@0xFaust12 @macrocephalopod @therobotjames @robertmartin88 @witchqueendot @Mtrl_Scientist Can always count on @macrocephalopod + @therobotjames for useful insights

English

Coastal Quant

205 posts

@coastal_quant

Seasoned quant researcher.

Palus (@PalusFinance) provides better yields on idle cash for startups and SMBs, typically beating existing treasury services by 1–1.5% per year. Congrats on the launch, @Sam_Lushtak and @MichaelAtPalus! ycombinator.com/launches/PfC-p…

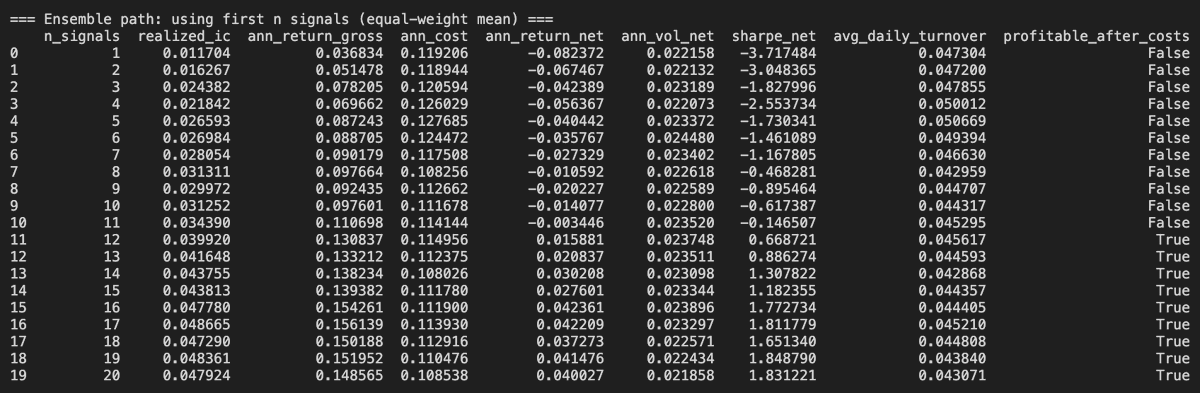

@Merridew__ @coastal_quant You combine a bunch of weak alphas into a stronger alpha. If they’re uncorrelated, that makes combining them *better* than if they were positively correlated! I honestly feel like we must be talking about completely different things or misunderstanding each other here.