Tim Steffen retweetledi

Baird Director of Advanced Planning Tim Steffen discusses what high-income heavy savers need to know about this maneuver. spr.ly/6012BBT1di

English

Tim Steffen

5.7K posts

@TimSteffenCPA

Assisting @rwbaird Financial Advisors & their clients with tax and financial planning issues.

In this video, @TimSteffenCPA, Director of Advanced Planning, breaks down what you need to know about the future of Social Security, and how you can prepare. bit.ly/432STgF

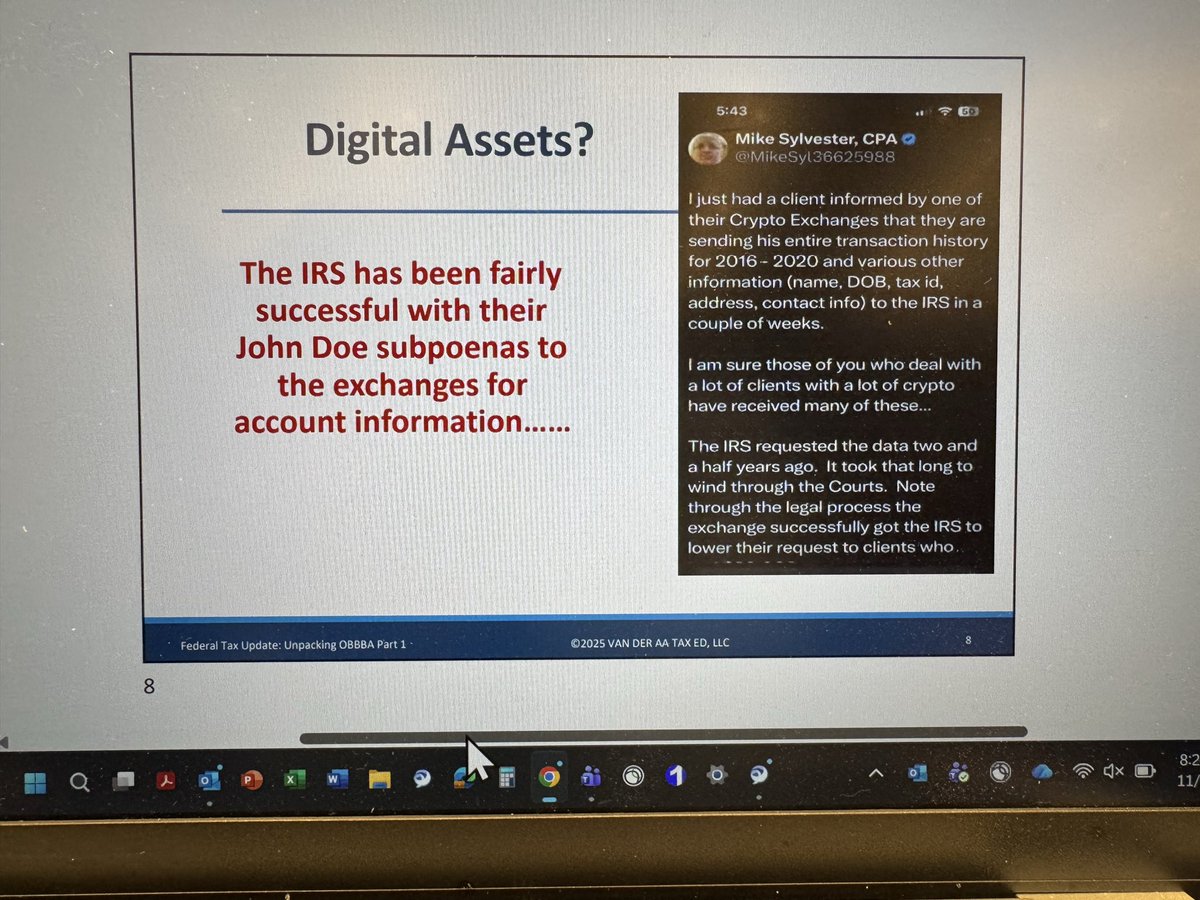

@FortWayneCPA you remain in this guys cpe presentation.

Bought 2 queen bees off marketplace, going to pick them up in Alexander County. If I don't return, my last words were "meet at the chicken coop, got it"