JoHnL

22 posts

JoHnL

@JohnL_im

Microcap investor, amateur writer, Skills status: Loading... Just trying to beat the indexes without blowing up my account

Katılım Mart 2023

109 Takip Edilen10 Takipçiler

JoHnL retweetledi

Press Release: @CarrierCDS | $CCDS.V $CCDSF

Carrier Connect appoints Mark Alexander as Chief Revenue Officer

- Ex-Purolator commercial sales leader

- Focus on revenue growth, retention & pricing

- Strong track record in pipeline + execution

Adds real commercial depth as platform scales

Press Release: tinyurl.com/4d7px474

#CCDS #AI #DataCenters #MicroCap #DigitialInfrastructure

English

@thewatsonview liquidity begets liquidity, oil contracts is exciting, can't wait

English

Posted new update on Abaxx on WSB

reddit.com/r/wallstreetbe…

English

@PythiaR All good valid points. I think OM translation (meant more EBITDA than EBIT margin) depends a lot on consumables and multi-system which are less sales intensive. To me there’s a path where no more than $10-15MM of dilution is left before positive CF, but it’s a question mark now.

English

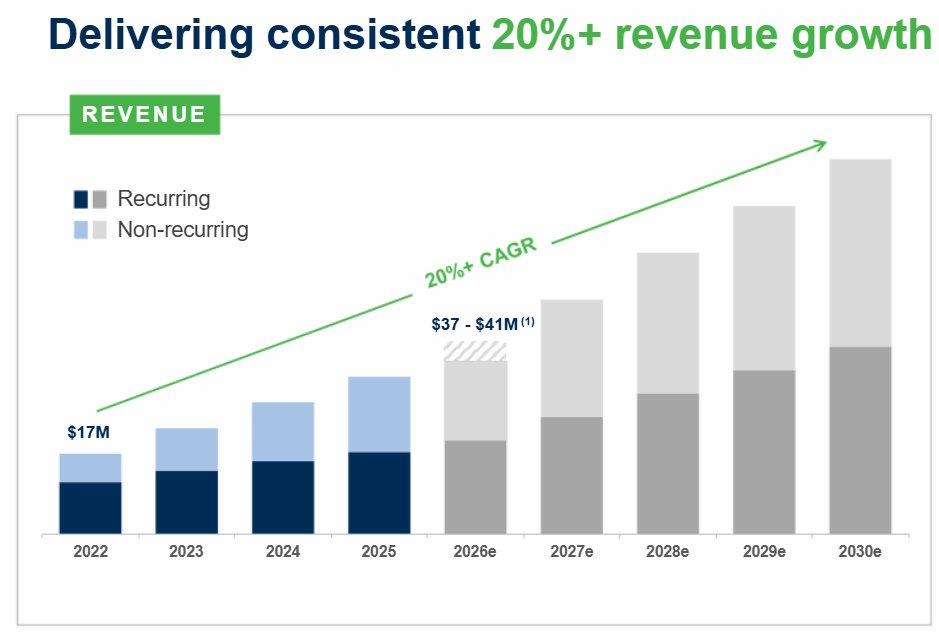

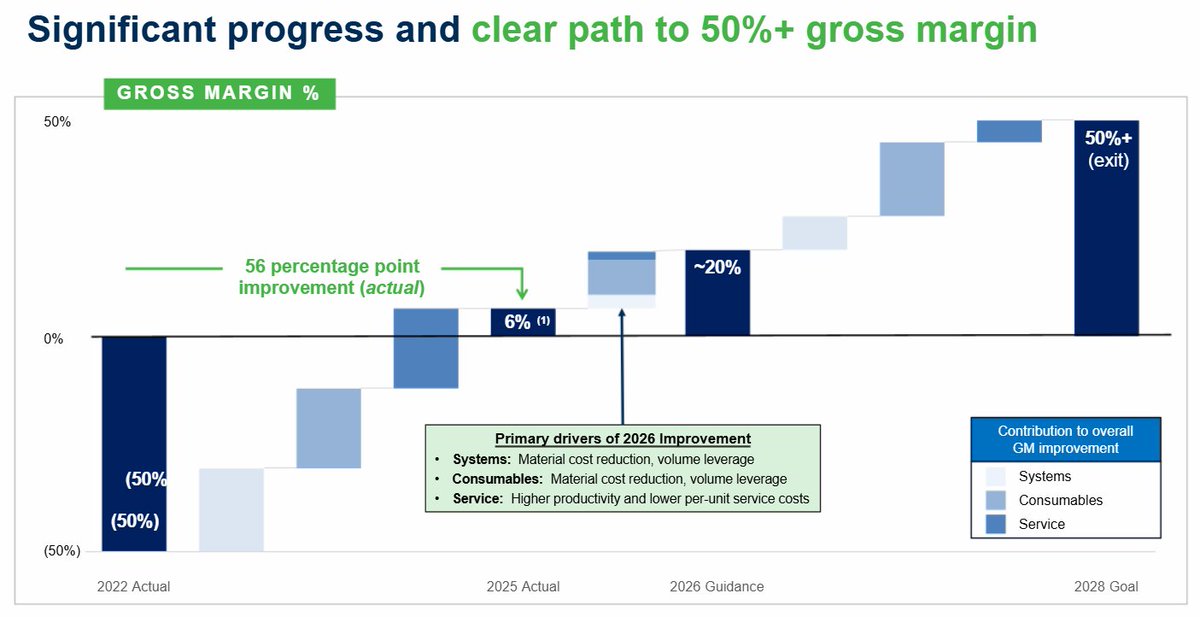

$RPID updated presentation shows first-time out-year guide of 50%+ GM on 2028 exit and 20%+ top-line CAGR implying $75-80MM 2030 revenues. At 30% OM we get to $22-24MM EBITDA. Today's EV is <$90MM. Pretty ridiculous - and clearly M&A candidate too.

English

JoHnL retweetledi

@everyonehatesp1 Revenues likely to fall in 27 becuz Part B price reset in 26 unless they can break into hospitals. Yes they have lots of cash but that would probably go into acquisition to grow rather than shareholders, so the bet at this price would be management make good deal, thought?

English

@hippo_finance At this point LNG seems like the side show, volume for gold contract could go a lot higher not to mention potential of silver and copper contracts, these prob the value drivers long term

English

$CCDS.V seems to have bottomed but could be wrong. Write up on my thoughts on valuation open.substack.com/pub/diminishin…

English

Some thoughts $BAER, open for some thoughts from other investors, great info from @BDeveran and @spacanpanman on bull case

@diminishingrreturns/note/p-191468659?utm_source=notes-share-action&r=392em0" target="_blank" rel="nofollow noopener">substack.com/@diminishingrr…

English

@Lotterystonks any thoughts on the dilution in 2Q and will likely continue given current cash position

English

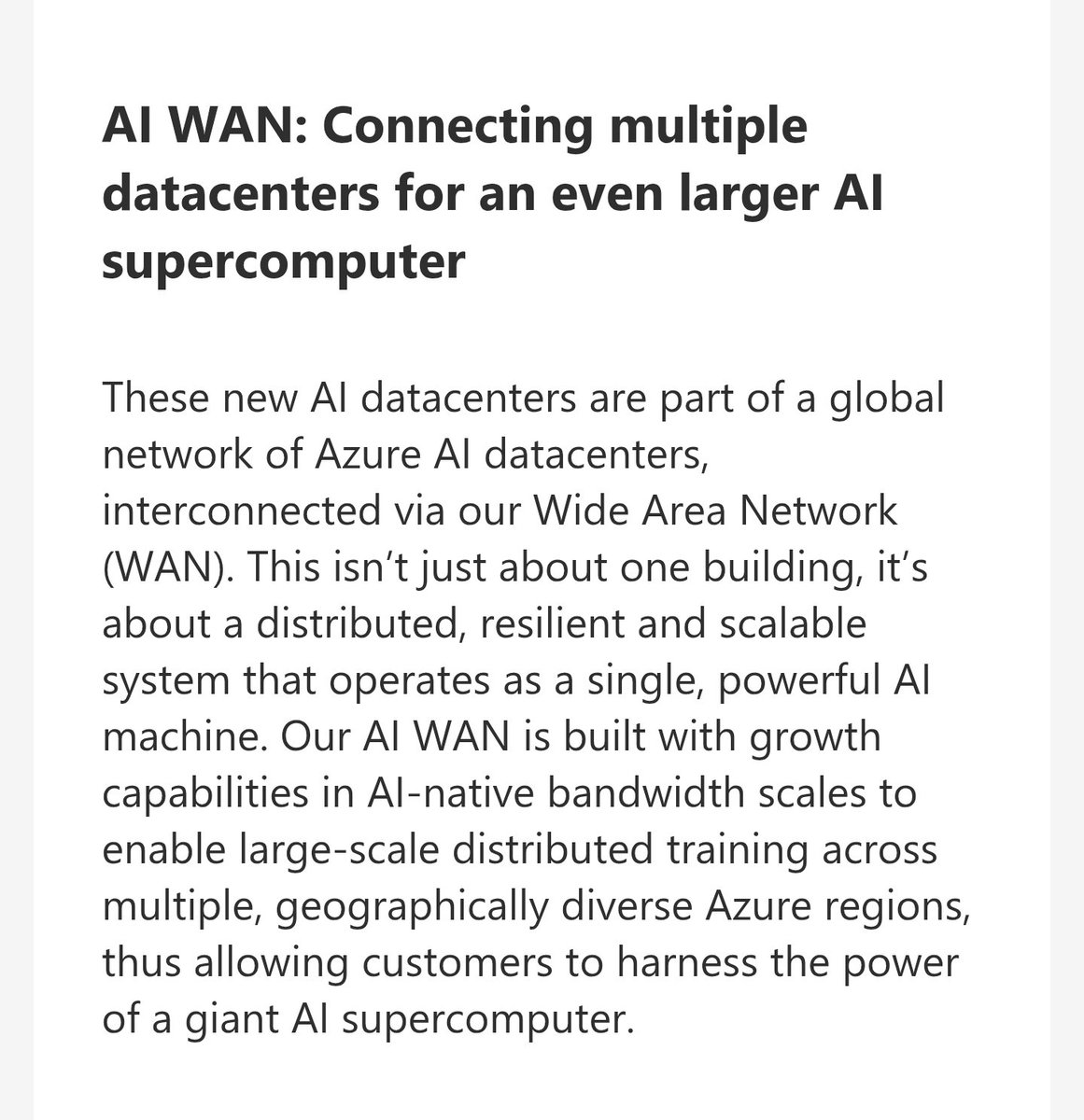

$NUAI $MSFT if you followed my DD on this.. Things are getting crazier..

Msft planning to connect their datacenters to form a huge AI wan.🤯

"-This is a fundamental shift in how we think about AI supercomputers. Instead of being limited by the walls of a single facility, we’re building a distributed system where compute, storage and networking resources are seamlessly pooled and orchestrated across datacenter regions. This means greater resiliency, scalability and flexibility for customers."

Imo, from Odessa and NUAIs powered land will be the first rollout of this AI wan running through MSFT core hub cities.

They will do it with their Hollow Core Fiber that just now made a big breakthrough in performance.

You ain't bullish enough.

blogs.microsoft.com/blog/2025/09/1…

English

@Michigan_Value Do you think OPUVIZ alone could reach $300M, seems like a big market for them to capture from EYLEA

English

Next, let's consider the 3 new drugs acquired for almost nothing up front. $HROW's M&A terms: ~10% royalties and zilch up front. Small drug companies take the deal bc HROW can sell those drugs way better than the original owners can. Those 3 drugs, likely another $300M, include

English

$HROW $500 2030 price target long post. We get something like $500, give or take, if they get to $2B revenue. The portfolio before recent M&A is likely to get pretty close:

Vevye $1B

Iheezo $300M

Triesence $200M

Immy and small legacy drugs $150M

= $1.65B

English