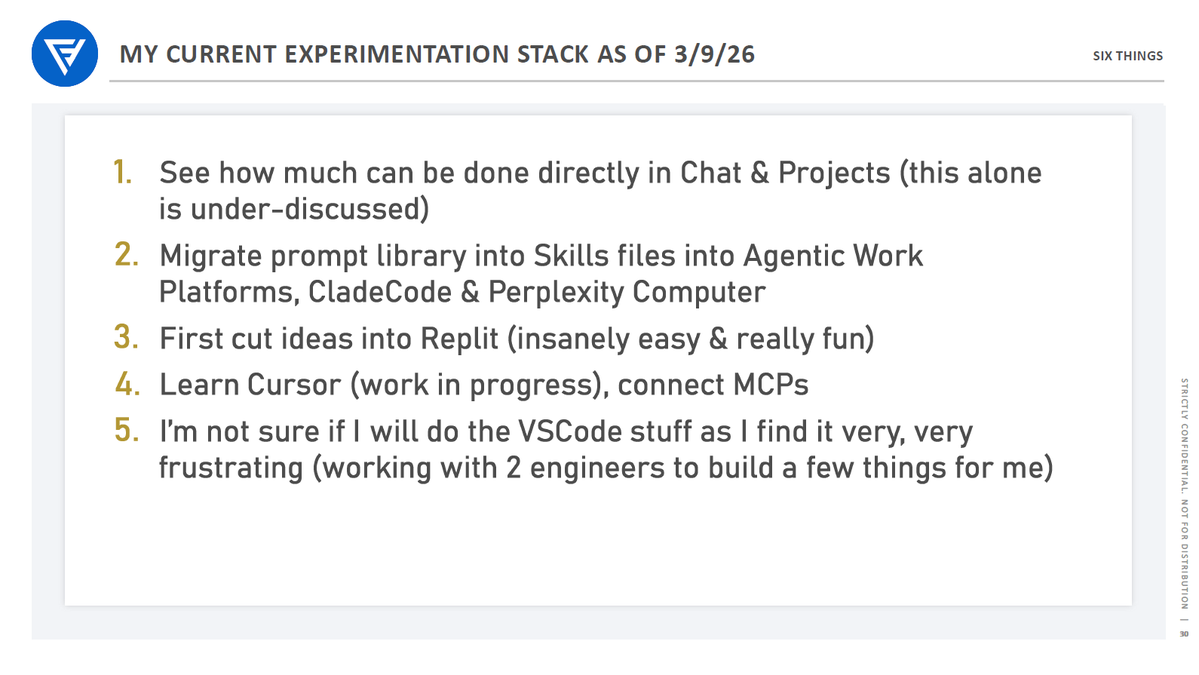

@FundamentEdge I built a risk dashboard with Claude code today. Fetches broker and price data, charts p&l by name, flags anything outside of risk parameters I set…vscode is my go-to, very easy once set-up.

My AI experimentation stack as of March 9th.

Up for any ideas or suggestions!

Maybe I'm just slow, but I have found the VSCode user interface to access Claude Code very maddening. I have found Cursor to be more user-friendly so starting there.

My hypothesis is that the agentic work platforms will improve at such a fast pace that actually won't need to write code for what I do. And hopeful that OpenAI Frontier moves out of enterprise into consumer availability as well.

So far, I've been super pleased with the Claude Co-Work outputs and have found Perplexity Computer to be really helpful as well.

We sent out our Q4 2025 letter. Warning: it's long.

biremecapital.com/blog/the-end-o…

We were +33% for the year, after a rough 2024.

Inside, we issue a broad criticism of the Trump administration's actions across various domains, from its weaponization of DoJ prosecutions, to the corruption of the Trump family's crypto businesses, to the "systematic attack on science and technocracy".

We also go in on what we call "vibe investing", the fact-lite method of speculation that took the number of multi-billion market cap, pre-revenue companies to highs not seen since the 2021 SPAC bubble. $QBTS $JOBY $OKLO $ONDS etc. Amazingly, these stocks still have no material cost to borrow.

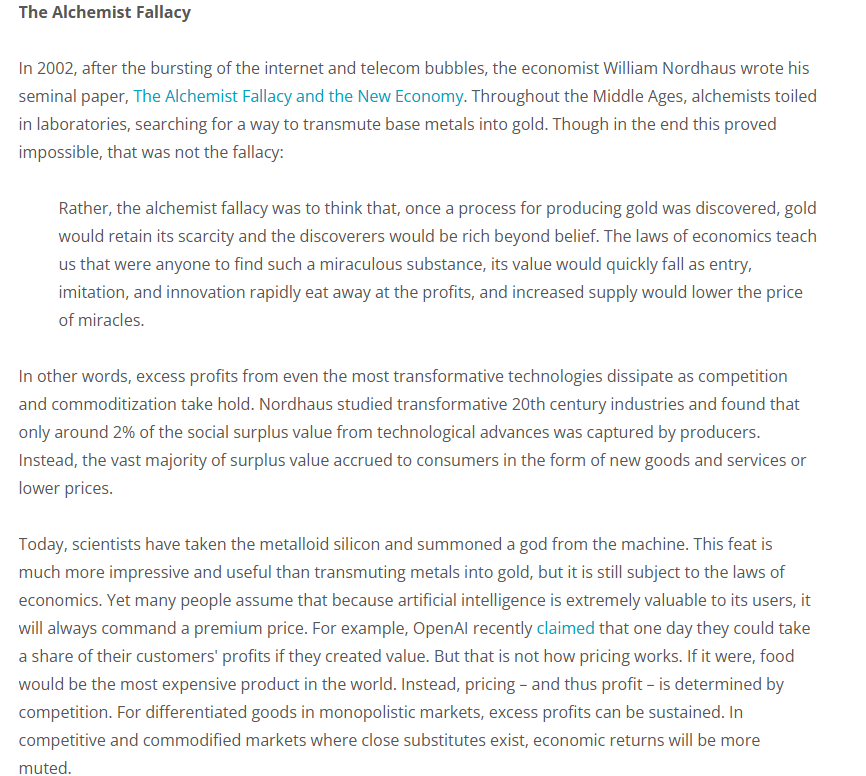

In addition, we share our short thesis on $AAPL as well as give our views on how the "Alchemist fallacy" may pertain to AI-related businesses.

Finally, we describe a few investments we made in 2025, from SoftwareOne $SWON.SW to $PINFRA to $3445.JP and give an update on the amazing run had by Airtel Africa $AAF.LN.

As always, none of this is investment advice and past performance does not guarantee future results!

@ACapitalLP $lab has $1.50-1.60 per share in cash, no debt, plus a business I value at around 30 cents per share. Trades for $1.11. Disconnect because they stopped hosting earnings calls and cash is earmarked for future acquisitions. Hard to lose money at these levels.