Sabitlenmiş Tweet

on biotech platform strategy

in a new essay, @ElliotHershberg and I riff on biotech platform typology and partnering dynamics. we unpack why many biotechs pivot from external partnerships to internal programs, and why that trend might change in the near future.

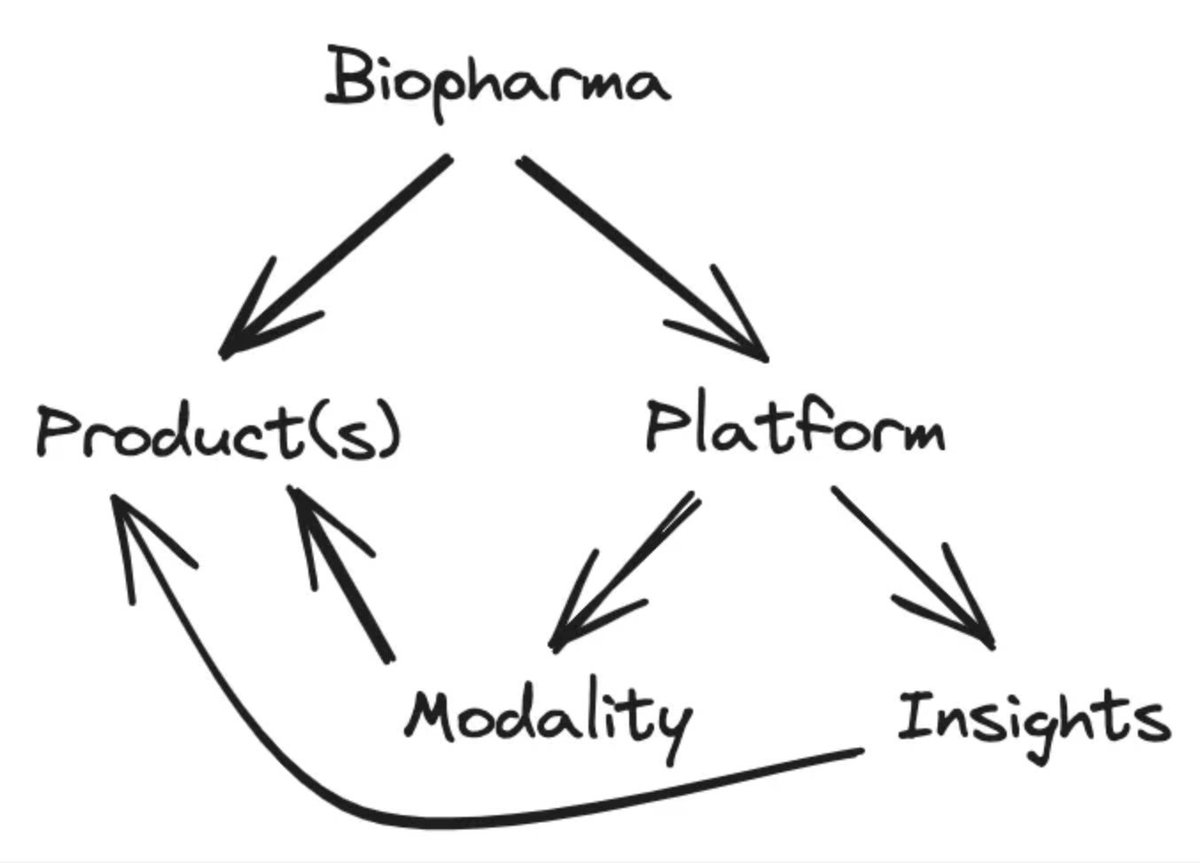

we start with a framework from biotech veteran Steven Holtzman for categorizing biotechs into product and platform companies, and the differences between therapeutic modality platforms and disease insight platforms.

the business strategy pursued by each biotech ultimately comes down to the details of the underlying technology, but historically, a vertical focus on internally developed drugs has been the most successful value creation strategy in all of biotech.

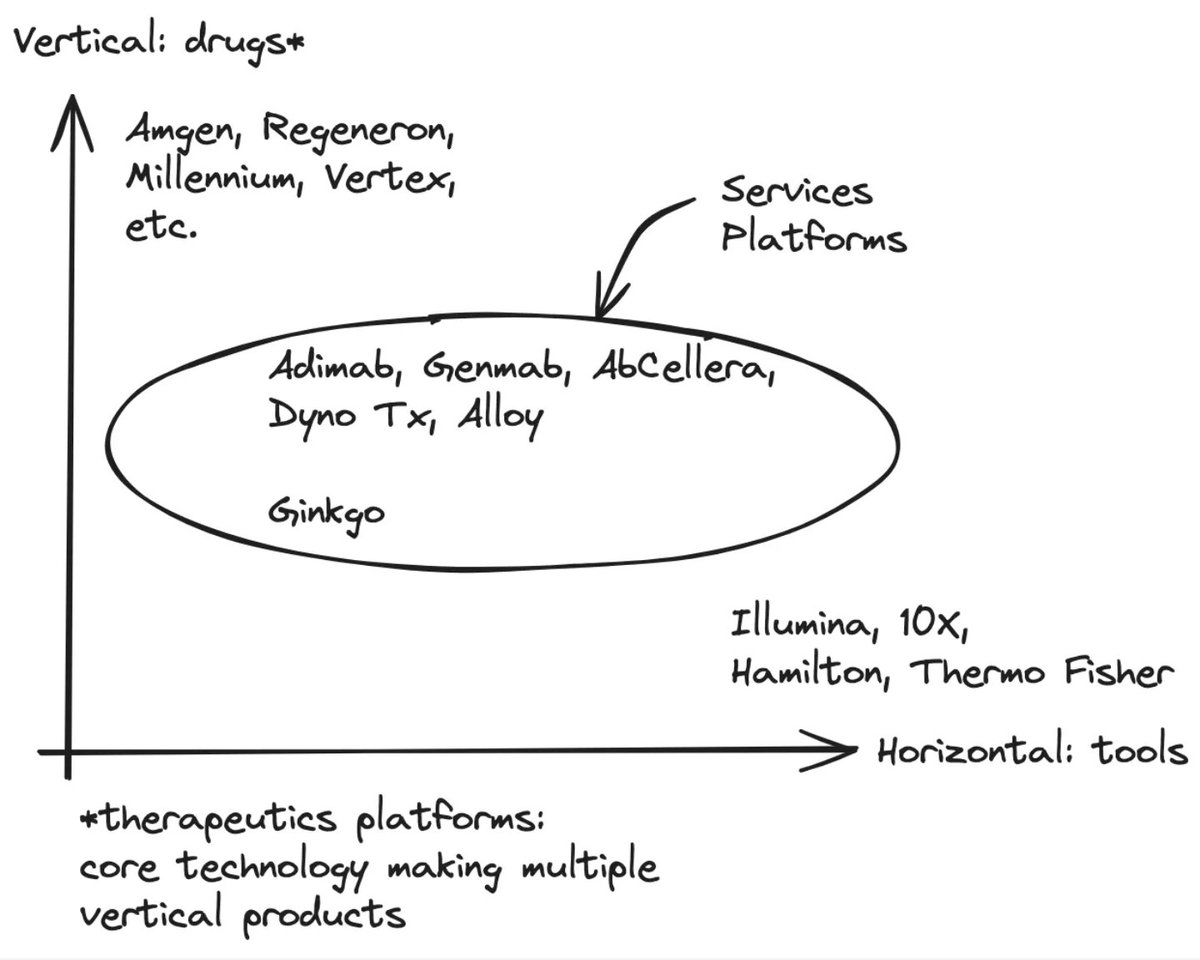

building a services platform, which exclusively pursues external partnerships with no internal pipeline, is really, really hard. the list of companies that have done this successfully is short, and many end up shifting strategy to developing their own wholly owned assets.

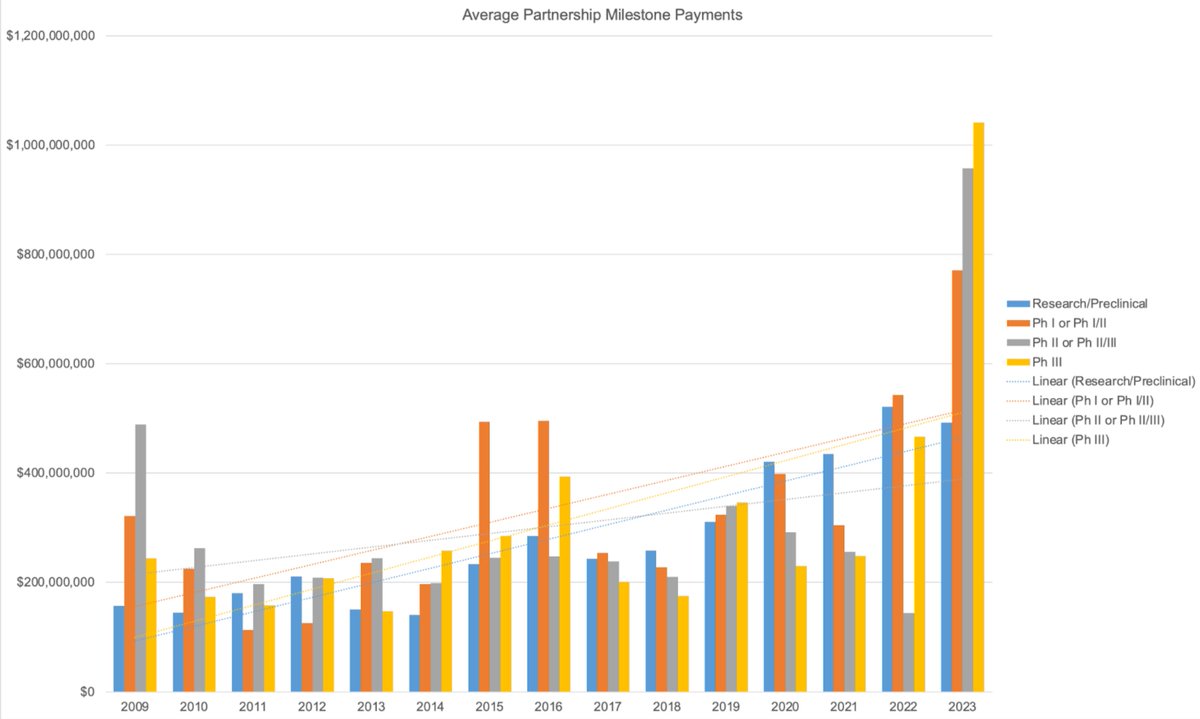

a partnership-only business model in biotech has been difficult to scale successfully, but will this trend continue? to address this question, we analyzed data from biopharma partnerships over the last ~15 years.

if platform technologies are becoming more proven and validated, average partnership deal value should increase over time. if average deal value continues to increase, at some point it will be feasible (and even preferable) to pursue a services/partnerships-only model as a platform biotech.

we found a trend towards increasing average total deal value, average milestone payments, and total number of partnerships over time, effectively increasing the total addressable market for services platforms.

there are some important caveats and confounds with these data, but qualitatively, these trends suggest that there may be a shift in pricing power from partners to technology platform developers. if this trend continues, external partnerships as a mechanism of value capture will improve relative to wholly owned internal programs, thus improving the scalability and success-rate of services platforms in biotech.

this was a fun one to write. the full piece is packed full of perspective and conjecture worth disagreeing with, so reach out if you want to discuss!

English