MontviewX

62 posts

What is historically super cheap here (cheaper now than last 10 years)on a NTM basis? $CSU / $TOI $MELI $NVDA What else?

I'm not going to dis AOC's B.A., but do you really think earning a bachelor's degree is a more impressive achievement than taking a small family business w/ 6 employees and turning it into a company with over 300 employees and $20 million in annual sales? If so, you're an idiot.

The Centers for Medicare and Medicaid Services posted new details today about its CBD pilot program, which launches April 1. The details confirm recent reports that eligible products can contain up to 3 milligrams of THC per serving. themarijuanaherald.com/2026/03/center…

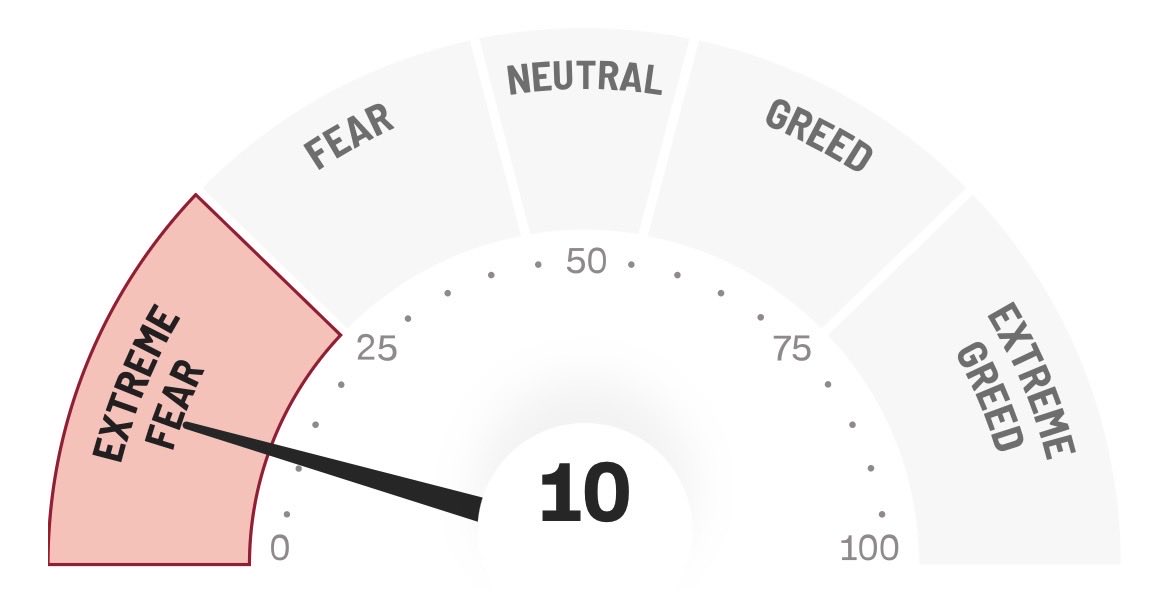

2) To see how ridiculous this lead is, take a look at the monthly graph of Pending Sales. They rose from an index of 70.8 in January (which was the worst January reading ever) to 72.1 in February. No sane person would interpret this result as an "improvement" in macro housing market conditions. Especially with the backdrop of mortgage rates falling below 6% in February.