Alec Euriq

1.1K posts

OpenAI’s $100MM advertising run rate is almost entirely a function of “novelty demand” since they launched a primitive product with little optimization capacity. Relevant questions: 1) How much better does the platform get?, 2) Where does demand settle when they can accommodate SMBs?

Alec Euriq@RationalOptimi5

@eric_seufert @lfg_cap Is it a function of companies just trying this out (ie. pilots), or is the product actually working?

English

@eric_seufert @lfg_cap Is it a function of companies just trying this out (ie. pilots), or is the product actually working?

English

@RationalOptimi5 @lfg_cap Real. OpenAI comms team emailed this stat to me a few hours ago.

English

“OpenAI has surpassed $100 million in annualized revenue from its ChatGPT ads business, six weeks after the pilot was announced, according to a spokesperson”

We’re all old enough to remember when a $100M product took years to scale.

Lots of Monday Morning Quarterbacking on here about @OpenAI & @sama lately. But the team is moving fast and fixing its mistakes.

h/t @theinformation

theinformation.com/briefings/excl…

English

@patrick_oshag Correlation-causation will be hard to discern for some time

English

Nuts

Eric Glyman@eglyman

Since 2023, the top quartile of AI spenders on @tryramp have more than doubled their revenue. Bottom quartile? Flat A roofing company in Texas. A window installer in Utah. A construction firm in Florida that grew 65% The gap is accelerating and most companies don't feel it yet

English

@pekwat Sometimes they will, but it is not common, as it breaks the illusion that this is an asset the GP wants to ‘hold on for longer’. A failed M&A process is a yellow flag, so if you hold a dog and think M&A will fail, you go directly to a CV

English

@pekwat In many instances, LPs are getting a price > M&A. Additionally, and perhaps even more importantly, they are getting liquidity in a situation where an M&A event was unlikely.

So itms a trade off - not obvious to me which side is getting the better deal, time will tell.

English

@MontviewX @breadcrumbsre Most PE assets are deeply underwater at those levels. Don’t see it happening any time soon for the higher quality companies, even if this is where they should trade at a fundamental level

English

@breadcrumbsre Maybe it’s more like ~13% vs ~6% controlling for multiple expansion/contraction? You gotta believe target multiples have come way down to get to mid teens though

English

@buccocapital @travisk There’s a lot of truth to what you’re saying, but the issue with SMB is the amount of death/birth in the space, so if a better product comes along, INTU might start shedding a lot of market share on new adds to the disruptors, which would break their unit economics.

English

People are destroying SMB B2B software but there’s a meaningful chance HUBS/INTU are AI winners:

I was listening to @travisk who recently said:

“LTV:CAC with a sales machine, especially if you go [after] small businesses, is life on hard mode. Anybody who’s crushed it on SMB, those guys are special individuals who've made that happen. Because life in the SMB B2B world is no joke."

Hard mode. Sounds moaty to me. Some thoughts on how the market could be wrong re: HUBS/INTU

1. SMB is brutally, brutally hard to make the math work, so counter intuitively there’s less competition. And in some sense the survivors are anti-fragile. They keep consolidating share during downturns

2. They have aggregated the customers and have the scale economics

3. AI will encourage full-platform adoption as agents benefit from max surface area and clean data

4. SMB are less tech savvy. Will just want tech that works.

5. Can either roll up space or launch incremental features cheaply w AI

6. Low cost/freemium competition is not new. Vibe coding doesn’t change that.

7. AI will cause an explosion in small business creation

English

@pekwat I think there are more than one example of 20-25x forward on optimistic margin progressions. That would translate to >25x ltm even on normalized margins

English

@pekwat I was kind of buying the thesis until they acquired an asset I was a lot more familiar with. Untouchable for me after that. A true Gell Mann moment

English

@pekwat They’ve paid well north of that for some targets. 25-30x ebitda on normalized margins for unprofitable companies growing mid teens. Crazy stuff

English

@kofinas Bret has shown us who he is. Not sure it is worth spreading his takes tbh. This is not an intellectually honest communicator any more.

English

Is the assumption here that Charlie Kirk's very existence posed such an existential threat to the national security state that he needed to be urgently killed?

It seems the bar for a state-led conspiracy to murder someone for his general opposition to war is being set very low.

Bret Weinstein@BretWeinstein

On June 18th, I had a text exchange with Charlie Kirk. He said he was spending two full days at the White House trying to persuade President Trump not to initiate a war with Iran. Given that Charlie was close with the President and that he represented a large constituency essential to Trump, and given that many proponents of the war with Iran saw a U.S. attack as urgently necessary to the survival of Israel, it is reasonable to wonder if his refusal to back down from his steadfast opposition somehow resulted in his murder. A good investigation could have settled the matter. What we got only increases the reason for concern. Asking this question may be unforgivable, but it is in no way unreasonable. Charlie was in a strong position to keep us from doing what we have now done, and the timing of his death removed him from the equation and likely changed the course of history--as Charlie himself worried it might.

English

@viggy_krishnan @pekwat @HatfieldCapital @rev_cap Only a breakdown of the system. Authoritarianism or something similar.

Hyper growth / productivity would be another avenue but a lot less likely.

English

@SouthernValue95 PC bubble is overblown.

Mostly self contained, vast majority of credits will be either money good or deliver ok recoveries. Overall losses should be <10% cumulative in the next 5 years, even in a downside case

English

And if you think strongly one of the above risks is overblown, let me know why?

English

What risk are you actually worried about being a real systemic risk leading to a multiyear blowup, starting now?

English

@ACapitalLP @DDInvesting @OctusCredit @hhawnk15 I guess you could, but its a decently capitalized market with clearing prices above where he is guiding.

English

My take: The best opportunity in the market is setting up a fund/vehicle to buy dislocated private credit loans from forced sellers.

My credentials: I run the leading information and data provider on the global credit markets (@OctusCredit). I was buying bank debt in the 60s in the fall of 2008 that eventually refi'd at par, including from the Lehman desk auction. I am very bullish on software and think the Citrini thesis is flawed. I reached out to them to debate me on our podcast.

Two quotes from Seth Klarman have guided my investing for over 20 years:

1) "My experience is that when people want to give something away at a ridiculous price because they have to, not because they want to, that’s a good time to buy."

2) "The best opportunities for value investors often arise when other investors are forced to sell, regardless of price."

Over the past couple of weeks, headlines have rolled in about redemptions coming from public and private credit funds:

""Morgan Stanley Limits Redemptions at $7.6B North Haven Fund After Withdrawal Requests Hit 11%" (March 12, 2026)"

"Cliffwater Limits Repurchases to 7% After Record 14% of Investors Seek Exit From $33B Flagship"

"Blue Owl Gates OBDC II as Hedge Funds Circle With 35% Discount Buyout Offers" (March 10, 2026)

Another headline: "Private Credit ETFs Plunge 18% in Two Weeks as 'Gating' Fears Spread to Publicly Traded Vehicles"

I believe these headlines will continue. Investors should get used to them. Or as George Soros' concept of reflexivity: our perceptions of reality don’t just reflect reality—they actively change it.

Or in steps...

1. The Bias

Investors believe private credit is a "magic" asset class: high yields with low volatility. They assume "semi-liquid" funds mean they can always get their cash back quarterly.

2. The Action

A $1.7 trillion wall of cash pours in. This massive liquidity makes the underlying borrowers (software companies) look healthier than they are, "validating" the initial bias.

3. The Pivot

AI threats / Citrini thesis emerge. A few "smart money" investors doubt the fund valuations and submit redemption requests to test the exit.

4. The Spiral

Funds hit their 5% withdrawal caps and "gate" the doors. This act of self-preservation signals "danger" to the rest of the herd, turning a small exit into a mass panic.

5. The New Reality

The perception of a "safe haven" has been reflexively destroyed. The asset is now a liquidity trap, creating the "forced sellers" that Seth Klarman waits for.

Soros once wrote: "Financial markets, far from accurately reflecting all the available knowledge, always provide a distorted view of reality. The degree of distortion may vary from time to time; sometimes it’s quite negligible, at other times it is quite pronounced."

If redemptions still continue and private credit is considered an asset to avoid, more investors will ask for their money back. And more funds will be forced to sell assets inside these funds.

The underlying businesses haven't changed. The huge cash equity checks beneath these loans haven't changed (Yes LTV has changed because multiples have compressed but cash is still there). The maturity profile hasn't changed. Revolvers are still available.

The one thing that has changed is the reflexivity of the new reality and people are rushing for the doors in an illiquid market = buying opportunity.

Here is some simple math:

If you buy a loan at 90, with a SOFR + 500 floating rate coupon that matures/refis at par in 3 years your return is ~13%.

If you buy a loan at 80, with a SOFR + 500 floating rate coupon that matures at par/refis in 3 years your return is ~18%.

If you buy a loan at 75, with a SOFR + 500 floating rate coupon that matures/refis at par in 3 years your return is ~21%.

I view these as the absolute LOW returns. I believe returns will be materially higher for 2 reasons:

1) The AI/Citrini thesis will be proven wrong shortly throughout this year as software companies report good numbers in Q1, Q2 and Q3

2) In the very off-chance you get to own the keys of these companies, buying a software company through a restructuring has the chance of MOICs over 2.0x taking into effect rights and equity discounts.

All told: As I said on our podcast, I think this could be a once in a generation opportunity to buy assets with MINIMUM mid teen returns, very little chance of capital loss with potential huge upsides.

I do not think an investor should BLINDLY buy everything being force sold by a private credit fund or BLINDLY buy every software company out there. But this is so overblown its creating an opportunity for the best credit investors in the world to set up vehicles to absolutely crush it. An alpha, not a beta trade.

The table is being set. The smart funds are already setting up to capitalize on this opportunity as it plays out over the rest of the year.

English

@jay_21_ Not only that, but there are very large players set up to do exactly this trade. And if press releases are to be believed, those trades are not being done in the 70s

English

Havent all of these things changed?

"Underlying businesses havent changed. Huge cash equity checks beneath these loans havent changed (Yes LTV has changed because multiples have compressed but cash is still there). Maturity profile hasn't changed. Revolvers are still available"

Kent Collier@DDInvesting

My take: The best opportunity in the market is setting up a fund/vehicle to buy dislocated private credit loans from forced sellers. My credentials: I run the leading information and data provider on the global credit markets (@OctusCredit). I was buying bank debt in the 60s in the fall of 2008 that eventually refi'd at par, including from the Lehman desk auction. I am very bullish on software and think the Citrini thesis is flawed. I reached out to them to debate me on our podcast. Two quotes from Seth Klarman have guided my investing for over 20 years: 1) "My experience is that when people want to give something away at a ridiculous price because they have to, not because they want to, that’s a good time to buy." 2) "The best opportunities for value investors often arise when other investors are forced to sell, regardless of price." Over the past couple of weeks, headlines have rolled in about redemptions coming from public and private credit funds: ""Morgan Stanley Limits Redemptions at $7.6B North Haven Fund After Withdrawal Requests Hit 11%" (March 12, 2026)" "Cliffwater Limits Repurchases to 7% After Record 14% of Investors Seek Exit From $33B Flagship" "Blue Owl Gates OBDC II as Hedge Funds Circle With 35% Discount Buyout Offers" (March 10, 2026) Another headline: "Private Credit ETFs Plunge 18% in Two Weeks as 'Gating' Fears Spread to Publicly Traded Vehicles" I believe these headlines will continue. Investors should get used to them. Or as George Soros' concept of reflexivity: our perceptions of reality don’t just reflect reality—they actively change it. Or in steps... 1. The Bias Investors believe private credit is a "magic" asset class: high yields with low volatility. They assume "semi-liquid" funds mean they can always get their cash back quarterly. 2. The Action A $1.7 trillion wall of cash pours in. This massive liquidity makes the underlying borrowers (software companies) look healthier than they are, "validating" the initial bias. 3. The Pivot AI threats / Citrini thesis emerge. A few "smart money" investors doubt the fund valuations and submit redemption requests to test the exit. 4. The Spiral Funds hit their 5% withdrawal caps and "gate" the doors. This act of self-preservation signals "danger" to the rest of the herd, turning a small exit into a mass panic. 5. The New Reality The perception of a "safe haven" has been reflexively destroyed. The asset is now a liquidity trap, creating the "forced sellers" that Seth Klarman waits for. Soros once wrote: "Financial markets, far from accurately reflecting all the available knowledge, always provide a distorted view of reality. The degree of distortion may vary from time to time; sometimes it’s quite negligible, at other times it is quite pronounced." If redemptions still continue and private credit is considered an asset to avoid, more investors will ask for their money back. And more funds will be forced to sell assets inside these funds. The underlying businesses haven't changed. The huge cash equity checks beneath these loans haven't changed (Yes LTV has changed because multiples have compressed but cash is still there). The maturity profile hasn't changed. Revolvers are still available. The one thing that has changed is the reflexivity of the new reality and people are rushing for the doors in an illiquid market = buying opportunity. Here is some simple math: If you buy a loan at 90, with a SOFR + 500 floating rate coupon that matures/refis at par in 3 years your return is ~13%. If you buy a loan at 80, with a SOFR + 500 floating rate coupon that matures at par/refis in 3 years your return is ~18%. If you buy a loan at 75, with a SOFR + 500 floating rate coupon that matures/refis at par in 3 years your return is ~21%. I view these as the absolute LOW returns. I believe returns will be materially higher for 2 reasons: 1) The AI/Citrini thesis will be proven wrong shortly throughout this year as software companies report good numbers in Q1, Q2 and Q3 2) In the very off-chance you get to own the keys of these companies, buying a software company through a restructuring has the chance of MOICs over 2.0x taking into effect rights and equity discounts. All told: As I said on our podcast, I think this could be a once in a generation opportunity to buy assets with MINIMUM mid teen returns, very little chance of capital loss with potential huge upsides. I do not think an investor should BLINDLY buy everything being force sold by a private credit fund or BLINDLY buy every software company out there. But this is so overblown its creating an opportunity for the best credit investors in the world to set up vehicles to absolutely crush it. An alpha, not a beta trade. The table is being set. The smart funds are already setting up to capitalize on this opportunity as it plays out over the rest of the year.

English

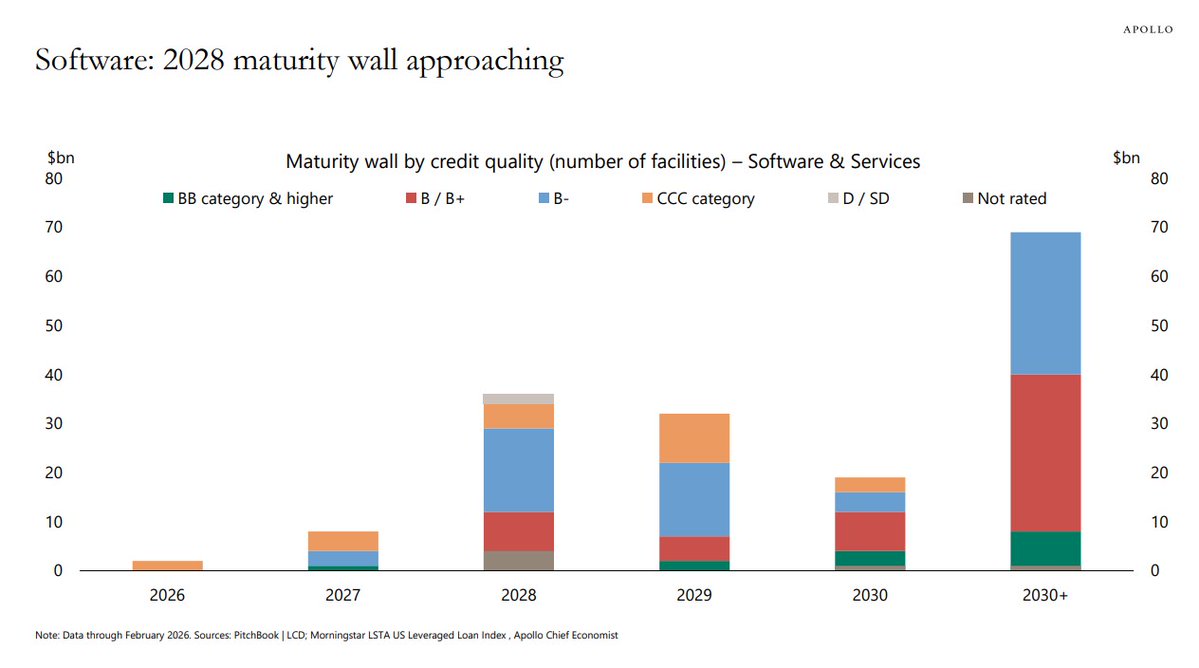

@TheStalwart Maturity wall is the gift that keeps on giving when it comes to doomerism

English

A lot of software debt is going to have to be rolled over in 2028. Via Torsten Slok

English

@BucknSF Direct vc secondaries already a thing. Multiple VC continuation funds have gotten done

English

VC continuation funds going to be all the rage

Richard Christopher Whalen@rcwhalen

"Continuation funds are a rapidly growing, key exit strategy for private equity (PE), with an estimated 20% of all PE exits in 2025 expected to be executed through these vehicles, up from 14% in 2024. Nearly 75% of the largest global PE firms have used at least one continuation transaction." @CFAinstitute

English

@pekwat It’s one of the dumbest things people continue to tout. 70s inflation was temporary as well if you widen your time horizon wide enough

English