@TommyDeepwater Which rigs do you think are the most likely/capable to be contracted for this project?

English

The Skewed Path

47 posts

@TheSkewedPath

Private investor with a focus on asymmetric investment opportunities. I publish my ideas on Seeking Alpha.

Oil shock. The Brent forward curve shows quick and steep disinflation back to the $70s level mid-term and the $80s short-term. via Bloomberg

STRANGE COINCIDENCE! My Q4 earnings live stream was taken offline prior to $PATH's call. Then their earnings stream gets taken offline halfway through, prior to Q&A Remember: Short interest has increased dramtically while at record low valuation, and at a time when ARR growth is finally reaccelerating and they just flipped fully GAAP profitable!!

@kimsin6 @OMGwen3rds8 Kim, cycle peak pricing will ensure they are built again

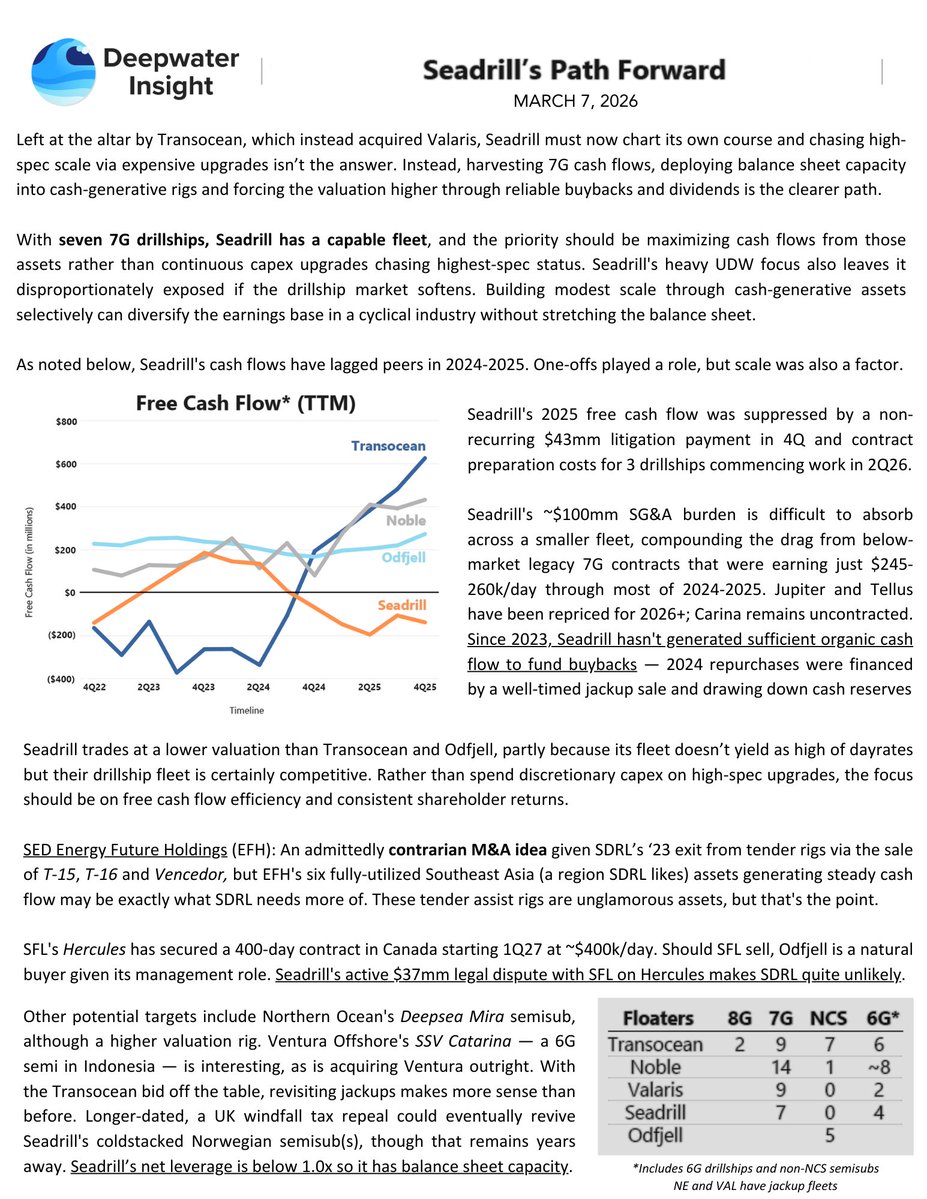

$RIG $TDW $VAL $NE I am in the processing of building "the bible" for offshore deepwater drilling market data. There is alot of talk about the fleet size but outside of the larger players it is a bit difficult to track what other companies own drillships and where they are operating. Here is how I am tracking the global fleet - if I am missing something please let me know. For the idle category some vessels are listed idle on a temporary basis like Noble Voyager or Valliant that are contracted but they just have white space until the contract begins. Would love any feedback from any of the other sharp folks that follow this market. @Ultradeep3 @TommyDeepwater @ICBarrett @offshoremayor