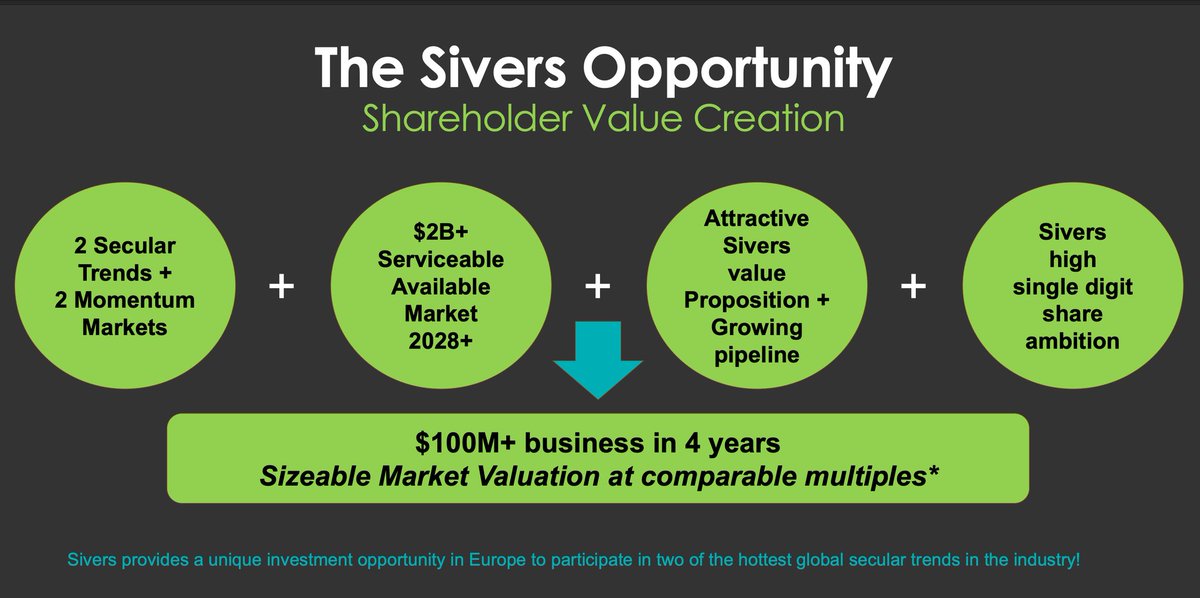

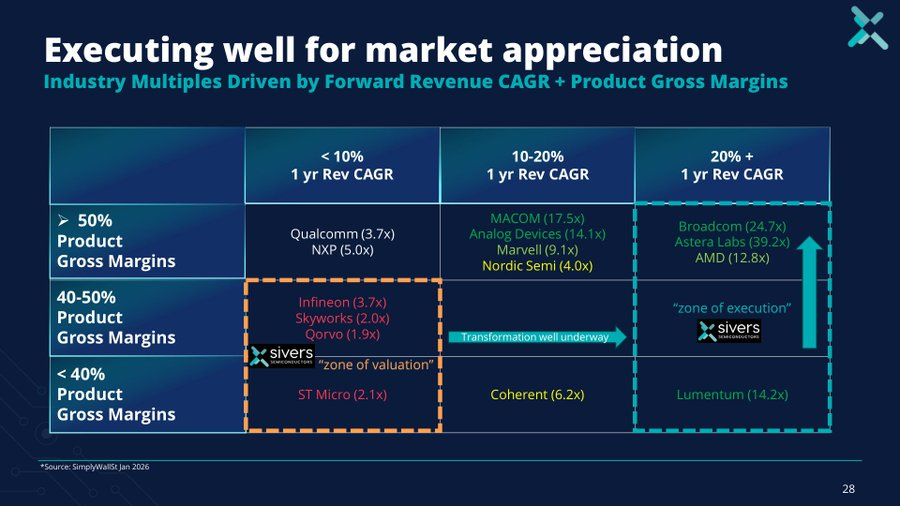

I actually thought $SIVE should be trading at $2B+ MC today (from ~$520m) if they were listed as a US company. Not later this year. Since I’m not sure how: - $LWLG trades at 3.5x+ the valuation - packaging companies that buy their lasers trade at 5-6x their valuation. - laser companies from $MTSI to $LITE have premiums trading in the tens of billions. And Sivers are in hyperscaler supply chains through $MRVL, $JBL, O-Net, and others rather than being dependent on one customer. There’s not very many publicly listed AI DC laser companies in the world either. So either it’s a highly sought after acquisition target for $AVGO or $MRVL that want to vertically integrate upstream. Or they can pull a $LITE that went from $17->$800 and downstream TAM expansion the ELS/optical transceiver stack through IP acquisitions. Depends how ambitious the company is of course but i just don’t think anyone noticed this laser supplier in Sweden since my thesis post. Just might require a little patience for the US listing and I’m almost certain US institutions are interested like they were with $IQE. DD periods usually last a few weeks after they read my thesis but I see a clear path to $10B+ MC from here over the next few years.