Sabitlenmiş Tweet

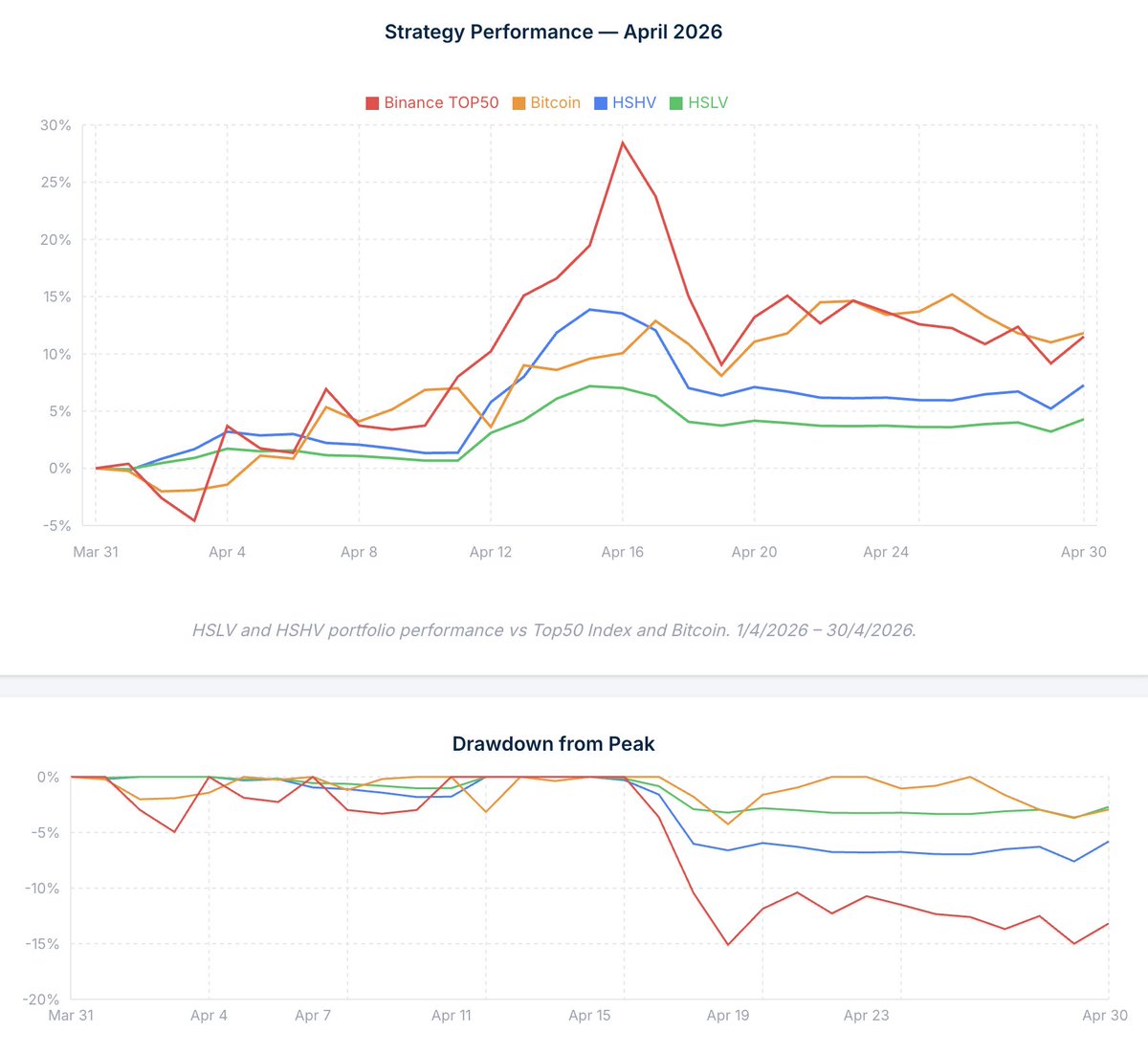

1. April Performance:

April closed positive.

HSHV portfolio delivered +7.3% with a -7.6% max drawdown.

HSLV portfolio returned 4.3% with a 3.7% max drawdown.

English

Pavel | Robuxio

8.5K posts

@PKycek

Daily insights on institutional algorithmic trading | CEO @robuxio_com

If I only has 10 minutes a day to trade-I would choose the last 10 minutes of RTH in indices........... All day-everyday.