Brandon retweetledi

Brandon

2.1K posts

Brandon retweetledi

English

@ScottBarrettDFB @FantasyPtsData Just not true. Denver defense was very good but multiple teams had very good defenses. Bo was unreal. We saw the broncos without him and it wasn’t good. His game against Buffalo was goat level. It’s amazing how people can’t shed priors

English

Brandon retweetledi

As usual I will give my x earnings ($504.65) to someone who likes this post! Winner chosen at random on Sunday. For extra fun if the winner follows @joinnoblemobile I will DOUBLE it and if you are a Noble subscriber I will give you FIVE times the amount! Good luck! 😀🎉

English

Four teams. Two series. One path to the Cup. 🏆

Conference Finals picks are LIVE and every correct pick is worth 7 points (3x multiplier). If you're chasing the leaderboard, this is your round.

Top 5 teams still earn NHL Shop gift codes. Another $1,000 CAD cash draw hits when the round wraps.

And yes, the Habs are still alive. Let's go, @CanadiensMTL. Bring it home! 🔴⚪️🔵

Be sure to lock in your Conference Finals picks.

ndax.io/en/ndaxice

@NHL

English

QB Leaders in EPA per Dropback [Last 3 Years]

1. Malik Willis (0.42) 👀

2. Brock Purdy (0.23) 🔥

3. Josh Allen (0.21)

4. Drake Maye (0.19)

5. Lamar Jackson (0.18)

...

63. Desmond Ridder (-0.10)

64. Bryce Young (-0.10) 😨

65. Will Levis (-0.10) 👖

English

On April 8th, our lead crypto analyst @m0xt_ made three key calls.

Bitcoin $BTC. Coinbase $COIN. Galaxy Digital $GLXY.

One month later, those three are up 13%, 18%, and 65% (save this).

What's interesting is he wasn't bullish before that. @m0xt_ had been sitting in 75% cash for weeks because the downside was too hard to map out.

Conflict risk was high. Damage to crypto infrastructure was a real possibility. So he stayed defensive.

Then a few things shifted.

The risk of things getting worse lowered. The macro backdrop, while still messy, became easier to read. And sitting at 75% cash started to feel like leaving too much on the table.

So on April 8th, he made his move, buying a basket where the 3 biggest bets were:

→ Bitcoin (+13.24%)

→ Coinbase (+18.59%)

→ Galaxy Digital (+65.16%)

Sentiment turned. Galaxy did 5x the move of Bitcoin in a month. Coinbase did nearly 1.5x.

But he didn't go all in.

@m0xt_ still held 30% cash because the market was pricing things as 'fully fixed,' and he saw that as too hopeful.

There were (and still are) open questions around knock-on effects from supply chain issues, energy prices, and how lasting any sentiment recovery actually is.

Money in slowly. Dry powder ready in case things get rough again.

If you'd been a Milk Road PRO member on April 8th, this trade alert would have been sent to you the minute he bought.

(The exact entry, weighting, and reasoning behind each name.)

For everyone who watched crypto run this month and thought "I should have been in" - you could have been. For $1.

Access the full breakdown of the trade (and every other one we've made/will make) in the first comment 👇

English

@LateRoundQB Need some super late 4th round rookie dynasty sleepers! Or guys even undrafted in leagues?

English

If you have any questions for this week's mailbag episode, send them my way.

English

2,821 days in the making 🏆

Brandt Snedeker claims his 10th career PGA TOUR victory @MyrtleBeachCl – his first since the 2018 Wyndham Championship.

English

TPRR with 3+ WRs on the field over the past two seasons

(among a few teams that could be 11-heavy)

Chris Olave - .26 (13th)

Wan'Dale Robinson - .24 (21st)

Michael Pittman - .23 (28th)

Calvin Ridley - .23 (29th)

DK Metcalf - .21 (37th)

Devaughn Vele - .18 (58th)

@FantasyPtsData

English

crypto or AI, it doenst matter

Milk Road analysts are always on the forefront

we were early to crypto

early to get out of alts

early to crypto equities

early to shift into mag 7

early to AI infra stocks

were not perfect, but were consistent

get your $1 trial to PRO

Kyle Reidhead | Milk Road@KyleReidhead

missing the gains in AI stocks? turns out all you had to do was subscribe to Milk Road PRO for $1 and you would have been told months ago to buy $MU, $AMD, $CRDO, $NBIS and not shown here from another analyst, $BE and $INTC good luck solo searching for the next runners you can find the link in my bio, probably don't wait any longer

English

Brandon retweetledi

It’s @joinnoblemobile giveaway time! Just like this post and one person will get free wireless for a year, a ~$600 value. Winner chosen Saturday at random. The average American spends $83/month on wireless which is . . . twice what they do in other countries. 🤔 Good luck!

English

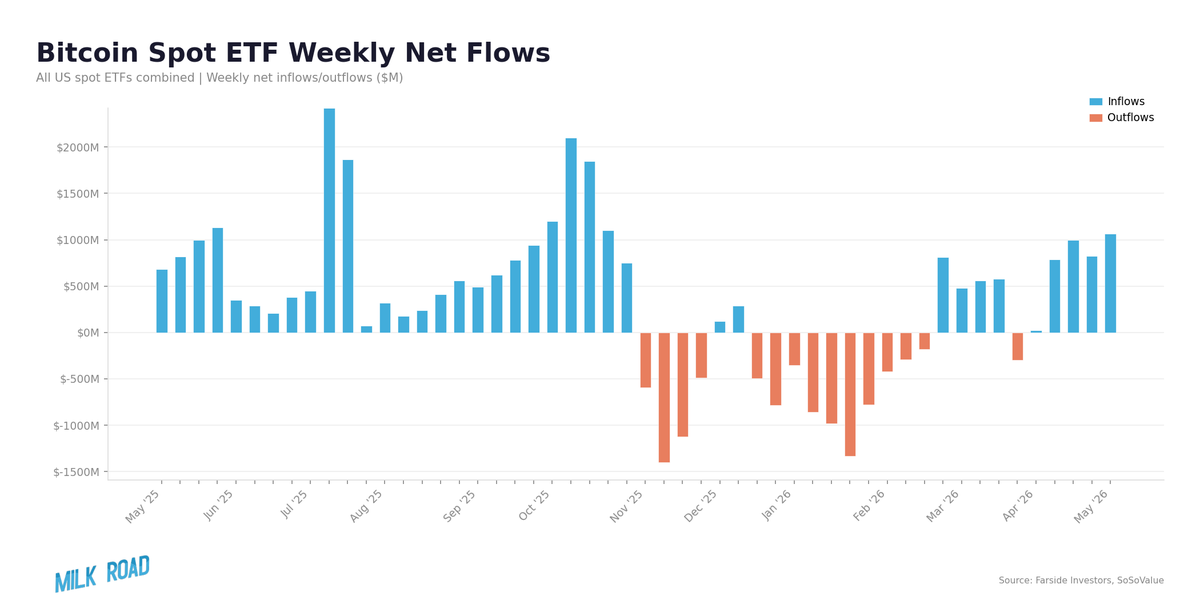

spot bitcoin ETFs on a 5-week inflow streak!

$2.4B poured in over april

they are back above $100B AUM

they had their best 5-week inflow since October

let the good times roll

English

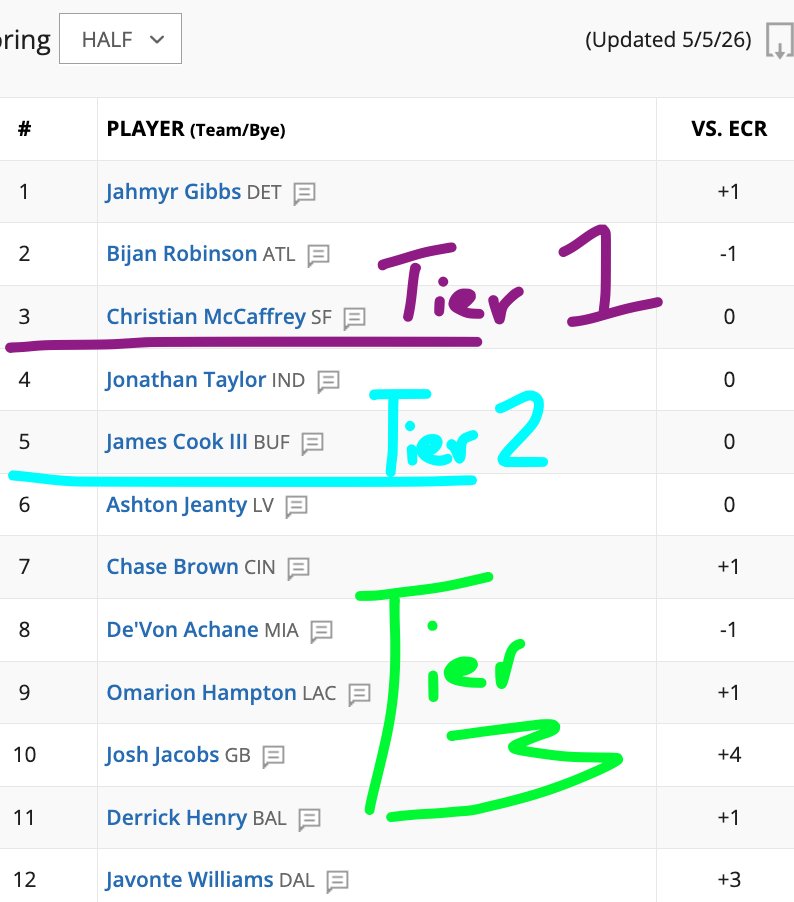

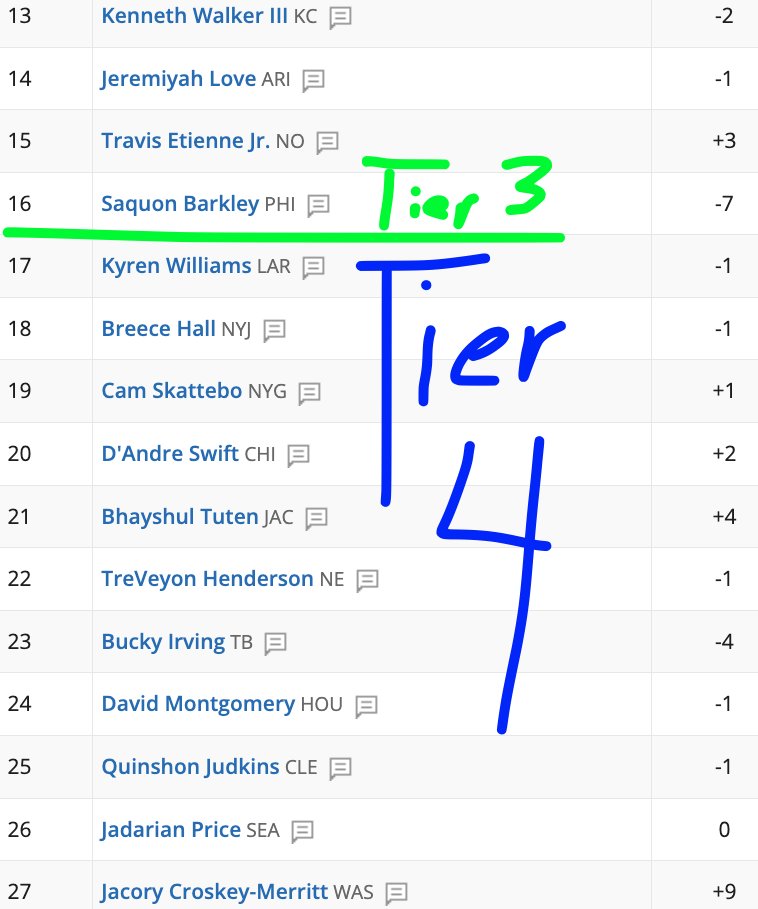

RB looks super deep for 2026 Fantasy Football

Here are my Half-PPR ranks. Tier 3 and Tier 4 are massive, very little difference between those players imo

Jacob Gibbs@jagibbs_23

New Beyond the Box Score! @dwainmcfarland and @DanSchneierNFL roasted my rankings! 2026 Fantasy Football Rankings (Top-75 RBs) youtube.com/live/fG1dooY7F…

English

SK Hynix gives you AI hardware exposure at ~3x 2026 earnings, while everyone else pays 30x for Nvidia.

But there's a better way to express the trade.

SK Square is a holding company with ~20% of SK Hynix sitting inside it, and that single stake represents roughly 95% of SK Square's value.

The discount has been sitting between 40% and 70% since SK Square was created in 2021.

What's different now is that closing that gap has become a stated management priority - and executive compensation is tied directly to hitting it.

That kind of comp structure is rare in Korea. The official target is below 30% by 2028.

Activists are pushing too.

Palliser Capital and Third Point have both built meaningful positions. Third Point has gone as far as suggesting SK Square take on debt against the Hynix stake to fund buybacks.

There's real pressure now, from inside and outside.

Milk Road@MilkRoad

Our lead crypto analyst just made his first pure-play AI investment. He's getting AI hardware exposure at ~3x 2026 earnings, while everyone else pays 30x for Nvidia. Here's what he found (bookmark this)... @m0xt_ has been hunting for a real AI hardware position for months. The more he uses AI every day, the more obvious it gets that this buildout is years away from peaking. The problem is valuation. Nvidia, AMD, Broadcom, the whole obvious basket - all priced to perfection. So he went looking for the company everyone needs but nobody talks about. That search led him to SK Hynix. The world's #2 memory chip maker behind Samsung. But the real story is HBM - high bandwidth memory. This is the data fast lane inside every modern AI system, the piece that lets Nvidia, AMD, and Google chips actually move data fast enough to train models. SK Hynix owns roughly 60% of that market and is Nvidia's primary supplier. Samsung and Micron are still trying to catch up on the tech. The latest quarter: Revenue up 192% year over year. Operating profit up 405%. Margins at 72%. Those are Nvidia-style numbers. The difference is almost nobody outside Korea is paying attention. SK Hynix trades at about 4.5x expected 2026 earnings. Micron, which is behind on tech and earns roughly half the profit per dollar of revenue, trades above 10x. The gap exists for one reason: SK Hynix is a Korean stock, and Korean stocks have historically traded at a discount over governance and access concerns. That's changing. The Korean government is pushing reform, and SK Hynix management has confirmed they're exploring a US listing. If that happens, the discount compresses fast. But @m0xt_ didn't buy SK Hynix. He found a better way to express the trade. SK Square is a holding company with ~20% of SK Hynix sitting inside it, and that single stake represents roughly 95% of SK Square's value. (The rest is cash and small investments.) The two stocks move with a correlation above 0.95, but SK Square trades at a 40% discount to the value of what it holds. So you're buying SK Hynix at a discount on a discount. (AI memory exposure at roughly 3x 2026 earnings.) The discount has been sitting between 40% and 70% since SK Square was created in 2021. What's different now is that closing that gap has become a stated management priority - and executive compensation is tied directly to hitting it. That kind of comp structure is rare in Korea. The official target is below 30% by 2028. Activists are pushing too. Palliser Capital and Third Point have both built meaningful positions. Third Point has gone as far as suggesting SK Square take on debt against the Hynix stake to fund buybacks. There's real pressure now, from inside and outside. Three independent ways this trade pays off: 1/ SK Hynix keeps compounding as the AI memory leader. 2/ A US listing re-rates the Korean parent. 3/ The SK Square holding company discount closes toward management's target. @m0xt_ started building the position two days ago. SK Square is up ~18% since. He's hoping for a pullback to add more, because he wants this to grow into one of his top three positions in his portfolio. Want to see the exact size he's putting on, where he's adding, and everything else in his portfolio? Check the link in the first comment.

English

I have several Dynasty Rookie Drafts going. SuperFlex 12-Teamers with TEP. Here are my first three picks in one of them. What do you think?

I still think Stribling and Williams are top values right now past the 1st round of Dynasty Rookie Drafts, ESPECIALLY Stribling. 📈

English

@jbchoknows Left side and try to win every year until you can't. A title is worth it!

English

🚨 MASSIVE TRADE OFFER ON THE TABLE!! 🚨 12-tm PPR Dynasty w/ TEP

Which side you got? Bonus points if you tell me why. Let’s hear it! 🤝

English