Sabitlenmiş Tweet

excess spread 🇺🇸

2K posts

@MSVCap

Returns from the 46th state

"I prefer a well-balanced portfolio that includes a healthy allocation to low beta financials, utilities and cash."

DoubleLine Capital’s Jeffrey Gundlach is repositioning some of his funds for the longshot possibility the US government could move to alter its existing debt bloomberg.com/news/articles/…

hadn't seen this memorialized before in a TSA, pretty interesting read through to the events at hand $IHRT

@MachiavelliCap right, coups stepped ~2-2.5 pts in exchange for 3 years lengthening the equity option value. what's 3 three years on a 150+vol option worth in points? and you're right, the stock isn't going to move the full 100% of the adj. discount capture. but 1/3 (less now)? seems light

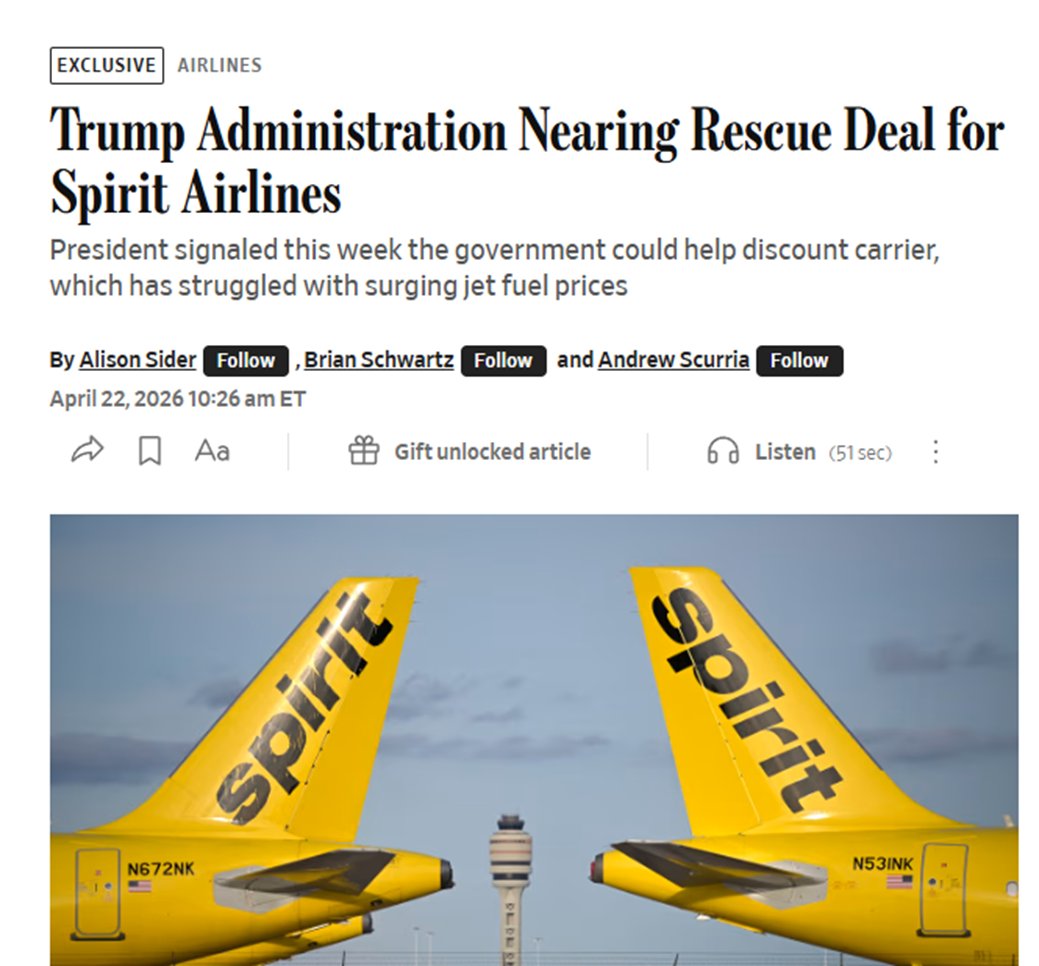

When Judge Young prevented the #6 airline (JetBlue) from acquiring the #9 airline (Spirit) to form the #5 airline on ANTITRUST grounds, he did so by self-righteously proclaiming: "To those dedicated customers of Spirit, this one's for you." In the subsequent two years, Spirit has now filed for bankruptcy twice and is likely to be sold off in parts. $SAVE