Taylor Sugar

3.2K posts

Taylor Sugar

@TaylorSugar

LONG HARD : $MSTR + $BTC + $STRF + $STRC | SHORT $CAD | Scarcity + Demand | Max the Sats, Max the Income

Newmarket, Ontario Katılım Mayıs 2011

1.3K Takip Edilen1.2K Takipçiler

@TaylorSugar @askjussi REITs are likely to significantly underperform their historic rate of return in a new, higher rate environment. Plus work-remote is here to stay, and that is a secular headwind for office REITs

English

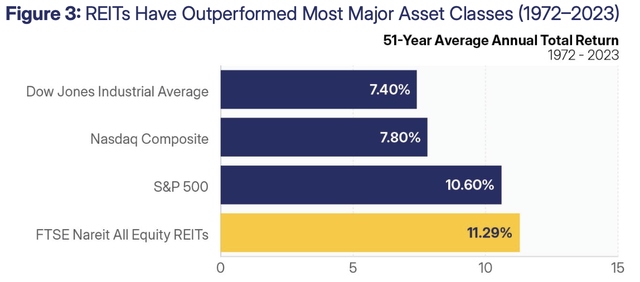

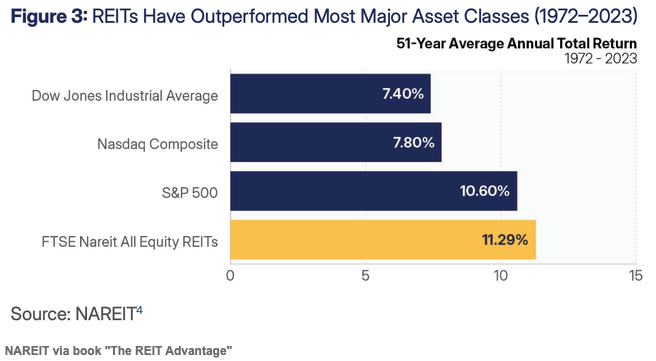

A lot of investors now view REITs as low-return income vehicles for retirees. That is backward. Over the longest time period available, REITs have actually outperformed the S&P 500 and even tech stocks. The last 5 years were rough, but that does not define the asset class.

$SPY $VNQ

English

@dampedspring Because they are targeting a $100 par value and price stability is a key feature in the STRC value proposition.

Rising volume signals product market fit.

English

$MSTR would be better selling $STRC here at 99.30 with no dividend instead of 100 yesterday with $0.95 of dividend but they won't cuz 🤷♂️

English

@danielfoch @RichardDias_CFA Don’t forget they increased the cmhc limit to $1.5M from $1M

English

In 2023 I predicted that the Ontario & Federal Government would be forced to bail out developers, and they'd do so quietly through policy reform. I provided 3 mechanisms that they'd use to do it.

2 of 3 have now happened:

1. You would see a large state-sponsored equity group buying units.

2. You would see a temporary GST/HST removal on units, making them 13% cheaper for these funds and developers to purchase.

3. They would adapt CMHC lending programs like MLI Select to accommodate large blocks of condos (you can use CMHC standard but not MLI yet)

Let's see if CMHC gives me the holy trinity on this prediction that literally ZERO people on here agreed with and most people said I was an idiot for coming up with 🤣.

English

@AdamBLiv STRF + MSTR is better as has more downside protection especially because you are not modeling an increase in strd price.

English

@HoyaCapital @DailyREITBeat Long term interest rate cycle a headwind for reits.

Structurally higher inflation a headwind

for reits.

Money supply sensitive assets > interest rate sensitive assets.

English

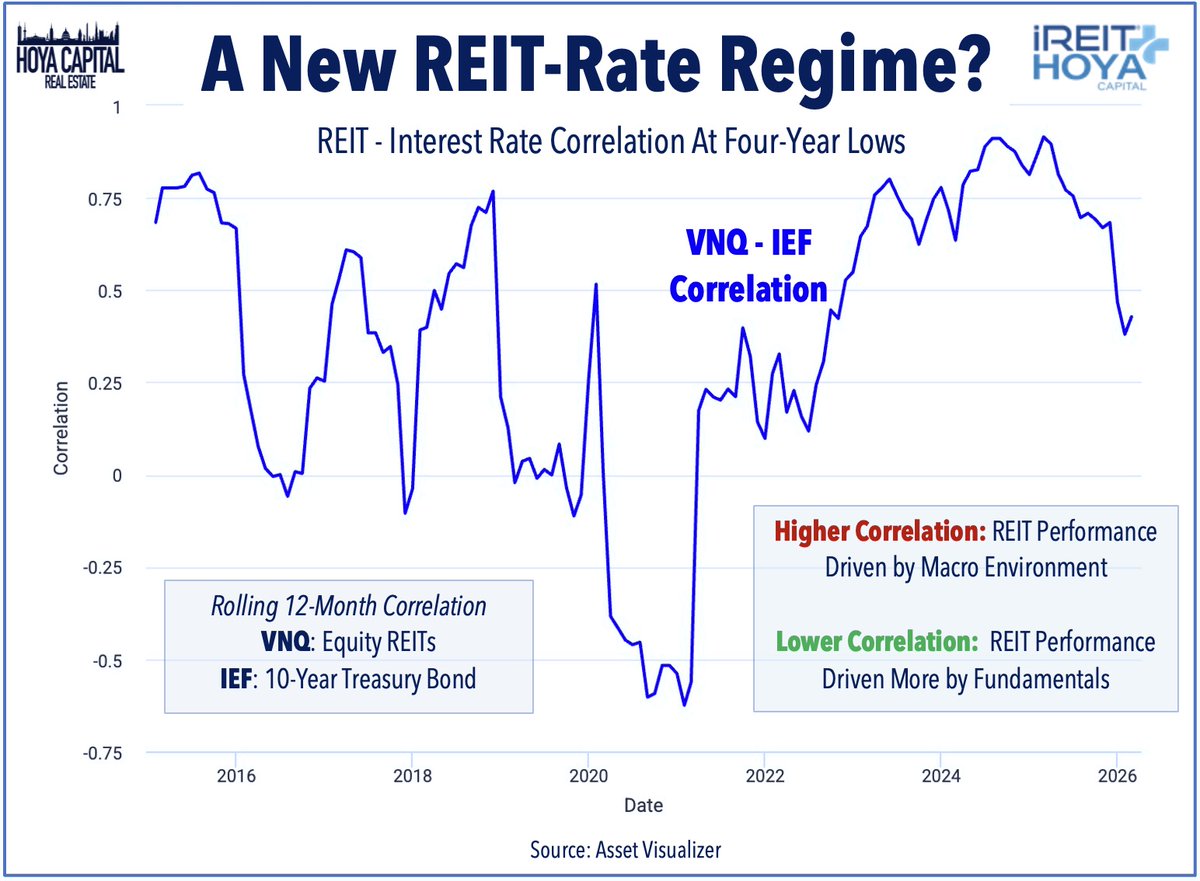

📊 A New Rate-REIT Regime?

State of REITs: seekingalpha.com/article/488543…

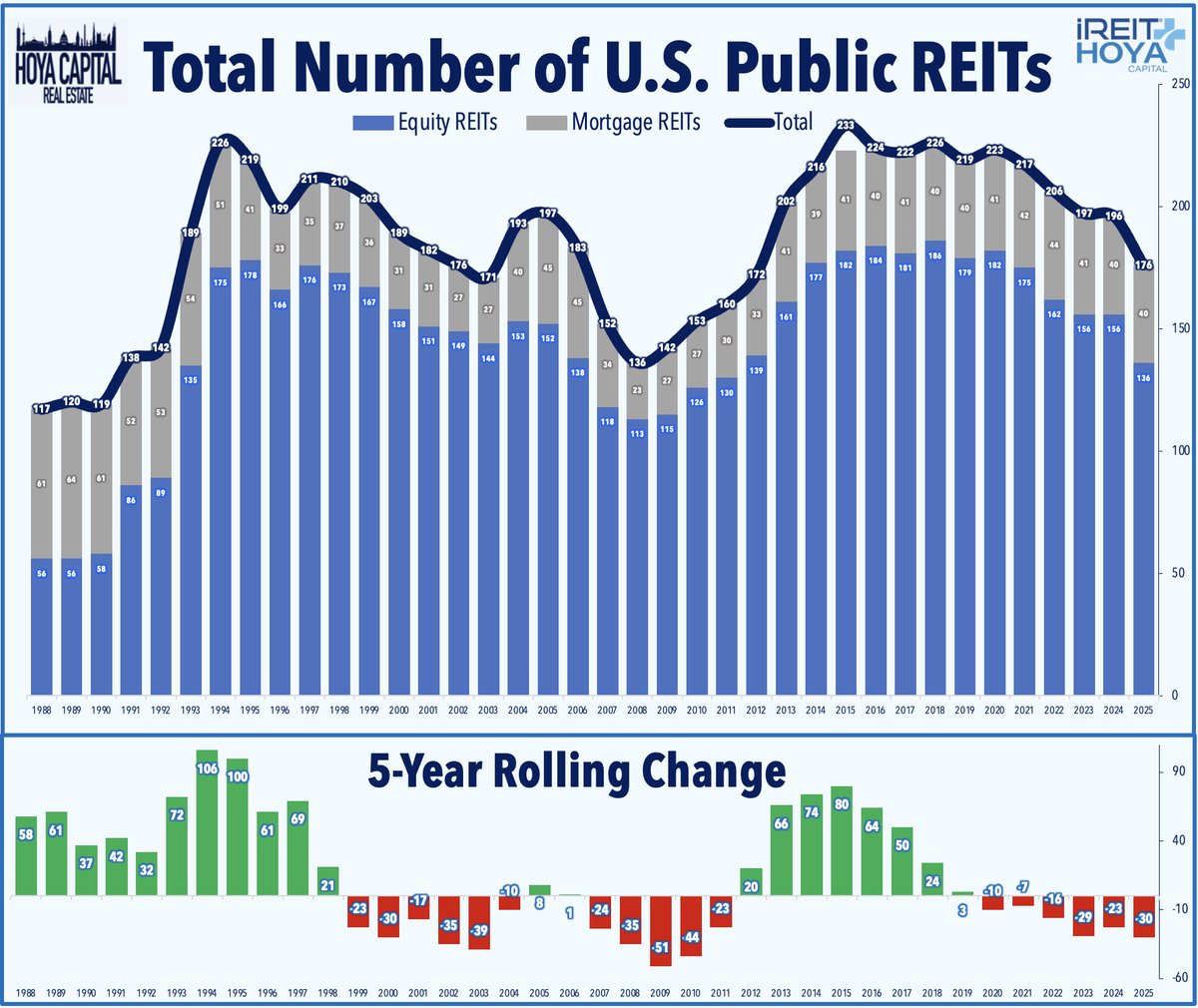

REITs were rolling out of the gates in early 2026, coming back into favor amid a HALO trade (Heavy Assets, Low Obsolescence) after a half-decade of rate headwinds and unfavorable narrative.

The oil price surge tied to the Iran conflict has complicated the rotation by sending rates soaring, yet REITs have remained surprisingly resilient in recent weeks, maintaining sizable year-to-date outperformance.

REIT-rate correlations have eased in recent quarters, signaling a more favorable "regime change" where performance is driven by property fundamentals rather than macro forces, following a prolonged period of rate-dominated.

Property-level fundamentals were not the culprit in the half-decade REIT bear market. Breaking the “rates up, REITs down” regime can finally unlock performance supported by resilient property-level operating trends.

Green shoots are emerging across the REIT landscape: companies are proactively unlocking shareholder value through asset dispositions and whole-company sales, while capital markets are reopening, highlighted by the successful IPO of Janus Living and improving transaction activity.

@AllTheREITNews | @DailyREITBeat | @ReitAcademy | @Alreits | @REITs_Nareit | @bradthomas

#REITs #Dividends #Investing

English

@HermesLux Agree that it eats into STRK and STRD but STRC success increases the collateral for STRF each week.

STRF has gone from 500% btc collateral to 710% btc collateral.

As STRF becomes safer eventually the yield should compress and the price should increase.

English

Not only is STRC eating all other fixed income and private equity, but it also appears to be eating into STRK, STRF, and STRD, not that it really matters—not every product can be number one after all.

Phong Le@phongle

Our digital credit vehicle achieved escape velocity this week.

English

@hillery_dan Higher energy prices increase the production cost of bitcoin.

Similar to increasing the replacement cost on real estate

English

STRC = Bitcoin network share buy backs.

I don't care about oil price.

English

@Convertbond Do it again from the end of February and the escalation of the Iran conflict

English

Hard Assets vs. Financial Assets in a Multipolar World

2026

Coal $CNR +33%

Oil & Gas $XOP +33%

Natural Gas $FCG +27%

Gold $GLD +16%

Uranium $URNM +16%

Silver $SIL +13%

Copper $COPX +6%

Nasdaq $QQQ -3%

Mag 7 $MAGS -9%

Banks $KBWB -10%

Bitcoin $IBIT -19%

English

@Rajatsoni Max Pain isn’t sideways.

Max Pain is NGU as the opportunity cost of not understanding bitcoin increases.

English

Max pain right now is Bitcoin's price staying at $70K for 4 years

All of the weak handed Bitcoin holders will rotate out to strong hands like me

My time horizon is 20+ years

I could potentially triple my stack if Bitcoin stays at $70K for 4 years

English

@askjussi Long term interest rate cycle has switched directions. Interest rate sensitive assets don’t have the tailwinds of the last two decades behind them.

English

After a historic bear market, REIT valuations are near historic lows.

Meanwhile, history shows 50+ years of double-digit total returns.

And unlike most sectors, active management in REITs has consistently beaten passive benchmarks.

This may be the opportunity cycle.

English

Stick a fork in it. Done. Beyond well done.

YEGWAVE@yegwave

According to a new Environics Institute survey, about 80% of Canadians say they trust Prime Minister Mark Carney.

English

Bricks 📉fall in gold over time.

Bitcoin📈rises in gold over time.

English

@CDInewsletter Ironically you could swap the titles and it still works.

English

$MSTR sure is one ugly chart.

-52% since mid-July. My God.

English

@BitPaine Don’t short decentralized scarcity in a world sick with centralized ♾️

Bitcoin is the cure for ♾️

English

this man is going to be in a breadline soon

James Wynn@JamesWynnReal

Adding to $BTC shorts here. Strong rejection at $105K after the SEE pumped due to $33bn injection. Bubble is getting bigger. - Wynn

English

@MPelletierCIO The only good bonds are Bitcoin bonds

$STRC $STRF

They offer real returns with yields above inflation 9-10.5% as well as tons of hard money collateral

English

@TheELongWave 50% cash is too dangerous with the printers and debasement

Perhaps I could agree with the permanent portfolio

25% cash 25% gold 25% bond 25% equities

Although the only bonds I like are Bitcoin bonds and I don’t like cash.

English

Most investors today remain fully invested — not as a deliberate strategy, but as a hopeful wish.

Across the advisory and FIRE industries, professionals are increasingly seeking unprecedented levels of research and insight to navigate this late-cycle environment.

My latest update on Substack provides detailed guidance and a prudent, evidence-based strategy designed to help advisors and investors protect capital and position for long-term success.

The TELTAAM Model continues to hold 50% cash, does this type of model appeal to you?

Click by bio for the link to the model.

English