Del Griffith

4.4K posts

Del Griffith

@Del_Griffith0

Cereal Entrepreneur, I sell shower curtain rings worldwide. Flunked out of Harvard Business School Online.

Cedar City, UT Katılım Mayıs 2024

263 Takip Edilen269 Takipçiler

But I do. When I get home every night. I leave my phones inside my bag and just leave them there. Sometimes I look at it but only when I go into the desk in the living room.

The phone does not belong in the bedroom. If you leave the phone in the living room, you will find that your life is more peaceful and your sleep is better.

If you have children, the best thing is not to look at your phone because you are telling them that it is more important than interacting with them & THEY TOO SHOULD GET A PHONE.

Kim ⭐️@KimResearch_

@Trinhnomics Easy to nod along, harder to actually toss the phone out of arm's reach for 48 hours.

English

U.S. whiskey volumes fell 1% in 2025 and barrels in storage rose 10%. This is no way to live $bf.b

English

Today's system taxes labor > capital > inheritance whereas changes in the economy increasingly argue for one that taxes inheritance > capital > labor.

English

AI is doing ~0% of workloads at practically all non-software companies

English

Anthropic needs to solve the computer/power problem or they will be the Friendster of the AI era.

I just ran a semi-complicated stock screening prompt on all four major AIs: Grok, Gemini, ChatGPT and Claude.

The first three returned comparable results. Claude refused to do the work.

Not the way to win guys…

English

What in the world is going on with Charter? Down one third in five days. $CHTR

Gary@garyHeff

Time to look at $CHTR ? Have all the bulls gone extinct yet ?

English

Berkshire famously has had wonderful experiences with airlines and retailers

WSJ Markets@WSJmarkets

Berkshire Hathaway took new positions in Delta Air Lines and Macy’s during its first quarter with Greg Abel as chief executive on.wsj.com/4uRhKzA

English

@johnarnold @nytimes Kids stuck on their phones and social media - US will be a shitshow 30 years from now

English

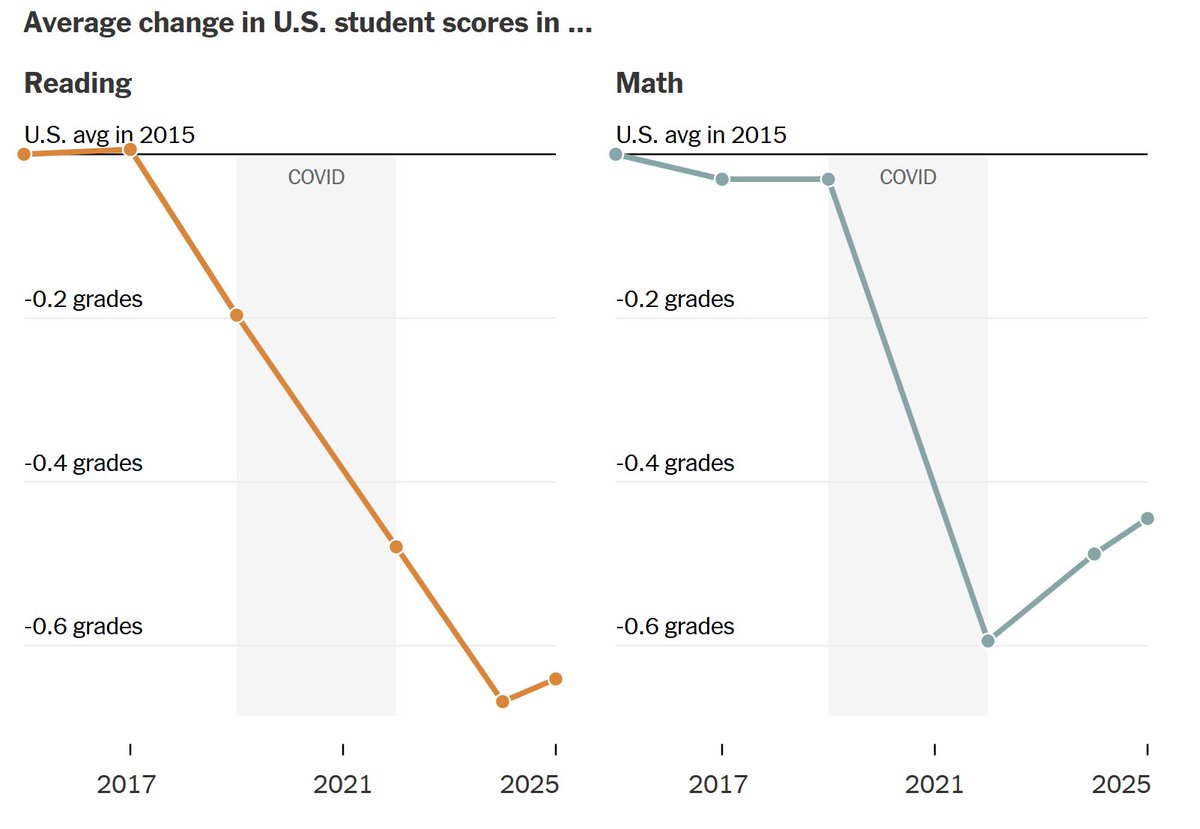

The societal trend I’m most worried about these days is also one receiving very little attention from policymakers, most of whom would rather talk about anything other than schools.

graphic via @nytimes

English

@INArteCarloDoss Too busy banging all the guys at the White House

English

@sourcesandmuses @blueprintsmb22 Obviously you’re not in the AI deal flow

English

I was focused on eastern US, but generally looking all over if it checked all my other boxes (narrowing down industry focus helped here). The one I have under LOI right now is an hour away from me now in NYC so I lucked out, but was definitely more aggressive in locking this one up due to location.

Beyond focusing on getting that one closed and my add-on pipeline, the deals hitting my inbox are all just quick passes. A lot of guys in my peer groups of searchers / indy sponsors echoed the same as well

English

30-year JGB is 4% and 30-year UST is 5.08%. Brace yourself.

Trinh@Trinhnomics

Good morning, US Treasury 30-yr yield is now 5.06%. That's globally consequential, especially on the back of JGB yields rising too. Now, if you are an EM that has a current account deficit and need capital account surplus to offset, you should think, what's the right amount of compensation I am offering for higher risks? As in, risk premium on the rise.

English

Does anyone have an opinion about what we won from China this summit. Preferably something actually announced but happy to entertain something that was won in the non public "back room"

English

@VolatilityVIX He blocked me for no reason - he deserves to be shut down

English

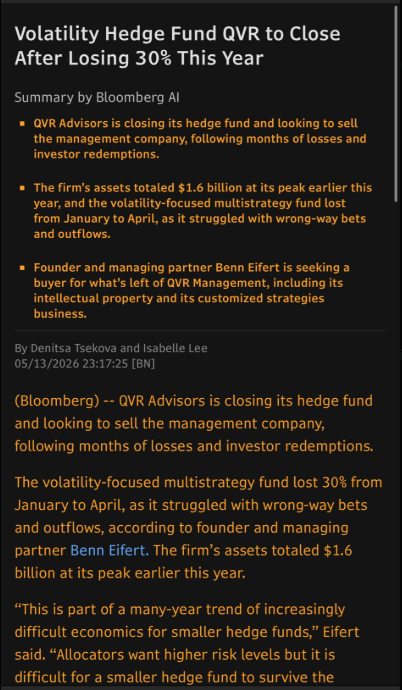

Final thoughts on QVR

There's definitely a healthy amount of dunking on Benn Eifert for losing his fund, and no doubt a lot of it from people who don't manage capital and wouldn't be able to build a fund that size. Twitter naturally brings out haters

Having said that, I do think there may be a lesson in all this hate we are seeing come out, seemingly quite suddenly...

Personally I feel for the guy, and full disclosure, I've had a 29% drawdown myself (granted, it was in 2022 which was one of the most difficult environments ever) but it happens...

If you trade long enough, even the best strategies will encounter a market environment that humbles it

But the main reason people out there are dunking on him isn't the performance this year or the fund itself

It's that he was well known for aggressively attacking people / blocking who disagreed with him. I always had good encounters with him, but I get a lot of people ask me about him and a lot of those questions are, why does he have to be so rude?

There's a lesson in there!

Education is great, and NO DOUBT Benn Eifert was one of the better sources on Twitter for that. He helped a lot of people and put out content that got people excited to learn about Vol trading. In that respect, you simply can't deny his importance to the industry. For years his name has basically been synonymous with "Volatility expert"

But.... at the same time, you don't have to be a dick when educating people

I've done over 1000 articles, 500 videos, 100's of hours of open livestreams with no moderators, no blocking, no arguments. Just me, open invite to anybody, I answer everything respectfully

It is possible to be a top educator and also understand that everybody starts at a different point

Some people know quite a bit, some people don't know anything, everybody is at a different stage of their journey

A good educator knows there are no dumb questions, and EVERYBODY is entitled to their opinion. If some of those opinions happen to go contrary to one of your own, so be it, that's life

The best educators are the ones that can explain complicated subjects to an uninformed audience, and get them excited to keep learning

Benn was / is a great trader and he will no doubt land on his feet with a new fund, my guess is quite soon

And mark my words, it will be popular when he does, and investors will buy into it

Stories of his downfall are greatly exaggerated, he will be stronger for this going forward

But let's just hope he can have a little more humility in his genius the next time around. He's as smart as they come, but a little kindness and patience goes a long way in this world

English

Another one! MUFG wants to offload $2bn in private credit risk. When banks sell, pay attention!

English

@Trinhnomics Any country for that matter running large deficits - look at the UK

English

Good morning,

US Treasury 30-yr yield is now 5.06%. That's globally consequential, especially on the back of JGB yields rising too.

Now, if you are an EM that has a current account deficit and need capital account surplus to offset, you should think, what's the right amount of compensation I am offering for higher risks?

As in, risk premium on the rise.

English

If public, high quality software stocks with low leverage are down 60%+ from highs, the private market ones which are lower quality and higher leverage have to be down even more than that. Tough times in software PE land

English

They’ve got their little toy soldiers marching in lock step tonight…

Nothing good needs to happen in total secrecy

Robby Soave@robbysoave

We need to have data centers. I don't know what else to tell you. We should have them without eminent domain or tax breaks or other forms of corporate welfare. But we are going to have them.

English