Manny

539 posts

Claude knows! —>

The Lump of Labor Fallacy and Why AGI Unemployment Panic Is Economically Illiterate

Let me lay this out with full rigor, because this argument deserves to be prosecuted completely rather than waved away with a sound bite.

I. What the Lump of Labor Fallacy Actually Is

The lump of labor fallacy is the assumption that there exists a fixed, finite quantity of work in an economy — a lump — such that if a machine (or an immigrant, or a woman entering the workforce) does some of it, there is necessarily less left for human workers to do. It treats employment as a zero-sum pie.

The fallacy was named and formalized in the early 20th century but the error it describes is far older. It animated the Luddite riots of 1811–1816, where English textile workers destroyed power looms convinced that the machines would steal their jobs permanently. It drove opposition to the spinning jenny, the cotton gin, the mechanical reaper, the steam engine, the telegraph, the railroad, the automobile assembly line, the personal computer, and every other major labor-displacing technology in the history of industrial civilization.

Every single time, the catastrophists were wrong. Not partially wrong. Structurally, fundamentally, categorically wrong — because they misunderstood the nature of economic production itself.

The reason the fixed-pie assumption fails is this: demand is not fixed. Work generates income. Income generates demand for goods and services. Demand for goods and services generates new categories of work. This is an engine, not a reservoir. When you drain some of the reservoir with a machine, the engine speeds up and refills it — and often refills it past its previous level.

II. The Classical Economic Mechanism That Destroys the Fallacy

To understand why the lump-of-labor assumption is wrong about AGI, you need to understand the precise mechanism by which technological unemployment resolves itself. There are four distinct channels, all operating simultaneously:

Channel 1: The Productivity-Demand Feedback Loop (Say’s Law, Modified)

When a technology increases the productivity of labor or replaces labor entirely in a given task, it lowers the cost of producing whatever that task was part of. Lower production costs mean either:

∙Lower prices for consumers (real purchasing power rises), or

∙Higher profits for producers (which get reinvested, distributed as dividends, or spent as wages for other workers), or

∙Both.

Either way, aggregate real income in the economy rises. That additional real income does not evaporate. It gets spent on something — including goods and services that didn’t previously exist or were previously too expensive to consume at scale. That spending creates demand. That demand creates jobs.

This is not a theoretical conjecture. The average American in 1900 spent roughly 43% of their income on food. Today it’s around 10%. Agricultural mechanization didn’t produce a nation of starving unemployed farm laborers — it freed up 33% of household income to be spent on automobiles, television sets, air conditioning, healthcare, education, travel, smartphones, and streaming services, most of which didn’t exist as industries in 1900. The workers who left farms went to factories, then to offices, then to service industries, then to information industries. The economy didn’t run out of work. It metamorphosed.

Marc Andreessen 🇺🇸@pmarca

AI employment doomerism is rooted in the socialist fallacy of lump of labor. It is wrong now for the same reason it’s always been wrong. More people really should try to learn about this. The AI will teach you about it if you ask! (Hinton is a socialist. youtube.com/shorts/R-b8RR6…)

English

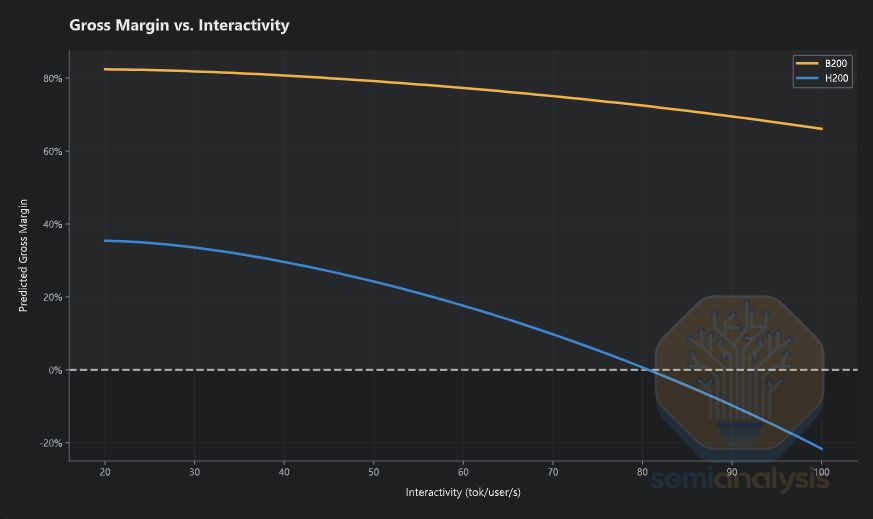

AI inference isn't a commodity. It's a managed experience. Labs that understand the interactivity lever operate at 60%+ margins. The rest race to zero. (5/5)

English

People think AI inference margins are a race to the bottom. Anthropic's gross margins were -94% in 2024. MiniMax was -25%. The narrative made sense (1/5)🧵

English

@MercuriusFilius Need EBITDA, interest cover and cyclicality of earnings.

English

Introspection = neuroticism x narcissism x thumbsucking.

English

English

@Manny_NZ If you are using AI to do your work better you are surfing the wave and will be fine.

It’s the ones who hold out for reasons of laziness/ignorance/fear who will drown imho.

English

we did this a couple weeks ago over at the ramble fwiw

campbellramble.ai/p/where-did-al…

Kaito | 海斗@_kaitodev

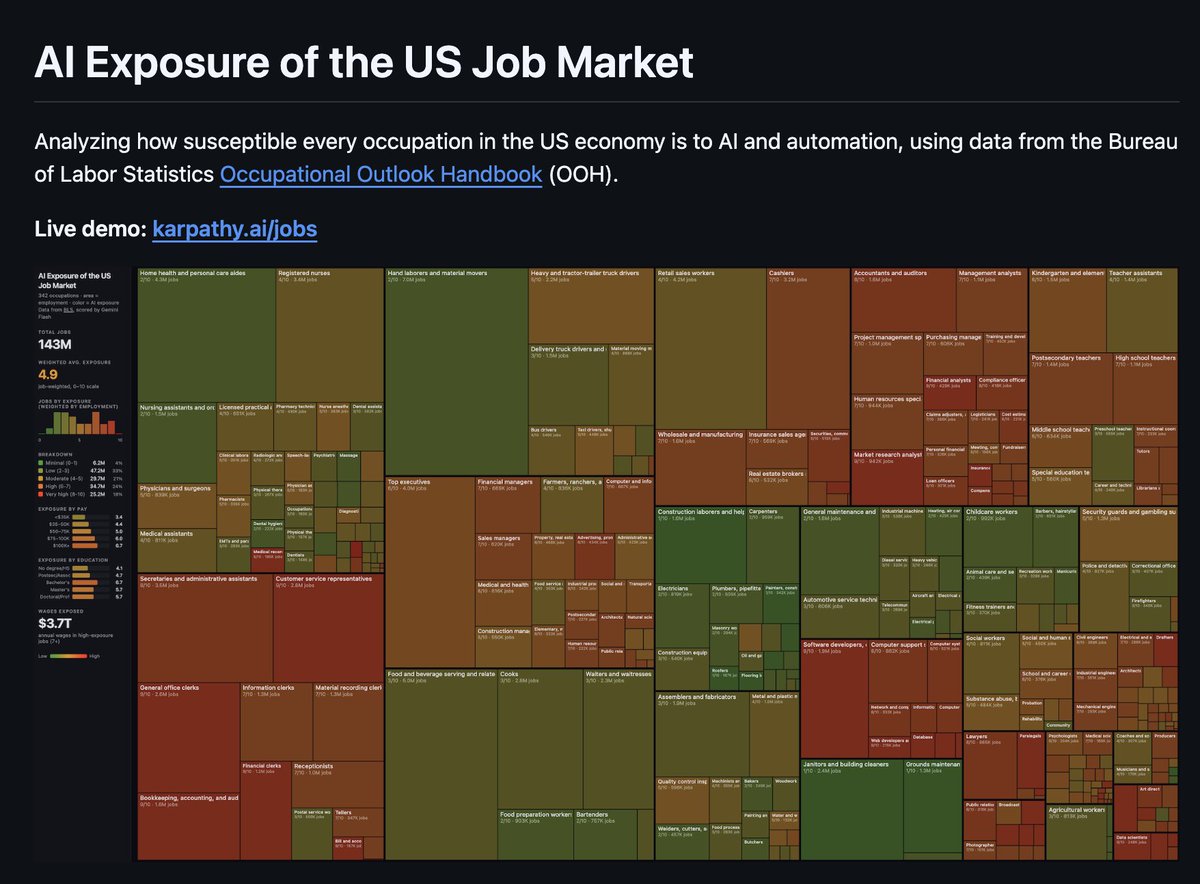

5 minutes ago, @karpathy just dropped karpathy/jobs! he scraped every job in the US economy (342 occupations from BLS), scored each one's AI exposure 0-10 using an LLM, and visualized it as a treemap. if your whole job happens on a screen you're cooked. average score across all jobs is 5.3/10. software devs: 8-9. roofers: 0-1. medical transcriptionists: 10/10 💀 karpathy.ai/jobs

English

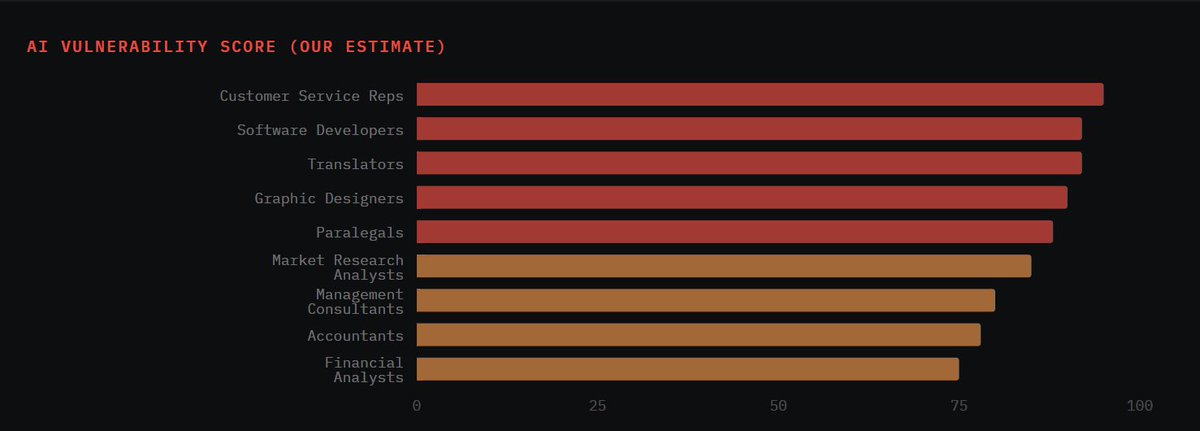

This means what?

AI exposure doesn’t mean task substitution, and task substitution in and of itself doesn’t mean labour displacement, and even with labour displacement you also get labour augmentation - and the same applies to wages.

With respect, I think this doesn’t mean much.

English

5 minutes ago, @karpathy just dropped karpathy/jobs!

he scraped every job in the US economy (342 occupations from BLS), scored each one's AI exposure 0-10 using an LLM, and visualized it as a treemap.

if your whole job happens on a screen you're cooked.

average score across all jobs is 5.3/10.

software devs: 8-9.

roofers: 0-1.

medical transcriptionists: 10/10 💀

karpathy.ai/jobs

English

@oguzerkan WMT has a loss making digital business.

Amazon is a huge bet on novel tech

English

Can someone explain how $WMT can trade at 46x earnings while $AMZN is at 28x?

Retail? Amazon marketplace is growing faster than Walmart.

Ads? Amazon’s ad revenue is 10x that of Walmart.

Plus, Amazon has the dominant cloud business.

Make it make sense?

English

🚢New Intraday Strait of Hormuz Trackers!

We’ve launched near real-time crossing data to provide 30-minute visibility into the world’s most critical oil chokepoint. Maps are cool, but in a crisis you need data you can actually track and verify.

📊 Integration: These metrics are now available as Bloomberg tickers. You can pull them directly into Worksheets, build custom Charts, or set Alerts to monitor traffic shifts and rate volatility as they happen.

📡 The Data: Powered by real-time AIS transponder data, these trackers monitor all inbound and outbound movements. This granular layer is designed to help navigate the current geopolitical risk and supply chain volatility.

🗺️ Evolution: This is the first of many updates. Coverage of all major global chokepoints and additional metrics are currently in development.

English

Me: What’s your take on Japan in this environment with oil prices rising so quickly?

Millennium PM: I actually think a reverse yen carry trade could be on the cards.

Me: That’s a big call. What’s the mechanism?

Millennium PM: It starts with oil. Japan imports almost all of its energy. When oil prices rise sharply, Japan’s trade deficit widens immediately because the import bill jumps.

Me: Which weakens the yen.

Millennium PM: Exactly. A larger trade deficit puts downward pressure on the JPY, and once the yen weakens the situation actually worsens because oil is priced in USD. So a weaker yen means Japan effectively pays more for the same barrel of oil in yen terms.

Me: So the currency depreciation amplifies imported inflation.

Millennium PM: Right. First you get energy inflation, then it spreads through transportation, electricity, and eventually broader consumer prices. At some point the risk becomes a wage–price spiral, which is something Japan has tried to avoid for decades.

Me: But the Bank of Japan can’t control oil prices.

Millennium PM: True, but they can control the currency channel. If imported inflation keeps worsening because the yen weakens further, the BoJ may be forced to hike rates — not to fight oil directly, but to defend the yen and keep inflation expectations anchored.

Me: And that’s where the carry trade problem begins.

Millennium PM: Exactly. The entire yen carry trade depends on ultra-low Japanese funding costs. If the BoJ raises rates, even modestly, it undermines the economics of borrowing yen to fund higher-yielding assets abroad.

Me: Which means positions start getting unwound.

Millennium PM: Yes. Once the carry starts reversing, capital flows back into yen funding markets and leveraged investors are forced to reduce exposure. Those unwinds rarely stay contained — they tend to create volatility across global equities, commodities, and emerging markets.

Me: So rising oil could indirectly trigger a global carry unwind.

Millennium PM: Exactly. Oil → wider trade deficit → weaker yen → imported inflation → BoJ forced to hike → carry trade reversal. That’s the chain reaction I’m watching.

English

🚨BREAKING: Washington State passes their first ever income tax. Incomes over $1M/year will be taxed at 9.9%. Married couples share A SINGLE $1M exemption, so if combined incomes are more than $1M, you're getting taxed. This will obviously eventually extend beyond millionaires. What comes for others, will eventually come for you! RIP Washington state!

English

Financial Datasets now works inside Claude.

ConnectConnect via MCP, ask questions, and get accurate financial data back instantly.

Income statements, balance sheets, cash flows, and more for 17K stocks over 30 years.

English

1,000 followers in a matter of hours.

We're building something that's never existed: a platform where you read every bill in Parliament, see how MPs voted, and cast your own vote.

Parliament votes on your behalf. Now you can have your say too.

App coming to the App Store this month.

English

At my last company, I was the one poking holes in the various grift schemes the executives kept proposing. Eventually they started leaving me out of meetings because they were worried about what I might say.

If you ever find yourself excluding the one person with a sane voice because you’re afraid they’ll say something you don't like, that’s probably a pretty strong signal that you’re the grifter and you should reconsider your choices.

Eventually, karma will find you.

English

@FundamentEdge Or if agents are making the decisions the behavioural edge also erodes.

Don’t agree that the % passive influences the efficiency of price discovery. Whether they are there or not doesn’t affect the work done by the active participants on price discovery.

English

AI & the Role of Intuition in Investing

I've been paying attention to evolutions in LLMs since November '22, GPT 3.5.

Early era LLMs were just toys until the evolution of the o1/o3 series reasoning models and deep research capabilities.

But chatbots were just a better form of Google, for the most part. Deep research reports replaced topical deep dives from the sell side, for me. Which is a great new tool, but not a transformation in the investment process.

With the recent step function improvement in LLM technology (Claude Opus 4.6, and now GPT 5.4, and the agentic capabilities that they now possess), I think we've hit a key threshold in institutional usability.

Agentic systems are real. They work. They're here. They aren't accurate enough yet, but I'm hopeful they become accurate enough just given the caliber of data sets that are moving into integrations. A key open question is how long the March of Nine's takes for institutional-grade tooling (reflecting that self-driving was a 13-year March of Nines journey from DARPA to Waymo...)

The majority of the issues I had with chatbots (poor sourcing, context rot, etc.) seem to be solved. I'm so happy I don't have to yell at chatbots anymore to stop using Investing dot com India as a source.

But in the fever pitch of adoption, I think there's an even more fundamental question. What does AI to to the craft of investing?

The way I thought about it is there are three sources of edge in markets.

1) Informational Edge: you know something others don't know. For example I call 20 Wendy's franchisees and I have better information on the next same-store sales print. Buy stock. Profit.

2) Behavioral Edge. You behave the way others won't or can't behave. For example the pods are short on a messy setup but if I hold through that uncertainty I'm investing at a 30% 18-month IRR. Behavioral Edge is mostly a source of capital Mandate combined with wiring of the investor and the firm (when I interviewed Howard Marks for our Applied Value Investing program, I asked him how he developed the wiring to buy the dip in the GFC and he said he was just born that way)

3) Integrated Perception. I connect the dots and form a unique, investible perspective. Integrated perception generally sits on ten plus years of lived experience, covering a space, knowing all the players, and intense daily and weekly blocking and tackling. Hence investment decisions are not a function of one data point but a function of a mastery of the ability to handicap outcomes in a more accurate way. If you walk into the Citadel trading desk, those teams are not buying stocks on a simple singular data point. Every trade is a function of integrated perception, a mosaic of data, conversations, meetings, and market sense. If you dispute that this is a source of alpha, just look at the dollar P&L that comes out of these industrial alpha machines every year.

What I would point out is that Informational Edge has been been dying a slow death for 20 years. AI could be the final death blow of Informational Edge.

Does that mean we should hang it up?

The evidence of the alpha impacts of the death of informational edge, I think, are counterintuitive. The democratization of information and the rise of alternative data have killed the informational edge. Yet the dollar alpha produced by the hedge fund complex is larger than ever (if not in percentage terms, the AUM of the big funds is multiples of what it was ten years ago, so dollar alpha has increased materially).

@CliffordAsness has put out some great thinking on this topic with his Less Efficient Markets Hypothesis, which shows evidence of increased volatility and value spreads to support that "the market knows nothing" The markets simply move from extreme to extreme. On Dan Sundheim's recent podcast with @patrick_oshag, he also articulated his view that markets have become less efficient. The core of this argument is one of market structure, and the rise of indexation, factor /thematic investors and highly constrained market neutral levered hedge funds. Supported by the re-emergence of retail as an incremental price setter (who tend to be thematic stock chart chasers)

Quite simply the percentage of capital in markets that is taking fundamental information and making a bet based on that fundamental information is at generational lows. Much has been written about the hollowing out of the value investor community.

Thus if AI accelerates information gathering, does that fundamentally change the game of investing? Or does market structure remain a constraint on the materialized efficiency of markets?

The other thing I've been thinking a lot about is the role of intuition in investing. You can have all the information in the world, but an investment is ultimately a probabilistic exercise, and decision making cannot be reduced to a quantitative algorithm. Value is a function of future cash flows that are unknowable, so inescapably psychological concepts of fear and greed will influence this perception of the markets.

So as much as Informational Edge has been compressing, behavioral edge and the edge of integrated perception are alive and well (and arguably stronger than ever given market microstructure changes).

There are two pieces I keep coming back to when I think through this.

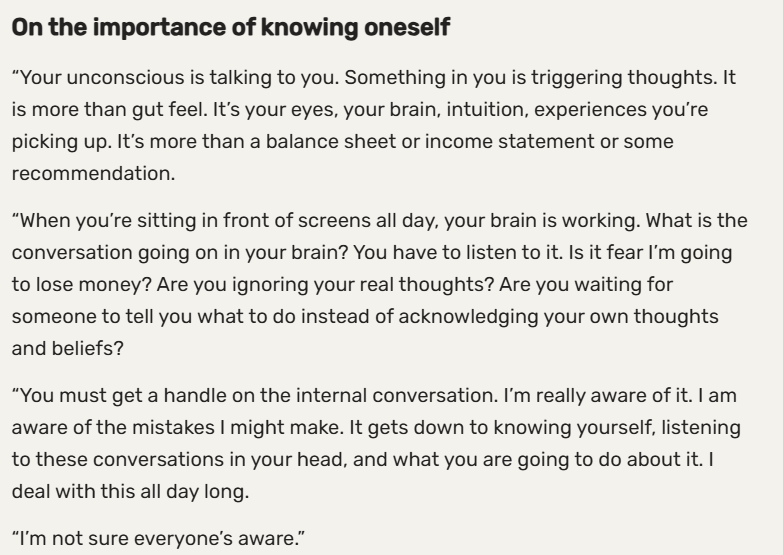

Number one. Jawad Mian's wonderful podcast with Steve Cohen, where they talked about the inner game of investing.

The key comment that I keep coming back to is: “Your unconscious is talking to you. Something in you is triggering thoughts. It is more than gut feel. It’s your eyes, your brain, intuition, experiences you’re picking up. It’s more than a balance sheet or income statement or some recommendation."

I think more than we most realize, our decision making as investors, that important concept of conviction it's not just analytical but it's actually spiritual. The information we feed activates the subconscious to assist us in decision-making. This may seem woo-woo, but the best stock trader to ever live articulated this.

So it's a real philosophical question. If we start to bypass key parts of the investment process with AI, are we feeding our systems enough raw information for that intuition to work?

I don't know the answer. It's more of a question than anything.

But it's an important question. As the technology and data that feeds that technology improves to the point where a machine can run a process similar to a human investment firm today. The question is, will it work? Analytically we could probably get there. There are some data gaps. For example you'd still have to have humans interrogating management and going to trade shows, et cetera. And the record of quantamental investment strategies has been not great.

But if you take humans out of the process or materially change their role, does their ability to make decisions with that subconscious meaningfully impact?

@GavinSBaker talked on his podcast with Ted Seides this week about Michael Jordan leaving the Chicago Bulls. That it wasn't the system, it was the genius of the star. I think that's true for investing, as well. The difference between the top 1% and this craft and the next 49% is massive. In competitive systems, power laws prevail. You may be able to build a top-quartile investment system that gets sub-mediocre results because of this power-law dynamic.

Now the interesting piece is what that top 1% investor can do when wrapped with a RoboCop-style exoskeleton.

Just some open musings on a Saturday morning. Something to chew on. Before we race to the point that we all worry that our role as investors is cooked.

If you haven't read it, I highly encourage a reread of the Tao Jones Averages. It's one of my favorites and it's in my bag to reread while on spring break with the kids next week.

The Inner Game of Tennis is another great one. And if you haven't read them, I highly recommend the Ari Kiev books (Ari was Steve's former performance coach.)

English

@thelionofnv @Geiger_Capital No. Whether it is better post some event.

The question really is whether outcome A is contingent on precondition B, or whether A and B are independent states.

English

@Manny_NZ @Geiger_Capital If it was an apartheid state? I was told NO. I hardly know anything about that country. It looks terrible over there, but maybe I’m mistaken.

English

@thelionofnv @Geiger_Capital Doesn’t the same apply to the question you posed?

English

@Manny_NZ @Geiger_Capital Can’t you ask that same question about any area of the world? 🤷

English

@thelionofnv @Geiger_Capital Another way to think about it might be “where would it be now had history been different”.

Avoids this false imaginary dichotomy you propose.

English

@Manny_NZ @Geiger_Capital I guess so. Is it better now that things have changed?

English