@jasonfried wondering if the intermediate states, or this can be formalised (and understood) as ooda loop en.wikipedia.org/wiki/OODA_loop

English

Dean Crash

146 posts

Using a gif, which tv or movie character is most like you in real life?

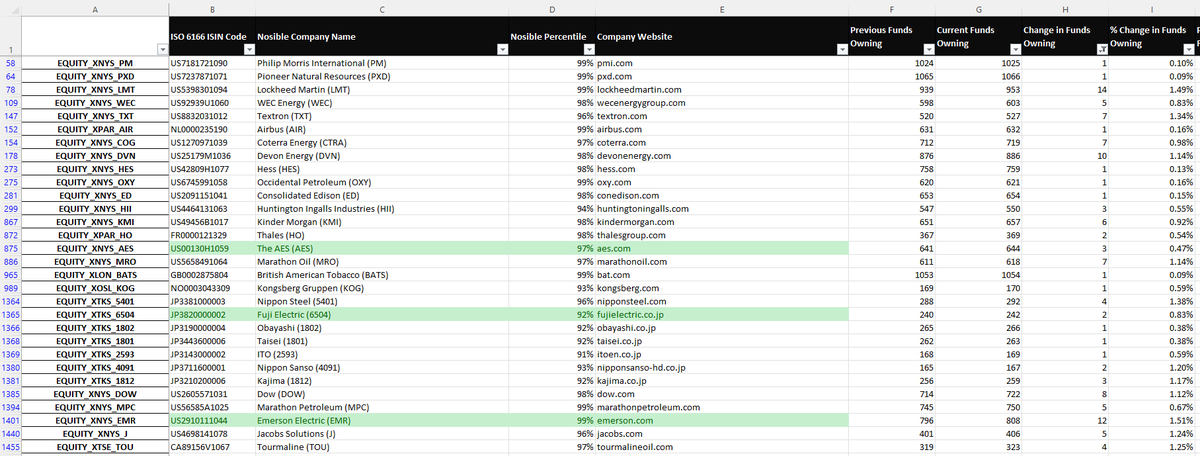

I'm excited. In less than 48 hours we are launching a new capability in @NosibleAI that will radically alter the ways in which our users can interact with our data and visualizations 🦾