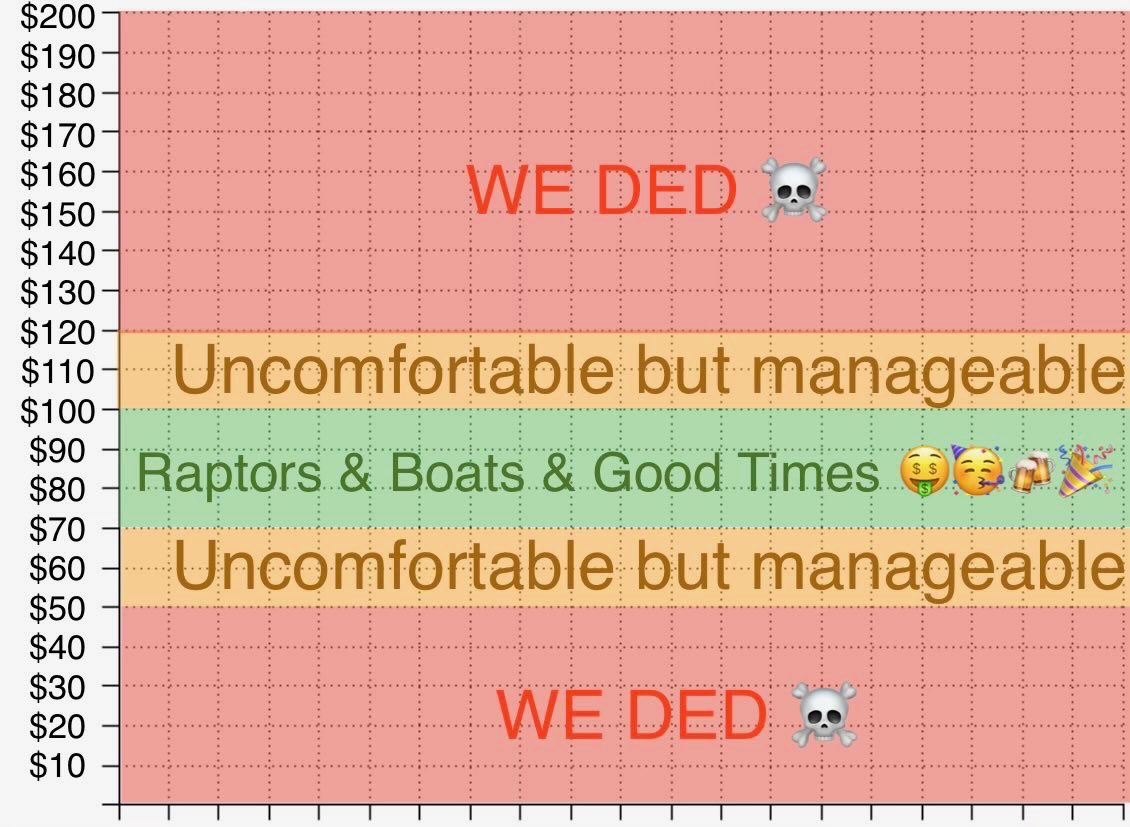

@kpb_rolling @tomkeene Great chart. Folks in The Patch are watching WTI closely

English

Paul Sweeney

2.1K posts

@ptsweeney

Co-host, Bloomberg Surveillance and Bloomberg Markets on Bloomberg Radio. Retweets are not endorsements and opinions are my own.

With apologies, a long tweet, about the likely macroeconomic outcomes of Liberation Day. Tariffs can be imposed for understandable if not necessarily good reasons: Protect a sector, right or wrong. Extract rents from foreign producers if there are rents to be extracted. Sure, if there is retaliation, everybody will be worse off, but it maybe worth taking the risk. Across the board tariffs, which sounds like what we are going to get, are however the worse possible tariffs. They are bad for the country that imposes them, even without retaliation. Standard scenario: The initial effect of higher tariffs may look good: Lower imports. Higher demand for domestic goods. Smaller trade deficit. But, with the smaller deficits, and the higher interest rates needed to keep demand under control, appreciation of the dollar (say), less competitive exports. Until trade deficit is back to square one. So: Useless? Worse. Costly reallocation from exports to import competing sectors. Misallocation. And for the revenues from tariffs: They are there, but in the end, they are paid mostly by US consumers. A relevant twist, which changes the standard scenario: The enormous uncertainty about Trumps’s tariff policy: Are the tariffs transactional or permanent? Will they remain/increase/decrease? In that environment, if I am a firm, what do I do? Build a plant in Mexico or in the US, in Vietnam or in China, etc. I do not know, and so I wait. We all wait. Investment comes down, aggregate demand falls, and the effect is a recession. Now the trade balance improves, for two reasons. The direct effect of tariffs, and lower activity means lower imports. As the Fed tries to maintain activity, lower interest rates and a lower dollar mean more exports. Looks great. Claim of success on the trade front (if you can make people forget the recession) But only for a while. Over time, as the economy recovers, you go back to the first scenario. The depreciation eventually turns into an appreciation, activity recovers, the trade deficit returns to square one Overall result: a recession, no gain. A general mess. We shall see how it all turns out.

Egg update 🥚 $8.64 for 2 dozen #costco 🛒 @tomkeene @ptsweeney

A breakthrough in Chinese Artificial Intelligence has US Stocks falling hard this morning. Get more information and analysis on DeepSeek in today's edition of Bloomberg Surveillance. Watch LIVE on YouTube with @tomkeene @ptsweeney @LisaMateoTV youtube.com/live/f39oHo6vF… via @YouTube

UConn Women’s Basketball Sets New Ticketing Benchmark sportico.com/leagues/colleg…