Chesley retweetledi

Chesley

616 posts

Chesley

@ChesleyCapital

All Cap Value. Growth and Value are joined at the hip.

London, England Katılım Mart 2019

702 Takip Edilen125 Takipçiler

Chesley retweetledi

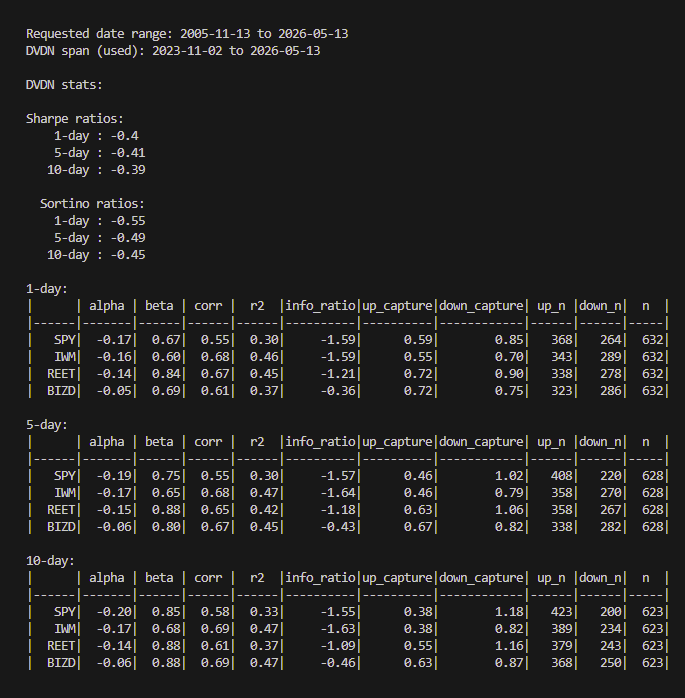

@CRPconnect Lately I've been using Tiingo. I just pull return data and run the calculations myself.

English

@SowingAlphaSeed Are you using nav or price data to feed the calcs?

English

@orrdavid The UK is poorer than every US state: insider.iea.org.uk/p/britain-is-p…

English

Chesley retweetledi

Chesley retweetledi

Most investors play the nicotine pouch trend through $BTI and $PM.

But there's an overlooked sub-category: the EM names. Each is a different angle on the same secular shift; smokers switching to pouches in markets where Big Tobacco controls the local listed vehicle.

$RLX (NYSE), China's vape king turning into a pouch player. USD 2,25B in net cash on a USD 2,6B market cap; you're getting the operating business for almost nothing. 2025 revenue +44% YoY. AirPouch launched, European acquisition in 2025, two-track M&A strategy now explicit. Optionality on Chinese pouch licensing post-2027 and SE Asia consolidation.

$BATK (Nairobi), BAT Kenya. 60% BAT-owned, 40% free float. CFO Philemon Kipkemoi has explicitly guided VELO to reach 15-25% of revenue in 3-5 years. Currently 1%. FY25 PAT +17%, dividend +40% to KSh 70/share for a ~12% yield while you wait. Imports VELO from Pakistan; East Africa demographic tailwind.

$PAKT (Karachi), Pakistan Tobacco Company. 94,7% BAT-owned. Pakistan is the 3rd largest pouch market on earth at 1,13B pouches/year, behind only the US and Sweden. VELO has 85% domestic share and Pakistan now exports VELO to Japan. Tiny 5,3% free float, brutally hard foreign access, but the volume base is unmatched.

$HMSP (Jakarta), Sampoerna. 92,5% PMI-owned. Indonesia's largest tobacco co at 34,9% market share. Selling both ZYN and its own pouch brand Shiro by Sampoerna. PMI built a USD 186M smoke-free factory in Karawang and announced a USD 320M "SuperLab" in 2025; this is PMI's smoke-free hub for ASEAN. 270M people, 60M+ smokers.

The pattern: Big Tobacco quietly building the future of pouches inside locally-listed EM subsidiaries that trade at fraction-of-parent multiples; high yields, structurally different risk, and in some cases take-private optionality.

English

Chesley retweetledi

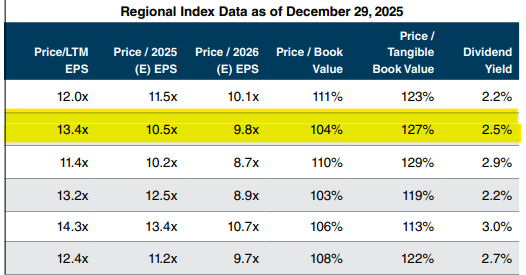

Another post-thrift conversion play to add alongside $LSBK and $ECBK.

- $NSTS is a tiny Illinois-based bank trading below 0.8x TBV

- Owns only 3 branches with weak operating performance

- Upside likely capped around ~1.0x TBV, below Midwest peer valuations (marked in yellow).

English

Love these HoldCo / listed-stake situations where the market is still valuing the company like an operating business instead of doing basic SOTP math.

What other HoldCo structures are out there?

$DK / $DKL

$EXOR / $RACE

$NWSA / $REA.AU

A Capital@ACapitalLP

Has anyone looked at $RILY lately? They are equitizing debt, cleaning up the balance sheet, and quietly turning the business around. If you strip out the $400mm+ $BW stake and the rest of the securities portfolio, the core business is trading at <4.0x…

English

Chesley retweetledi

$IBKR in 2022 was one of my most successful investments, 4 bagged in only a couple of years and I had it @ max position size

$D.MI feels very similar today, though I am early in DD.

English

Chesley retweetledi

Special situation time in Korea. Not many public company spin-offs happen in Korea, but we have an upcoming one on July 1, 2026. Tovis, 051360, is an industrial monitor and automotive display business that will be spinning off the automotive display business into a stand-alone, publicly traded company called Neoview. Recent disclosures allow us to finally analyze each stand-alone business separately and see the hidden value. Friendly reminder to DO YOUR OWN DUE DIILIGENCE and this is not an investment recommendation. If you would like a detailed write-up, please DM me. @MikeFritzell @ClarkSquareCap @douglaskimkorea (1/7)

English

Chesley retweetledi

$QBY.DE German Mittelstand IT business, €90m mcap.

- 42.2m net cash and growing. Buybacks / dividends will start in August (47% mcap), tender offer?

- 5MW own datacenter in Hamburg: AI for German SMEs, considers disposal, worth another €50-60m? (61% marketcap) more buybacks or divs?

- IT core business 2026E guidance: Sales €182-190m, EBITDA €10-16m another 50-100% marketcap?

- founders own 25% and approach retirement age in DE (66), rest FF. Will be acquired in next 12m? Obvious one for PE.

English

Chesley retweetledi

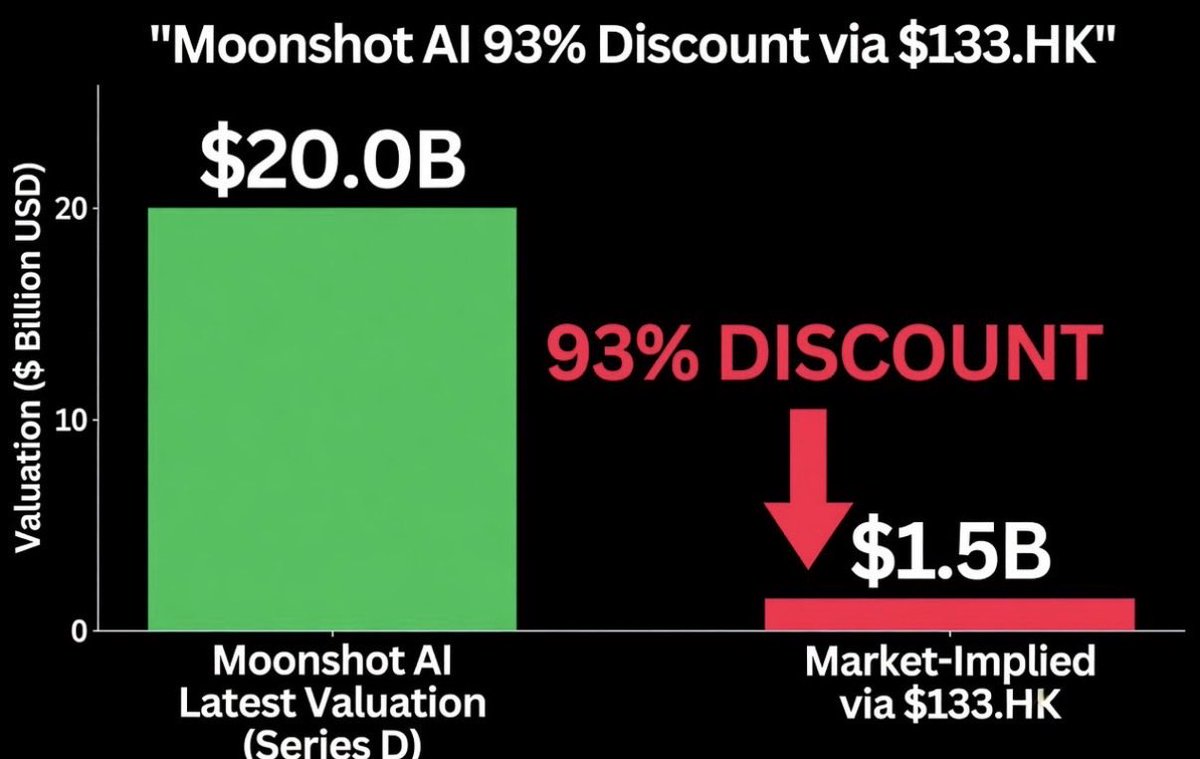

We like $133.HK, it’s a time machine that gives investors exposure to China’s leading agentic AI model associated with Cursor/SpaceX at a $1.5bn valuation. Thanks to activist involvement, you also get paid an 8% dividend yield to wait for the re-rate. Full writeup: maiuspartners.com/p/back-to-the-…

English

(12/12) Risks are limited thanks to strong cash generation, net cash position and regulatory protection. Catalysts are tangible and near-term: better reporting, buybacks, JV resolution, and re-rating in a stock with little analyst coverage.

Thanks @HugoNavarroPer2 for the idea and Fredrik Bergman (Aktivisten) for the amazing public research on the company.

This is not an investment recommendation, just sharing for my co-investors at Meridion and anyone who could be interested.

English

Chesley retweetledi

(1/12) 🆕 investment thesis on a great opportunity I found in the Nordics. Long with a mid-sized position at Meridion. Let’s fly to Finland ⏩

Oriola $ORIOLA.HE is the leading provider of pharmaceutical distribution and wholesale services in Sweden and Finland. Market cap of ~€170M on the Helsinki stock exchange.

It operates in a regulated duopoly with >40% market share in both countries.

English

Chesley retweetledi

I believe this works in apps script:

function yahooQuote_(symbol) {

try {

const url = "query1.finance.yahoo.com/v7/finance/quo…" + encodeURIComponent(symbol);

const r = UrlFetchApp.fetch(url, {muteHttpExceptions:true, followRedirects:true});

if (r.getResponseCode() !== 200) return NaN;

const j = JSON.parse(r.getContentText());

const res = j?.quoteResponse?.result?.[0];

const p = res?.regularMarketPrice;

return (typeof p === "number") ? p : NaN;

} catch (_) { return NaN; }

}

English

Chesley retweetledi

Available now. I was honored to write the foreword for the 25th anniversary edition of Life at the Bottom: The Worldview That Makes the Underclass by Theodore Dalrymple.

As you can probably tell from the title, the book is about life at the bottom of society. Not just in terms of money but in terms of behavior, values, and daily choices. Drawing on his many years working as a doctor with prison inmates and patients in low-income neighborhoods, Theodore Dalrymple describes how violence, addiction, broken families, and despair are sustained not only by material hardship but by ideas that excuse bad behavior and reject personal responsibility.

Dalrymple challenges a comforting story. Many people believe poverty is mainly about a lack of resources or unfair systems. This book argues that culture and norms matter just as much, sometimes more. When society stops expecting discipline, self-control, and accountability, the people who most need those guardrails suffer the most. I read the original version of Life at the Bottom about a decade ago when I was in college. One of the most important books I’ve ever read. Writing this foreword for the 25th anniversary edition feels like coming full circle. First living the world Dalrymple describes, then discovering his work in college, and now helping to bring it to new readers.

Strongly recommended. It is available today.

Get your copy here: us.amazon.com/Life-Bottom-Wo…

English

Chesley retweetledi

English

@ExpectedValues @twaddle_inc @JamesTraylor25 @DarkfireCapital Tbh I never purchase one. I relied on Indian instructors on YouTube.

English

So I've read Ted Warren's book "How to Make the Stock Market Make Money For You". Any other book recommendations for learning technical analysis.

English