SimplicitasOpes

708 posts

SimplicitasOpes

@SimplicitasOpes

Investing in stocks, people & the community. Looking for undiscovered diamonds.

Tampa, FL (VT / NYC) Katılım Şubat 2022

274 Takip Edilen374 Takipçiler

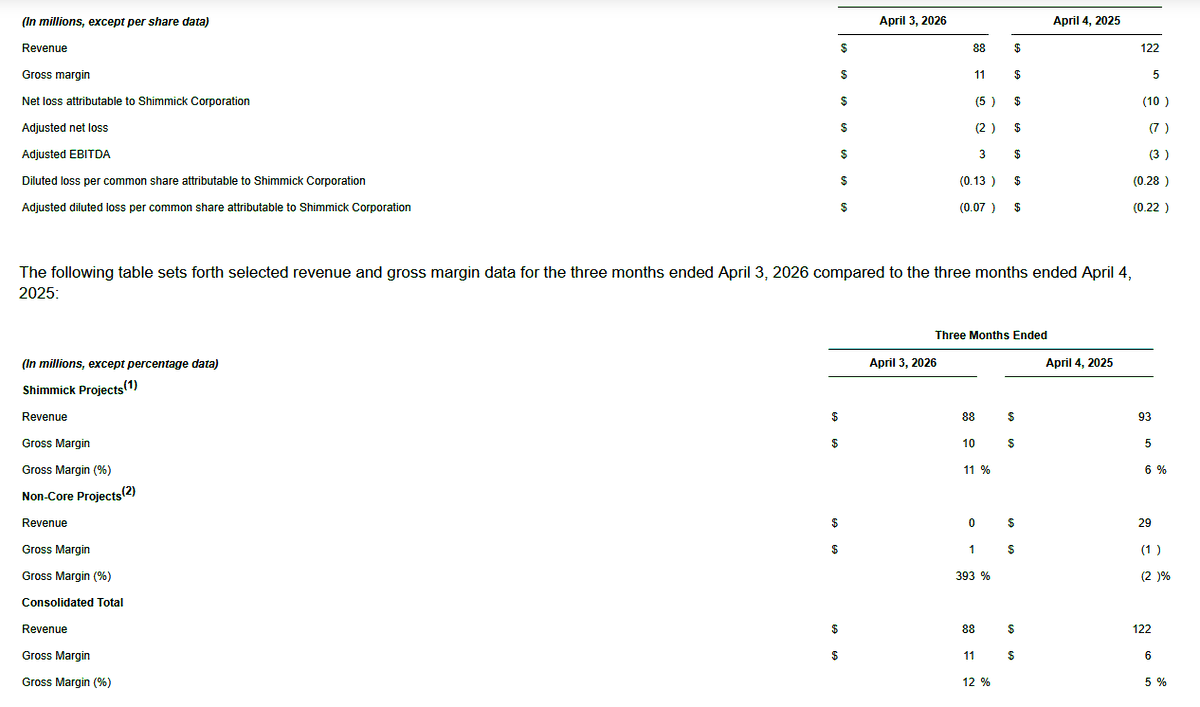

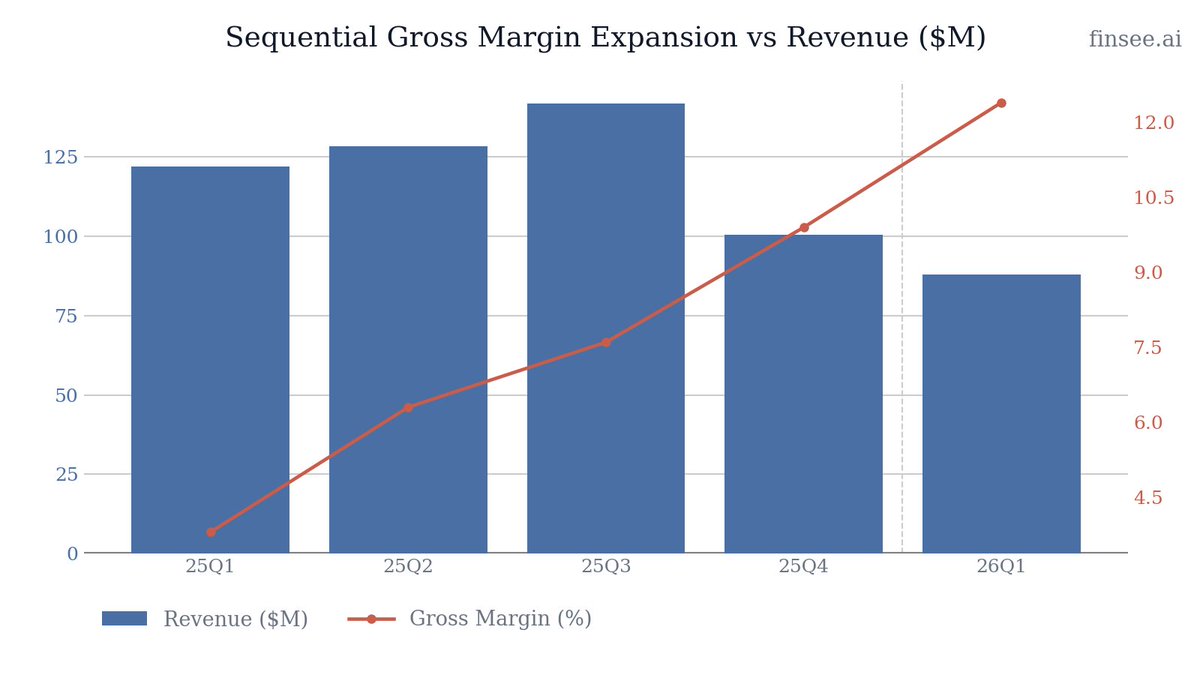

$SHIM Q1'26 Earnings are out.

Backlog of ~$944mm, highest since Q1'24.

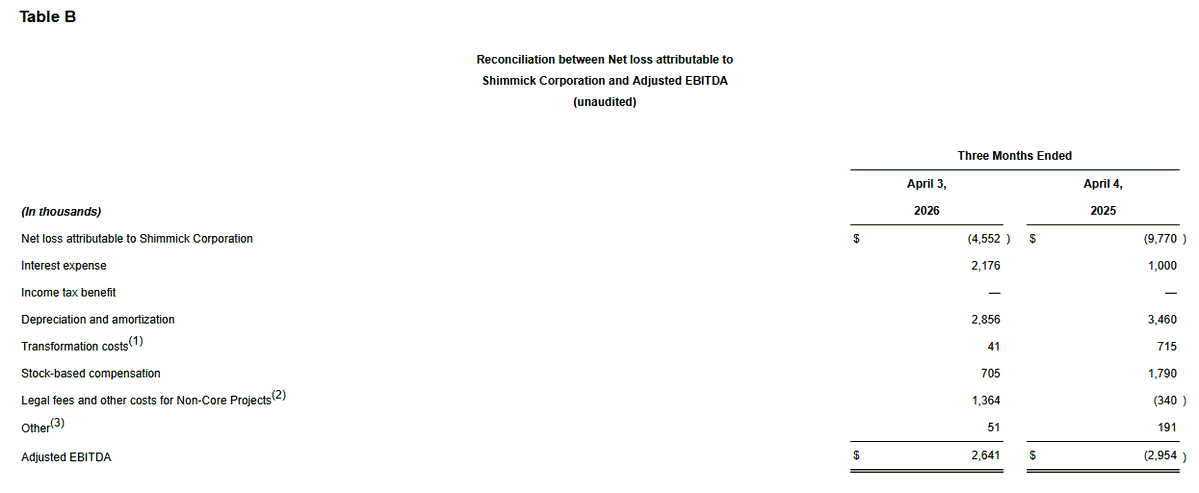

Adj. EBITDA of $3mm, continues to improve.

Gross Margin increased significantly, despite lower YoY revenue.

2.6x Book-to-Burn, its highest ever as a PubCo.

+$289mm of new awards in Q1'26

+$174mm of additional awards pending as of May 2026 in Water & Electrical target markets. Really great development.

FY26 guidance was reaffirmed:

Revenue: $550mm - $600mm (+17% YoY @ mdpt)

Adj. EBITDA: $15mm - $30mm (+350% YoY @ mdpt)

English

@Finsee_main I see... it's all about engagement, rather than usefulness. Tell me in a year how that business model worked out for you...

English

@SimplicitasOpes We published the article after the earnings release, when people look for info.

We published updates after the calls for many companies in previous quarters, they had 3x fewer engagements - people are not interested, unfortunately.

English

$SHIM Q1 2026 earnings: Short-Term Revenue Hit, Long-Term Margin Setup

Shimmick's Q1 results reflect a tale of two timelines. In the short term, revenue decelerated sharply to $88 million (down 28% YoY) due to adverse weather in California and Texas, slower project starts, and the deliberate wind-down of legacy projects. However, the forward-looking metrics are accelerating: backlog surged to a record $944 million driven by a massive 2.6x book-to-burn ratio. Furthermore, the company's margin transformation is cementing. Consolidated gross margin reached 12%, up from 5% a year ago, and Adjusted EBITDA printed its third consecutive positive quarter. The legacy 'Non-Core' drag is finally dead. However, to hit the reaffirmed FY26 revenue guidance ($550-$600M), Shimmick faces steep execution risks requiring a massive ramp in the back half of the year.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐋𝐞𝐠𝐚𝐜𝐲 𝐃𝐫𝐚𝐠 𝐄𝐱𝐭𝐢𝐧𝐠𝐮𝐢𝐬𝐡𝐞𝐝 — Non-Core Projects, which destroyed $68M in gross margin in 2024, are effectively finished. They generated just $0.2M in revenue this quarter, allowing the profitable 'Shimmick Projects' to dictate the bottom line.

• 𝐔𝐧𝐩𝐫𝐞𝐜𝐞𝐝𝐞𝐧𝐭𝐞𝐝 𝐁𝐚𝐜𝐤𝐥𝐨𝐠 𝐆𝐫𝐨𝐰𝐭𝐡 — The company booked $289 million in new work this quarter, yielding a 2.6x book-to-burn ratio. Backlog sits at $944 million (the highest since early 2024), providing massive revenue visibility if execution normalizes.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐒𝐭𝐞𝐞𝐩 𝐑𝐚𝐦𝐩 𝐑𝐞𝐪𝐮𝐢𝐫𝐞𝐝 — Printing only $88 million in Q1 means Shimmick must average over $160 million per quarter for the rest of the year to hit its $575 million guidance midpoint. This leaves zero room for further weather or start-up delays.

• 𝐋𝐢𝐪𝐮𝐢𝐝𝐢𝐭𝐲 𝐃𝐫𝐚𝐢𝐧 — Liquidity declined from $44 million at the end of FY25 to $34 million in Q1 2026. With negative operating cash flow (-$7.5M) and rising debt, the company needs these new projects to start generating cash quickly.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: ⚪

Neutral. The strategic pivot is working flawlessly on paper—margins are up, legacy work is gone, and the backlog is overflowing. But the sheer math of the Q1 revenue miss means the execution risk for the remainder of FY26 is dangerously high. Investors must monitor Q2 project ramp speeds closely.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢 𝐁𝐚𝐜𝐤𝐥𝐨𝐠 𝐀𝐜𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐭𝐨 𝐑𝐞𝐜𝐨𝐫𝐝 𝐇𝐢𝐠𝐡𝐬 [NEW]

The standout metric of the quarter is the $289 million in new awards, driving the backlog to $944 million—the highest level since Shimmick went public. Over 97% of this backlog consists of core 'Shimmick Projects'. The 2.6x book-to-burn ratio proves that end-market demand in critical water and electrical infrastructure remains incredibly robust.

🟢 𝐌𝐚𝐫𝐠𝐢𝐧 𝐐𝐮𝐚𝐥𝐢𝐭𝐲 𝐑𝐞𝐯𝐞𝐫𝐬𝐢𝐧𝐠 𝐏𝐨𝐬𝐢𝐭𝐢𝐯𝐞𝐥𝐲

Consolidated gross margins have officially completed their reversal from negative territory in 2024 to a healthy 12% in 26Q1. Shimmick Projects generated an 11% gross margin. This proves management's thesis: without the anchor of legacy projects, the core business is highly profitable and capital-efficient.

🔴 𝐒𝐞𝐯𝐞𝐫𝐞 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐃𝐞𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐨𝐧 𝐂𝐫𝐞𝐚𝐭𝐞𝐬 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞 𝐑𝐢𝐬𝐤 [NEW]

Q1 revenue plummeted to $88 million, down from $122 million in Q1 2025 and $100 million sequentially. Management blamed adverse weather and slower new project starts. However, maintaining the FY26 guidance of $550M-$600M means the company must rapidly accelerate production. If the newly appointed COO, Sarah Tacker, cannot immediately ramp up these awarded projects, guidance will inevitably be slashed.

🔴 𝐂𝐚𝐬𝐡 𝐁𝐮𝐫𝐧 𝐚𝐧𝐝 𝐓𝐡𝐢𝐧𝐧𝐢𝐧𝐠 𝐋𝐢𝐪𝐮𝐢𝐝𝐢𝐭𝐲

Shimmick burned $7.5 million in operating cash flow this quarter. Total liquidity dropped sequentially from $44 million to $34 million. While expected during the start-up phase of large infrastructure projects, this working capital drain is a concern given the sheer volume of new work coming online. The balance sheet has limited flexibility for further execution missteps.

⚪ 𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐒𝐡𝐢𝐟𝐭 𝐭𝐨 𝐂𝐨𝐥𝐥𝐚𝐛𝐨𝐫𝐚𝐭𝐢𝐯𝐞 𝐂𝐨𝐧𝐭𝐫𝐚𝐜𝐭𝐢𝐧𝐠

Shimmick continues shifting its backlog toward Progressive Design-Build and CM/GC models. This specific contracting innovation fundamentally de-risks the business, replacing fixed-price adversarial bids with collaborative cost-plus or guaranteed-maximum-price structures, ensuring the legacy margin wipeouts of 2024 are not repeated.

🔴 𝐑𝐢𝐬𝐢𝐧𝐠 𝐃𝐞𝐛𝐭 𝐏𝐫𝐨𝐟𝐢𝐥𝐞 [NEW]

Total long-term debt (including current portion) climbed to $68.6 million, up from $64.4 million at the end of FY25. Consequently, interest expense more than doubled YoY to $2.2 million in Q1 2026. This rising interest burden eats directly into the newly won gross profit, acting as a headwind to net income recovery.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀 (𝟐𝟔𝐐𝟏): $3 million

This marks the third consecutive quarter of positive Adjusted EBITDA (following $4.3M in 25Q3 and $3.7M in 25Q4). This stabilization indicates the operational turnaround is holding, even on lower absolute revenue volumes, proving the operating leverage inherent in the new project mix.

𝐒𝐞𝐥𝐥𝐢𝐧𝐠, 𝐆𝐞𝐧𝐞𝐫𝐚𝐥 𝐚𝐧𝐝 𝐀𝐝𝐦𝐢𝐧𝐢𝐬𝐭𝐫𝐚𝐭𝐢𝐯𝐞 𝐄𝐱𝐩𝐞𝐧𝐬𝐞𝐬 (𝟐𝟔𝐐𝟏): $14.3 million

SG&A remained essentially flat YoY ($14.4M in 25Q1). However, it is slightly higher than the $11M reported in Q4 2025. Keeping this overhead cost stable is the linchpin to achieving the 200-500% EBITDA growth projected for the year as revenue scales up.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐅𝐘𝟐𝟔 𝐂𝐨𝐧𝐬𝐨𝐥𝐢𝐝𝐚𝐭𝐞𝐝 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $550 million - $600 million

Accelerating. Reaffirmed guidance implies a massive ramp for the next three quarters. With only $88 million recognized in Q1, the company must average roughly $162 million per quarter going forward to hit the $575 million midpoint. This reflects management's confidence in converting the $944 million backlog rapidly.

𝐅𝐘𝟐𝟔 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀: $15 million - $30 million

Accelerating. Reaffirmed guidance targets 200% to 500% YoY growth. With $3 million secured in Q1, the company needs to generate approximately $6.5 million per quarter to hit the $22.5 million midpoint. This is highly achievable assuming the revenue volume materializes and Shimmick projects maintain their 10-12% gross margin profile.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐑𝐚𝐦𝐩 𝐕𝐢𝐚𝐛𝐢𝐥𝐢𝐭𝐲

With only $88 million in Q1 revenue, the math requires an average of over $160 million per quarter to hit your guidance midpoint. Exactly what quarter-by-quarter ramp are you modeling, and are those specific projects already mobilized in the field?

𝐋𝐢𝐪𝐮𝐢𝐝𝐢𝐭𝐲 𝐑𝐮𝐧𝐰𝐚𝐲

Liquidity has decreased to $34 million as operating cash flow remains negative during project start-ups. At what point in the year do you expect working capital dynamics to flip and operating cash flow to become positive?

𝐈𝐦𝐩𝐚𝐜𝐭 𝐨𝐟 𝐭𝐡𝐞 𝐍𝐞𝐰 𝐂𝐎𝐎

You highlighted the appointment of Sarah Tacker as COO to enforce 'disciplined execution'. What specific operational metrics or project control processes is she implementing to ensure the new backlog doesn't suffer the margin fade seen in past legacy projects?

English

@Finsee_main You don’t really need to know the company “deep” but if you had included $SHIM’s conference call transcript which clarifies several of the LLMs summary points, it would be far more useful, rather than slop.

English

@SimplicitasOpes Of course, if you follow the stock and know the company deep, you have a big advantage over llm. These articles serve two purposes:

1) provide a quick view - where people need to look deeper themselves;

2) tell regular folks what are the possible reasons it's up or down.

English

@BluthCapital Why does it always feel like this guy is talking his book when he opens his mouth… I suspect its just PTJ being who he is…

English

$OCC -- going to be very big, mgmt recharged stock comp auth. back in November because they clearly saw something big coming. I don't know timing of when this is reflected in reported earnings, but combo of low share count, lg proportion of fixed cost vs. variable cost and ramp up of Lightera JV is a recipe for an explosive stock.

English

Nynomic up 19% today!

My post yesterday outlined my modelling on their Nymomic, and their LayTec subsidiary.

TLDR:

- Nynomic (LayTec) are an undervalued chokepoint in InP/GaN MOCVD via $AIXA ramp

- At only 1.3x EV/Sales vs. names like $ONTO (10.7x) & $CAMT (13.8x)

As with any microcap, I expect significant volatility ahead.

But my modelling has built conviction that the market is yet to properly price-in LayTec.

Congrats to all who were earlier than me!

Paradis Labs@ParadisLabs

Thoughts on Nynomic ($M7U) at €145M MC: Caution: this is a numbers-heavy post where I walk through some of my modelling. No one’s really covered this on X since Nynomic doesn’t disclose subsidiary rev/margins. TLDR: Nynomic is very cheap at current 1.3x multiples vs metrology peers like $ONTO (10.7x) & $CAMT (13.8x). For a v. quick summary of the bull thesis: - Asymmetric exposure to photonics supercycle via their LayTec subsidiary - chokepoint in InP/GaN MOCVD via $AIXA ramp - $AIXA is 80–90% of global MOCVD Onto financials… -> By triangulating data points, I get to ~€15M revenue for LayTec in FY25: LayTec has ~800 installed reactors globally (based on customer list + historical $AIXA shipments + 25 years of sales) - New-reactor ASP: €95k / reactor - New reactors attached/yr (global MOCVD share, $AIXA + part of $VECO): ~100 units - New sensor revenue: 100 × €95k = ~€9.5M/yr - Service/software renewals: ~10–12% of installed base annually at €20–30k each = ~€1.5–3M/yr - Etch endpoint: ~€1–3M/yr -> Looking fwd to 2026: $AIXA Q126 orders were €171M at >65% opto mix. Call it €111M of opto equipment orders in a single quarter. If $AIXA’s FY26 opto revenue runs at ~€350M (conservative 62.5% of the €560M guide), and LayTec attaches at conservative 3–4% of reactor value on new orders: - That implies €10–14M of incremental LayTec revenue over the 2027–2028 recognition window. - So LayTec could reach €22–28M in FY27 layered on top of the ~€15M base I walked through above. Imo, the stock is starting to price in that inflection now. And consequently gives Nynomic a 1.3x EV/Sales multiple. That is very cheap against metrology pure-plays but fair against companies like Jenoptik who deal w/ photonics in Europe also. Imo, Metrology names would be a better/conservative comparison since the Nynomic group is ~80% photonics + ~20% metrology which acts as a drag on the financials. So I ultimately see Nynomic re-rating towards metrology names at least, like $ONTO/ $CAMT who have multiples of 10.7x & 13.8x. Especially if LayTec proves materially higher-growth and higher-margin than the wider Nynomic group. -> I currently hold a position in Nynomic.

English

@LynAldenContact Lol, they stopped testing Biden after the first week of his last term...

English

In the Stormlight Archives, there is a character (a king) who magically wakes up each day with a random intelligence level.

His caretakers test him in the morning to determine whether he’s capable of leading his country that day or is basically just given crayons.

Ryan Gentry@RyanTheGentry

Heads up: @claudeai is an idiot this morning.

English

@FactorOrigin @TomLeeTracker Dont disagree with you, although I was on the street when Cramer was running money and I don’t recall him being ’wildly successful’ maybe ‘mildly successful’ - I do remember most of the sellside not wanting to deal with him because he had some manner of recapturing commissions

English

People don’t understand the game. Jim Cramer for instance is dragged online because of his takes, meanwhile he has a show where people call up asking if they should buy or sell every stock in the market and whether he has intimate knowledge or not has to give a recommendation so people dunk on him, when in reality he ran wildly successful hedge fund and is worth 100-200 million dollars. Same goes for Tom Lee he was very succesful at JP Morgan and he now is a tv commentator when you have to give your opinion all day, obviously things will be wrong, when your creating hype around BMNR you have to go on speaking tours and get people excited you don’t do that without giving bullish outlooks. People forget Tom Lee on cnbc in 2017 telling people to allocate bitcoin to their portfolios as people laughed at him, tom Lee is no slouch be patient people.

English

TOM LEE SAYS A BIG DRAWDOWN IS COMING THEN THE RALLY OF OUR LIFETIME

- 10 of 13 new Fed chairs triggered a 10%+ drawdown in year one

- S&P on path to 7,300 then a decline that will feel like a bear market

- After that, we could see one of the strongest rallies of our lifetime

English

@HedgieMarkets Footnote: the UN thrives on crises, mostly of their own making. It supports their failed crisis of 'manmade global warming.' Whenever someone quotes the UN or World Bank or any form of woke World Economic forum, I'm afraid that's where I usually stop reading...

English

🦔The United Nations declared in January that the world has entered global water bankruptcy, a condition where depleted rivers, lakes, and aquifers will never recover to historical levels. The annual economic value of water and freshwater ecosystems is $58 trillion, equivalent to 60% of global GDP. Three billion people live in areas where total water storage is declining, and over 50% of global food is produced in those same regions.

By 2050, 46% of global GDP could come from areas facing high water risk, up from 10% today. Three major water disputes are intensifying simultaneously: Egypt faces potential $51 billion in agricultural losses from the Nile dam dispute, Pakistan has 23% of GDP tied to a river system now under treaty suspension with India, and the Colorado River's 2026 allocation renegotiation will determine water rights across seven US states producing a significant share of American winter vegetables and cattle feed.

My Take

I cover financial markets and the thing that strikes me most about this report is the absence of any pricing mechanism for what is being described. Water has no globally traded futures contract, no standardized risk metric, no liquid benchmark price. Agricultural land in water-stressed regions doesn't reflect declining aquifer levels. Sovereign credit ratings for countries where 30-40% of GDP depends on irrigated agriculture don't adequately weight multi-year drought probability. The $58 trillion in annual ecosystem value water provides has no insurance mechanism feeding into any financial model.

The three geopolitical disputes outlined here aren't abstract. Egypt is already the world's largest wheat importer facing a potential one-third reduction in water supply. Pakistan is managing debt restructuring and currency instability while the treaty governing 80% of its arable land sits in suspension. The Colorado renegotiation is happening now. These are near-term sovereign credit events dressed up as environmental stories, and the financial system has no framework for pricing any of them. The AI infrastructure buildout I've covered all year, the data centers consuming enormous quantities of water for cooling in already stressed regions, is a footnote in that larger story that nobody is connecting.

Hedgie🤗

English

For traders, I agree. For investors, not so much. The most successful investor I ever met is highly opinionated, has very little room for other's ideas and commits to his view and sticks with it. He buys and never sells, when he's wrong the stock may go to zero, but when's he's right he makes 100x or more. His largest holdling, now worth high 10-figures has been a 300x So, learn what works for you & do what works for you, there are no absolute right ways to invest.

English

Anyone with a functioning brain can trade stocks successfully—so then, why do few succeed on a big level?

Because few are willing to admit one simple truth: you suck!

Your head is full—sucky opinions, sucky assumptions, and “logic” that feels right but produces the wrong results.

As long as your cup is full, there’s no room for anything that actually works.

Empty it!!!

Strip away the ego. Discard everything you think you know.

Then find someone who’s already done it—at a high level—and shut up long enough to learn.

And finally, the hardest part: commit.

Commit to a strategy. Commit to your coach. Commit to the process. Commit to the belief that you can do it.

No dabbling. No second-guessing. No halfway effort.

Because success in this game doesn’t come from intelligence—it comes from discipline, humility, and coachability.

And most people fail because they lack all three.

You don't know shit! If you did, you would already be worth tens of millions of dollars. But I'm here to tell you that you CAN do it. Because I did. Anyone who tells you can't, never did it themselves. That's the final peace of the puzzle. Stop listening to losers and self proclaimed gurus. If they are so smart and they know how to teach you. Why haven't they done it for themselves. Do you really think someone who hasn't made 100 million dollars can teach you how to do it? If you do, then, that's why you'll never achieve it.

Mark Minervini@markminervini

Stop overcomplicating trading! -Buy the breakouts. -Cut your losses short. -Get aggressive when trades are working. -Cut back when they are not. Is that so fu&^ing hard? If it is, your probkem is in your head... read my mindset book. a.co/d/0ieuMg4l

English

@RaymondRavaglia @jaynitx Exactly, most of these studies pick one possible cause and build a thesis around it, when there are actually many possible causes - as you have suggested.

English

@jaynitx A different hypothesis: the poor learn failure from their parents. If there is a genetic basis for intelligence, the fact that these kids were IQ 140+ suggests that their parents also had higher IQs. Yet they were also poor. Perhaps bad culture is the common cause.

English

In the 1920s, a Stanford psychologist tracked genius children for 50 years.

Malcolm Gladwell breaks down what he discovered:

Rich families → successful. Poor families → failures.

Not average. Failures. Genius-level IQs that produced nothing.

He spent 60 minutes at Microsoft explaining why we're wrong about success:

The psychologist was named Terman. He gave IQ tests to 250,000 California schoolchildren.

He identified the top 0.1%. Kids with IQs of 140 and above.

His hypothesis: these children would become the leaders of academia, industry, and politics.

He tracked them. And tracked them. For decades.

The results split into three groups.

The top 15% achieved real prominence. The middle group had average, moderately successful professional lives.

And the bottom group? By any measure, failures.

The difference wasn't personality. Wasn't habits. Wasn't work ethic.

It was simple: the successful geniuses came from wealthy households. The failures came from poor families.

Poverty is such a powerful constraint that it can reduce a one-in-a-billion brain to a lifetime of worse than mediocrity.

There's a concept called "capitalization rate."

It asks a simple question: what percentage of people who are capable of doing something actually end up doing that thing?

In inner city Memphis, only 1 in 6 kids with athletic scholarships actually go to college.

If our capitalization rate for sports in the inner city is 16%, imagine how low it must be for everything else.

Here's something stranger.

Gladwell read the birth dates of the 2007 Czech Junior Hockey Team:

January 3rd. January 3rd. January 12th. February 8th. February 10th. February 17th. February 20th. February 24th. March 5th. March 10th. March 26th...

11 of the 20 players were born in January, February, or March.

This isn't unique to the Czechs. Every elite hockey team in the world shows the same pattern. Every elite soccer team too.

Why?

The eligibility cutoff for youth leagues is January 1st.

When you're 10 years old, a kid born in January has 10 months of maturity on a kid born in October. That's 3 or 4 inches of height. The difference between clumsy and coordinated.

So we look at a group of 10 year olds, pick the "best" ones, give them special coaching, extra practice, more games.

We think we're identifying talent. We're just identifying the oldest.

Then we give the oldest more opportunities, and 10 years later they really are the best.

Self-fulfilling prophecy.

The capitalization rate for hockey talent born in the second half of the year? Close to zero.

We're leaving half of all potential hockey players on the table because of an arbitrary date on a calendar.

Kids born in the youngest cohort of their school class are 11% less likely to go to college.

11% of human potential squandered because we organize elementary school without reference to biological maturity.

Now here's the part about math.

Asian kids dramatically outperform Western kids in mathematics. The gap is enormous and consistent across decades of testing.

Some people say it's genetic. It's not.

It's attitudinal.

When Asian kids face a math problem, they believe effort will solve it.

When Western kids face a math problem, they believe the answer depends on innate ability they either have or don't.

Here's the proof.

The international math tests include a 120-question survey. It asks about study habits, parental support, attitudes.

It's so long most kids don't finish it.

A researcher named Erling Boe decided to rank countries by what percentage of survey questions their kids completed.

Then he compared it to the ranking of countries by math performance.

The correlation was 0.98.

In the history of social science, there has never been a correlation that high.

If you want to know how good a country is at math, you don't need to ask any math questions. Just make kids sit down and focus on a task for an extended period of time.

If they can do it, they're good at math.

Why do Asian cultures have this attitude?

Gladwell's theory: rice farming.

His European ancestors in medieval England worked about 1,000 hours a year. Dawn to noon, five days a week. Winters off. Lots of holidays.

A peasant in South China or Japan in the same period worked 3,000 hours a year.

Rice farming isn't just harder than wheat farming. It's a completely different relationship with work.

There's a Chinese proverb: "A man who works dawn to dusk 360 days a year will not go hungry."

His English ancestors would have said: "A man who works 175 days a year, dawn to 11, may or may not be hungry."

If your culture does that for a thousand years, it becomes part of your makeup.

When your kids sit down to face a calculus problem, that legacy of persistence translates perfectly.

Now consider distance running.

In Kenya, there are roughly a million schoolboys between 10 and 17 running 10 to 12 miles a day.

In the United States, that number is probably 5,000.

Our capitalization rate for distance running is less than 1%.

Kenya's is probably 95%.

The difference isn't genetic. The difference is what the culture values and where it spends its attention.

Here's the most fascinating finding.

30% of American entrepreneurs have been diagnosed with a profound learning disability.

Richard Branson is dyslexic. Charles Schwab is dyslexic. John Chambers can barely read his own email.

This isn't coincidence. Their entrepreneurialism is a direct function of their disability.

How do you succeed if you can't read or write from early childhood?

You learn to delegate. You become a great oral communicator. You become a problem solver because your entire life is one big problem. You learn to lead.

80% of dyslexic entrepreneurs were captain of a high school sports team. Versus 30% of non-dyslexic entrepreneurs.

By the time they enter the real world, they've spent their whole life practicing the four skills at the core of entrepreneurial success: delegation, oral communication, problem solving, and leadership.

Ask them what role dyslexia played in their success and they don't say it was an obstacle.

They say it's the reason they succeeded.

A disadvantage that became an advantage.

Here's what Gladwell wants you to understand:

When we see differences in success, our default explanation is differences in ability.

We forget how much poverty, stupidity, and attitude constrain what people can become.

We refuse to admit that our own arbitrary rules are leaving talent on the table.

We cling to naive beliefs that our meritocracies are fair.

The capitalization argument is liberating.

It says you don't look at a struggling group and conclude they're incapable. It says problems that look genetic or innate are often just failures of exploitation.

It says we can make a profound difference in how well people turn out.

If we choose to pay attention.

This 60 minute Microsoft talk will teach you more about success than every self-help book you've ever read combined.

Bookmark this & give it an hour today, no matter what.

English

@MainooExtra @GoodPoliticGuy Almighty God is not restricted by a necessity to remain distant from human vulnerability.

True omnipotence is demonstrated not simply by remaining untouched by suffering, but by possessing the power to voluntarily enter it and conquer death from within.

English

The US president is praising Allah and Iran is defending the Pope, welcome to 2026

Masoud Pezeshkian@drpezeshkian

His Holiness Pope Leo XIV (@Pontifex), I condemn the insult to Your Excellency on behalf of the great nation of Iran, and declare that the desecration of Jesus, the prophet of peace and brotherhood, is not acceptable to any free person. I wish you glory by Allah.

English

@310Value @DeepSailCapital Condolences to Murray’s family, knew him well back in the day - we shared a common interest in deep value and underfollowed industries. RIP

English

@William53191104 @Rainmaker1973 Flew several times between NY & London. Time savings was helpful, but it was otherwise a non-event. I think our chairman had the record for most Concorde miles…

English

@Rainmaker1973 Yeah, and anybody who flew on it became, superstars just because they were a passenger. Everybody wants to know what it was like.👍🙋♂️

English

Yes. After about 10-15 questions within a single thread, you have to create a handover document and start a new chat— or go to a higher service level - this has to do with maxing out memory - once you hit the max, the AI cannot reference older data and attempts to bridge its own guess

English

Fact, AI is wrong often. I refuse to pay. I’ve gone back to Google search. AI leaves things out and/or makes things up. The longer your inquiry gets as you build on it the more it modifies its answers and it will randomly remove correct items previously provided in the same conversation. It’s limited. Unless you know that you will believe wrong or 1/2 answers.

English

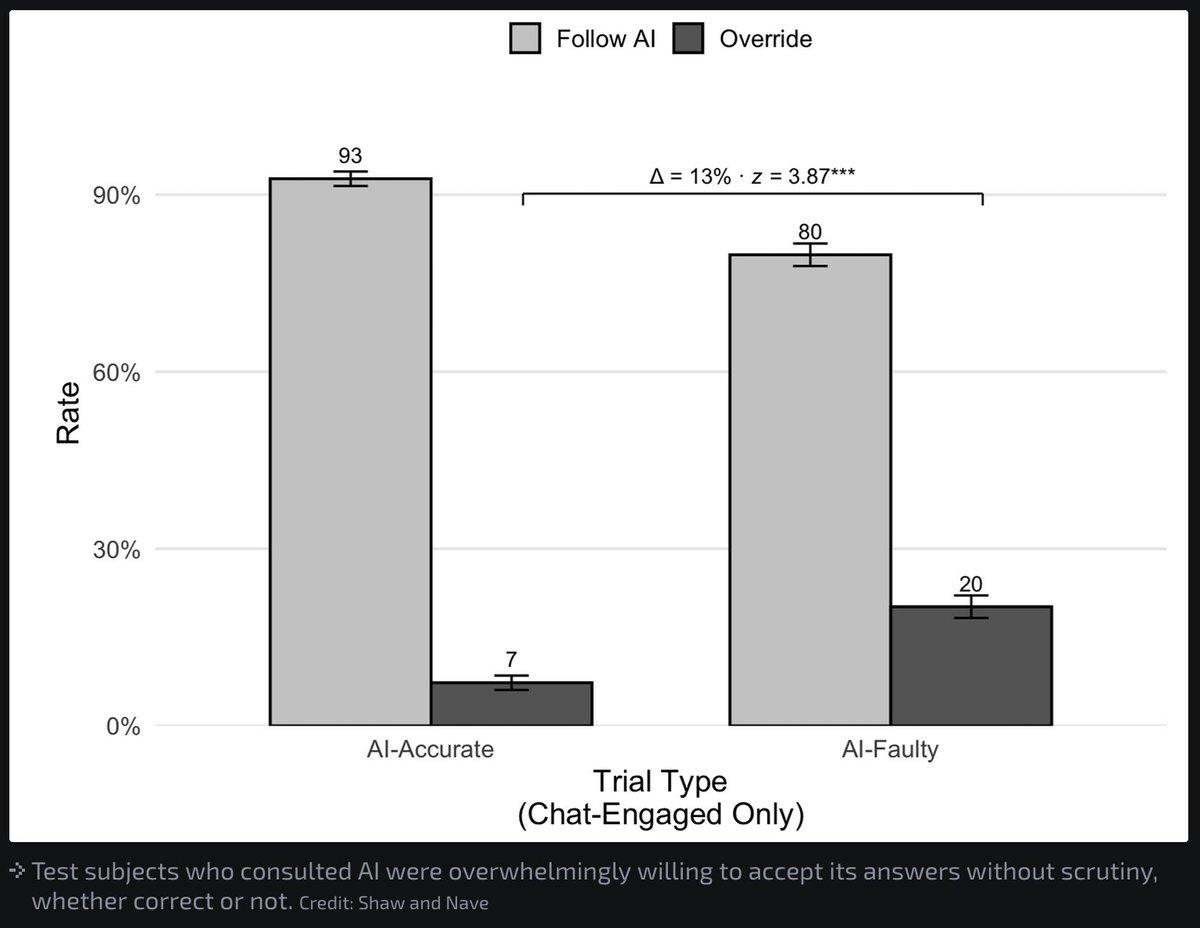

🦔Researchers at the University of Pennsylvania studied what they call cognitive surrender, the tendency to accept AI outputs without critical evaluation. Across 1,372 participants and over 9,500 trials, subjects accepted faulty AI reasoning 73.2% of the time and only overruled it 19.7% of the time. When the AI was wrong, users still accepted its answer 80% of the time. Subjects who used AI scored 11.7% higher on confidence in their answers despite the AI being wrong half the time. Adding time pressure made people 12 percentage points less likely to catch AI errors. Adding financial incentives and immediate feedback made them 19 points more likely to catch them.

My Take

The time pressure finding matters enormously for how AI is actually being deployed in workplaces. Companies are using AI to justify faster turnaround times, which means employees are using it under exactly the conditions that make them least likely to catch mistakes. When you're rushed, your internal monitor for detecting errors essentially stops firing, so you get AI output, no time to review it, high confidence it's correct, and a meaningful chance it's wrong.

People using a system that was wrong half the time still felt more confident in their answers than people who weren't using AI at all. That is a system actively making people worse at knowing what they don't know, which is one of the most dangerous things you can do to human judgment at scale. The companies pushing AI hardest into employee workflows should be reading this research carefully.

Hedgie🤗

Link to research for those interested: papers.ssrn.com/sol3/papers.cf…

English

@foundmyfitness But do you know what’s in the stainless steel - very possible it contains trace heavy metals which will be release md when exposed to acid containing juices…

English

Plastic blenders are a source of microplastics that most people overlook.

Those with plastic jars or pitchers release microplastics, and even nanoplastics, into blended food or drinks due to friction and mechanical abrasion during blending.

A single 30-second blending cycle can release up to 1 billion (yes, with a "b") micro- and nanoplastic particles.

BPA-free products are safer but can still release particles due to heavy use, heat, or abrasion. My advice is to switch to a completely stainless-steel blender. It's the only way to avoid contamination.

Thanks to @StevenBartlett for allowing me to audit his kitchen! Check out the full episode.

English

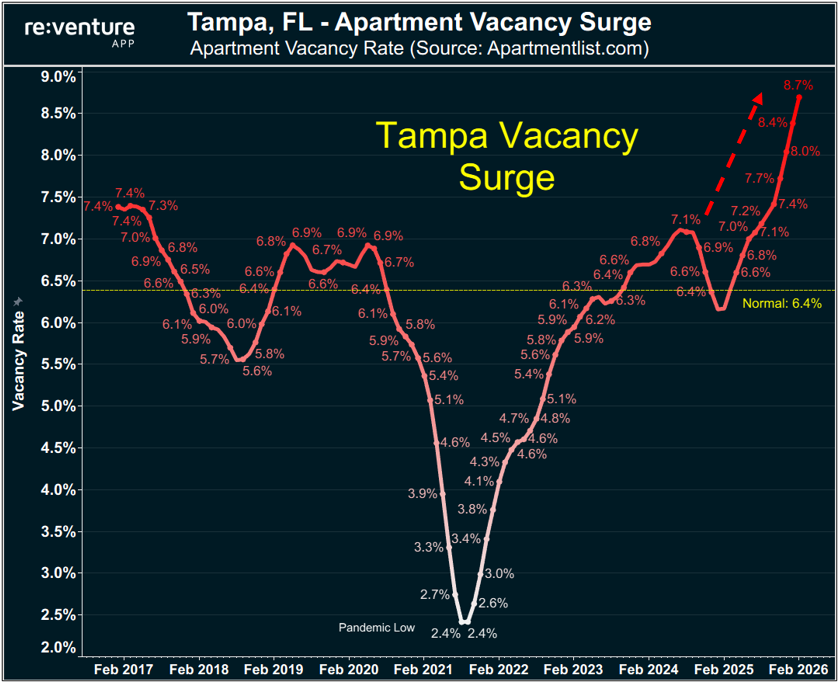

@nickgerli1 Depends on the neighborhood - there has been a tremendous increase in new supply. But certain areas with low crime & great schools north of Tampa (eg Lutz) still seem tight with quality properties moving in a few days to a few weeks.

English

What's going on in the Tampa Bay area?

Apartment vacancies just spiked to 8.7%.

Haven't seen anything like this in 10+ years.

They're going vertical.

English

@InvestorMexican @MSmicrocaps What happens if the big breakthrough, the big contract, etc. is announced 3 days after ur expiration…

English

@MSmicrocaps @SimplicitasOpes About position sizing and risk management, I think that the best approach with binary/catalyst stories is buying calls. That way you only lose the premium if things don't work

I initially bought the stock at ~$6 but sold at $5 to buy calls

English

$TGEN - Revenue down 12.5% YoY during Q4. Meaning there are no contracts yet 🤮🤮

Tomorrow's call has to be the best in history to avoid starting to think that this company has been diluting shareholders like crazy to invest in CapEx and OpEx to meet a demand that will never come.

English