English

Tim

11.4K posts

@GreatDecoupling

Anti-nuclear war Pro-nuclear energy

FDA has issued 7 warning letters linked to 20+ violative products with concerns about GLP-1 and other products sold to consumers marked for “research purposes” or “not for human consumption”. These products may pose serious health risks. Do not use or purchase unapproved GLP-1 products marketed for research purposes. fda.gov/inspections-co…

The world has no choice but to take the cyber threat associated with Mythos seriously. But it’s hard to ignore that Anthropic has a history of scare tactics. Examples:

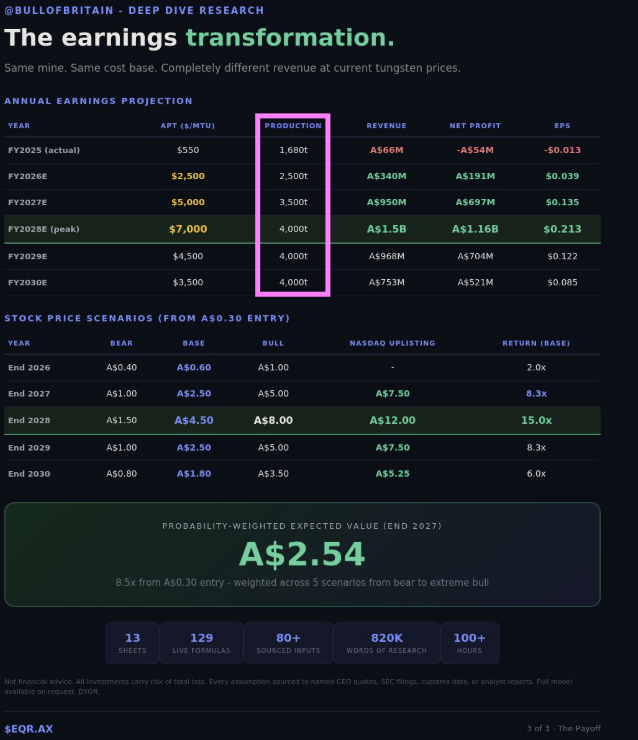

$EQR.AX Updated - Final model with 3,000% upside I spent 100+ hours building what I think is the most detailed $EQR.AX model in existence. 820,000 words of research. 13 sheets. 129 live formulas. Every input traced to a CEO quote, SEC filing, or customs document. The price projection based on CURRENT trends since 2025, projected scaling, all known catalysts, comments from every known Tungsten/industry professional with a 3-5 year timeline. The earnings table showing A$66M revenue transforming into A$1.5B at peak. The stock price scenario table from A$0.30 to A$4.50 base / A$12.00 Nasdaq. The probability-weighted EV of A$2.54 in the green box. And the model stats bar at the bottom. I've used all relatable Nasdaq uplisted Tungsten companies and their respective average volume increases and applied it to $EQR.AX as an industry standard on where it would put the stock relative to its intrinsic value. This also includes other industry bottlenecks and what the market prices their premiums as such. It has transcipts from CEO Craig Bradshaw in various seminars, youtube videos and earnings reports. This includes sections of Production, Contracts and Commercial info, Balance sheet / Corporate speak, Exploration and expansion (such as Wolfram), CEO sourced Market Data and Competitor data (ALM, China buying African/Bolivia mines to squeeze the West more) Lastly Third-party data from industry professionals and community members such as @Alexsei88, @UnnajaSnoop, @METhompson72, @el_miikka, @Fibonazzo, @AdventusCEO and @88_becks. Why the Western supply demand is broken and why Tungsten has no real ceiling based on price inelasticity. The West has completly relied on the back of Chinese material pricing and supply for so long, that it got so complacent that it shut down its majority of domestic supply. These are things such as exploration, funding and governmental backing, which have stemmed from net-zero and eco friendly narratives. Now China are shutting the tank, the West has finally realises the situation it has created. They had no substitute for this outcome from sheer ego and lack of intuition to pursuit social issues rather than physical. This entire situation has left a gap which can be mathematically obvious if only you just look at a few numbers. TOTAL WESTERN SUPPLY 2026: 17,940 2027: 22,100 2028: 26,000 2029: 31,000 2030: 34,300 TOTAL WESTERN DEMAND 2026: 24,900 2027: 31,100 2028: 34,900 2029: 37,250 2030: 40,200 Defecit: 28% Tungsten market is growing by a CAGR of 8%. Western defence being 7-8%. AI being 19-30%. CAGR of production volume? 4.7% to 4.9%. If you know anything about compounding, you can see where this is going. Supply EQR (Australia + Spain) ALM — Panasqueira (Portugal) ALM — Sangdong Ph1 (S. Korea) ALM — Sangdong Ph2 (S. Korea) ALM — Gentung (Montana) Wolfram Bergbau (Austria) Group 6 Metals (Tasmania) Tungsten West (UK — Hemerdon) Guardian / BMM (USA) Mactung (Canada — Fireweed) Recycling (Western) Vietnam (Masan — grey zone) End-use and % of demand Defence / munitions (11-14%): W = 10-20% of shell cost. NDAA mandates procurement regardless of price. Zero recycling. 1% military increase = 2% market increase because munitions aren't recycled. Oil & gas drilling (10%): W cost = 0.2-0.5% of driller profits at $300. At $3,000 = 2-5%. But oil doubled too, offsetting. No drill hole without tungsten carbide. Semiconductors — WF6 (3-4%): WF6 per wafer = tiny vs $20K+ wafer value. 200-layer NAND = 200 depositions. Samsung reportedly out by June 2026. No substitute for CVD tungsten in sub-22nm. Semiconductors — wire cutting: Tungsten wire yields more chips per wafer than diamond wire. Less swarf, thinner kerf. PV industry switched because economics were better even BEFORE the price spike. CNC machine inserts (25%): Insert = fraction of $500/hr machine rate. Nobody stops a factory over a $5 insert becoming a $50 insert. Redesign to non-W takes 3-5 years. Nuclear fusion (new): ITER divertor = 432 tonnes of tungsten. Government-funded. No substitute — only material surviving plasma-facing conditions. ITER started series production. DEMO, STEP, SPARC follow. PV tungsten wire (new, +198%): 4,500t demand in one year from near-zero. 20%→60% penetration. Solar deployment doesn't stop for tungsten prices, it's mandated by climate policy. Li-tungstate batteries (new, +300%): 12,000t demand. Solid-state battery core material. EV transition depends on it. Li₂WO₄ as electrolyte additive. Mining & construction (26%): Every drill hole needs tungsten carbide bits. Every excavator tooth. Every crusher liner. Mining doesn't stop because tungsten is expensive, it's the input cost of extracting everything else. Catalysts and timelines 2026 May-June: Samsung WF6 supply reportedly exhausted. Semiconductor tungsten crisis headlines. June: EQR debt fully repaid. Bradshaw: 'Expect to generate significant cash. July: Mt Carbine expansion board approval + construction begins. A$30M spend, equipment purchased. Sep-Oct: H2 FY2026 full earnings. EBITDA massively positive. Revenue A$200-350M+ for H2. Sep-Oct 2026: Bank coverage initiations. BofA did ALM in March, EQR is the logical next call. 2027 Nov 26-Feb 27: Mt Carbine expansion operational. Production steps from 2,500→3,500-4,000t. Jan 1, 2027: NDAA goes live. Chinese tungsten BANNED from all US defence contracts. No workaround. H1: AVDS/Cadence/institutional accumulation. ETF inclusion. Possible analyst day. Possible Nasdaq/NYSE uplisting announcement. GMTL +43% in 2 weeks on listing. ALM +200%. H2: Peak scarcity. Defence + semis + fusion. Thompson: 'rhodium-like move'. APT $6-10K+. 2028 New supply: ALM Ph2, TUN, Fireweed/Mactung beginning. Recycling at 6-7K tonnes. Takeover risk. Major miner or defence prime bids for EQR. When supply chain = 2 companies, buy them. 2030 Fusion fleet procurement (DEMO, STEP, SPARC). Permanent demand Pool 3. The general consensus from all the talks I've had with industry professionals and rare metal investors gives a timeline of 3-5 years minimum to re-engineer away from W in any application. Most applications have NO substitute at all. Companies will pay anything for 3-5 years rather than redesign. (AI Capex, 1.5 Trillion U.S. Defence spending) Once again. This entire post has been modelling on a framework of CURRENT day trends. Any fluctuation upward or downward will compound these results massively and will vary differently. Thank you for reading and enjoy the gains. This will most likely be my last long form Tungsten post unless anything major happens. Let's ride. 💥#Tungsten 🍀 NFA. DYOR.

Someone out there seems to know that an LLM is not an AGI, nor will better LLMs ever be AGIs.

Introducing Project Glasswing: an urgent initiative to help secure the world’s most critical software. It’s powered by our newest frontier model, Claude Mythos Preview, which can find software vulnerabilities better than all but the most skilled humans. anthropic.com/glasswing

Claude Mythos is Delusional

The duality of man