Loplop

4K posts

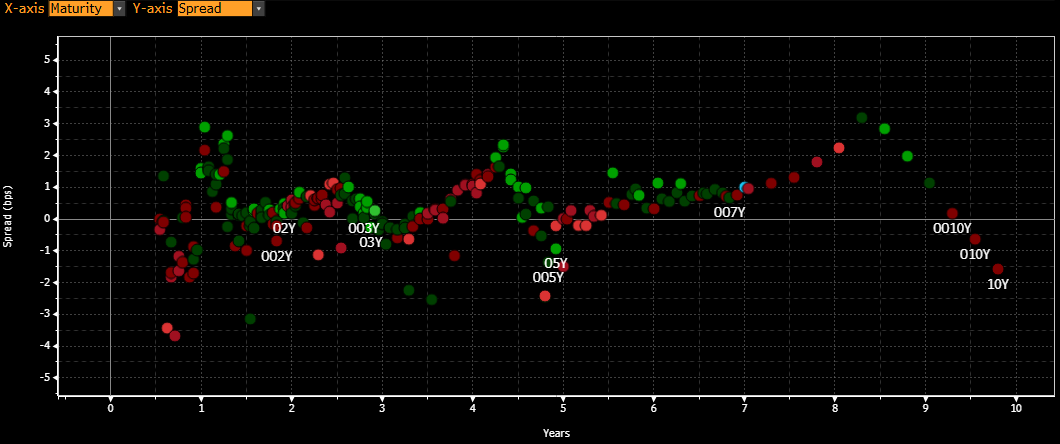

Some thoughts on the US rates curve: Not thinking about bullish vs bearish - that’s data/war dependent, and the path of least resistance is bearish until June FOMC.

The question is, if we do sell, should the curve bear flatten or steepen, and especially in the 2s5s or M7-M8 part of the curve? For 2s5s to bear steepen, two specific conditions have to be met:

1. Data (both inflation and unemployment) remains hot, removing any doubt that the Fed should be raising rates

2. The rhetoric from the Fed remains dovish relative to the data (perhaps driven by Warsh, or if Cook and Powell leave and are replaced by Miran and Kelton?)

1+2 would imply that the Fed is strictly behind the curve, and that policy response would be delayed, which means it would also have to be bigger, and this would be bearish for the belly.

Otherwise, the curve should flatten in a bearish move because there’s a good chance that the inflation effect disappears after June 2027.

So, based on this framework, one can determine what the market is thinking about data and the Fed's stance.

English

Substack is the most complete. To be clear, I have been emphasizing that the recovery in cyclical sectors was occurring and expected. The rest of it, especially labor gains, will be revised away. "So the warning signs are there — credit and quality are flashing warning signs. Markets will remain resilient due to passive factors until they don’t."

English

"Learn a trade!"

"Riveting?"

Truflation@truflation

🚨 Listen to the recording of a riveting macro discussion with - Truflation's Head of Data, Oliver Rust @orust99 - Truflation CEO @therealsrust - Heritage Foundation's @RealEJAntoni - Mike Lee Strategy @MikeLeeStrategy - Bianco Research @biancoresearch - Simplify Asset Management @profplum99 Come back next month for the May CPI release, June 10th, 2026. x.com/i/spaces/1wGWj…

English

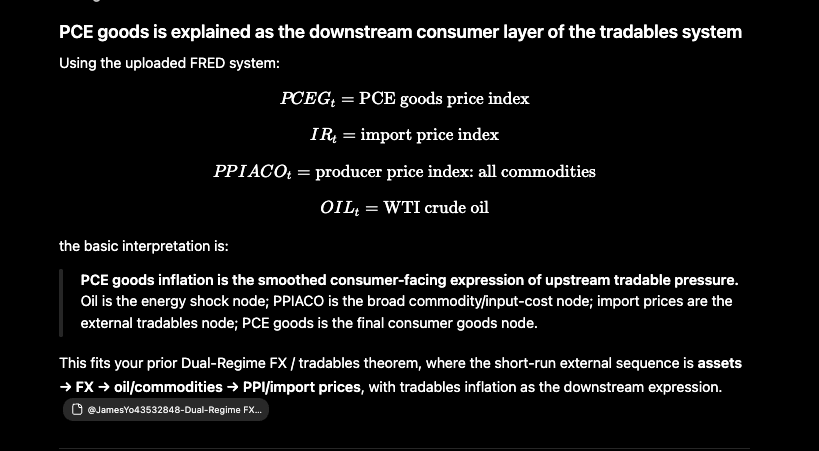

PCE goods is explained as the downstream consumer layer of the tradables system

The system looks like this:

OIL → PPIACO → IR → PCE goods

PPIACO is the best single explanation of PCE goods inflation: R2≈0.81

English

English

There are rumors that early SpaceX investors won't have a traditional 6-month lock up period.

If that's true @MunchingMoez says the S-1 alone could cause a market sell off. @MTSlive

English

Loplop retweetledi

@real_checkmark That's as much as I'm willing. Think about all possible investors and all their demands to spend, wages, leverage, issue to finance spending, finance the fiscal deficit, manage their sovereign wealth etc.

English

My handle/business name was based on the model below

Today

The size of the market/economy M is extremely large

K is super "springy"

C is as dampening as I have ever seen in "normal" economic conditions

X "bumps" are more impactful than normal as geopolitical and technological disruption AND distrust of data add more impactful surprises

This system is as fragile and overdamped as I have ever seen since developing this idea 35 years ago

Andy Constan@dampedspring

Damped spring model for volatility 101. This thread is about the concepts I use to model future volatility based on the idea that news moves markets to new equilibriums and conditions of participants and external stabilizing agents dictate the path that markets take on the way.

English

@rev_cap @MelMattison1 even lancaster where the amish are in PA is too expensive for only $1M

English

@maxwiethe @pernasresearch if they have a repeatable edge then why would they share it by selling research?

English

Unlike most independent researchers, @pernasresearch has an audited real money track record.

Since inception they've annualized >30% pernasresearch.com/performance-ve…

Monetary Matters listeners can get a 20% discount on their first year of Pernas Research at: pernasresearch.com/monetarymatters

English

📉 Is the SaaS era over? Software stocks have been in free fall, and @pernasresearch says the market is missing a massive, nuanced opportunity.

Full episode out now👇

YouTube: bit.ly/4tXnTcY

Spotify: bit.ly/4vFOOLS

Apple: bit.ly/4cyRZwl

English

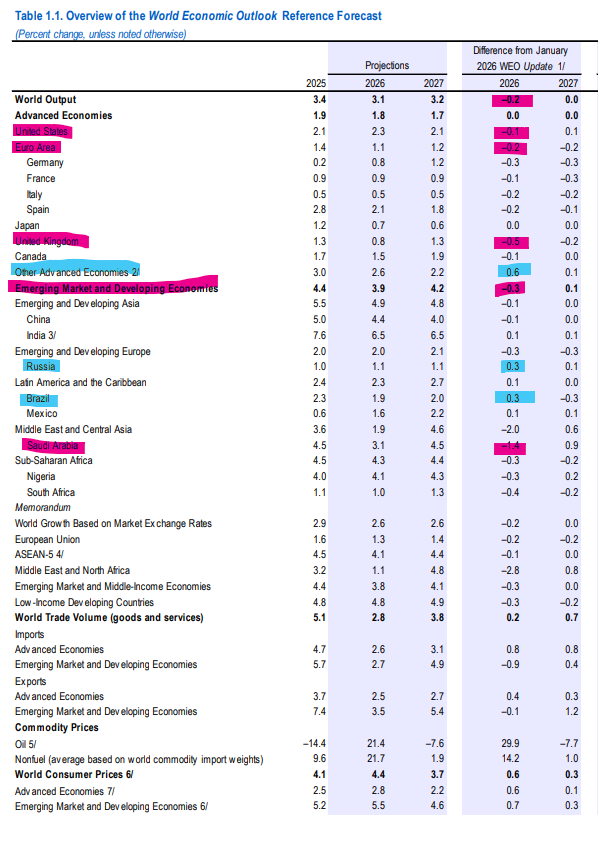

IMF cut 🌍 GDP f/cast by 20bps due to war. Recall last Apr WEO was 🔪by 50bps on tariffs but world output (🇨🇳 in particular) pushed on regardless. For all its failings #IMF must err on side of caution. Weirdly EM & G7 led downgrades yet "advanced others" got upgraded 0.6%. Who?🧩

English

Loplop retweetledi

Instead of building a forecast from scratch, which is an exercise in compounding guesses, you take the price the market is giving you and gradually work backward: what growth rate, margin, duration of competitive advantage does this price require to be justified?

Then the only question is: is that plausible or insane?

That's a dramatically easier cognitive task. You're not predicting the future. You're evaluating whether someone else's implied prediction is reasonable. Falsification rather than construction, Karl Popper would approve.

And it naturally surfaces the best opportunities: cases where the market's implied assumptions are obviously wrong in one direction. You don't need to know what a company is worth to know that the market is pricing in something that can't possibly be true.

@mjmauboussin has formalized this as "expectations investing" and it's probably the most intellectually honest valuation approach available. It admits what you can't do (forecast) and focuses on what you actually can (judge plausibility).

English

English

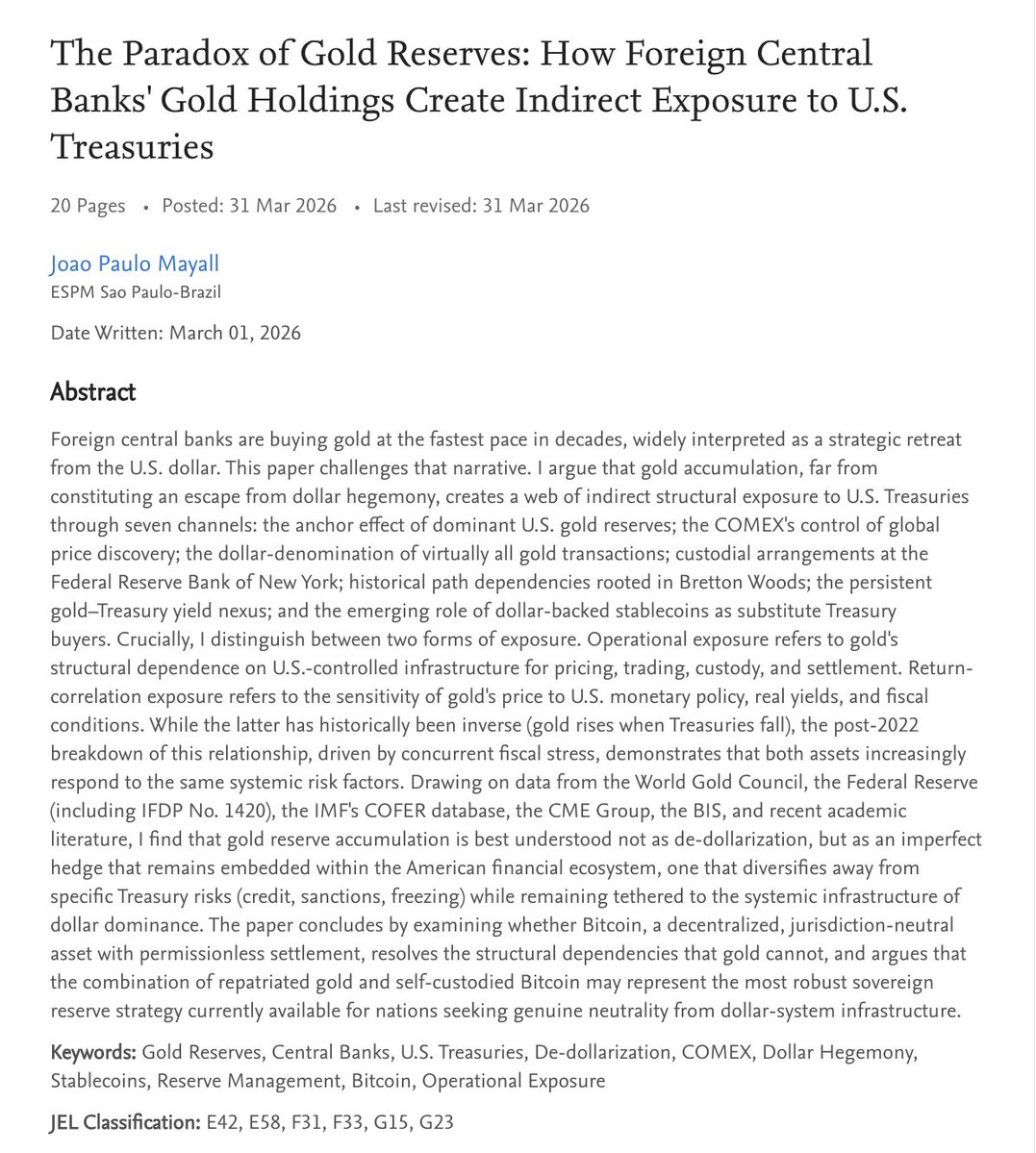

New paper: "The Paradox of Gold Reserves: How Foreign Central Banks' Gold Holdings Create Indirect Exposure to U.S. Treasuries"

Foreign central banks are buying gold at the fastest pace in decades. The consensus view: de-dollarization.

I argue the opposite. Gold accumulation doesn't reduce exposure to the dollar system. It restructures it.

The paper identifies 7 channels of indirect structural exposure to U.S. Treasuries through gold:

1. Anchor effect: U.S. holds 8,133t, 23% of above-ground supply;

2. COMEX price discovery: 74% of global exchange volume;

3. Dollar denomination: >90% of transactions in USD

4. Fed custody: 6,331t at the NY Fed for 36 central banks;

5. Bretton Woods path dependency;

6. Gold–Treasury yield nexus (post-2022 structural break);

7. Stablecoin substitution: $190B+ in Treasuries replacing official sellers.

I distinguish between operational exposure (pricing, trading, custody, settlement) and return-correlation exposure (sensitivity to Fed policy and fiscal conditions).

The paper also examines what gold DOES successfully diversify (counterparty risk, sanctions, freezing) and what it doesn't.

Central banks that sell Treasuries and buy gold haven't exited the dollar system. They've changed their position within it.

20 pages, 30+ sources including Fed IFDP No. 1420.

English

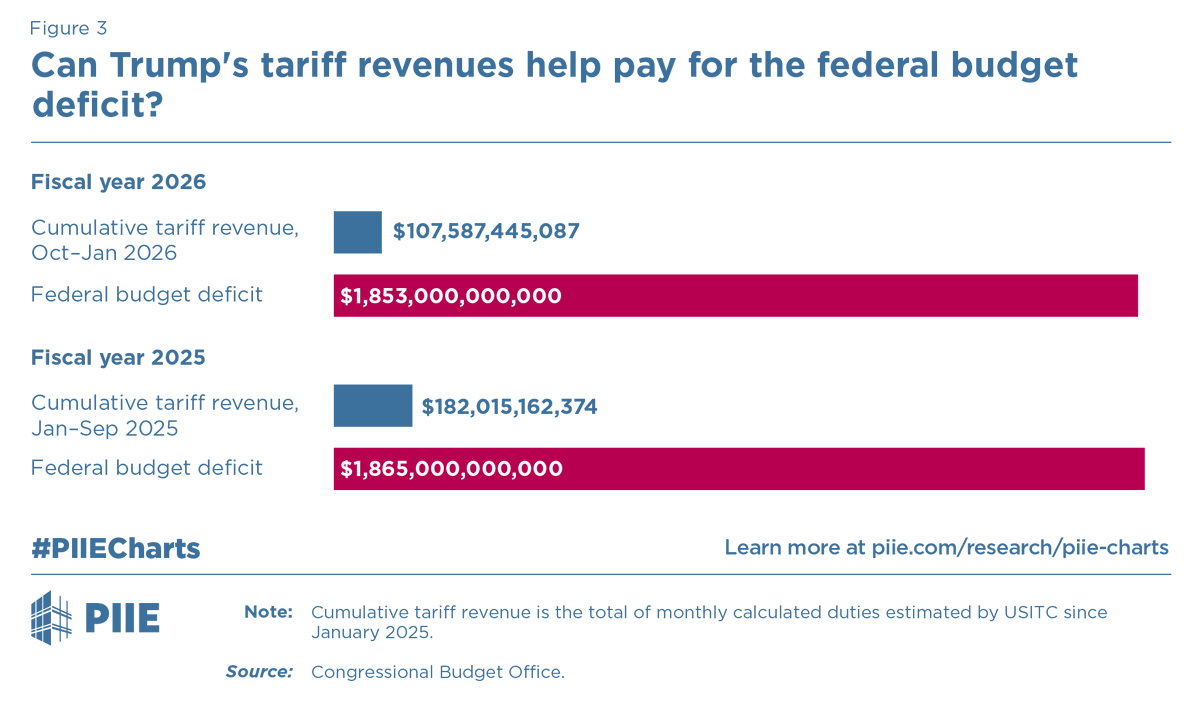

President Trump claims that tariffs can make an outsize fiscal contribution. This claim can be put in perspective by comparing actual tariff revenues with the size of the projected budget deficit 👇

English

@archmi_us @Econ_Parker Damn you guys hired someone from the 300 movie? Badass.

English

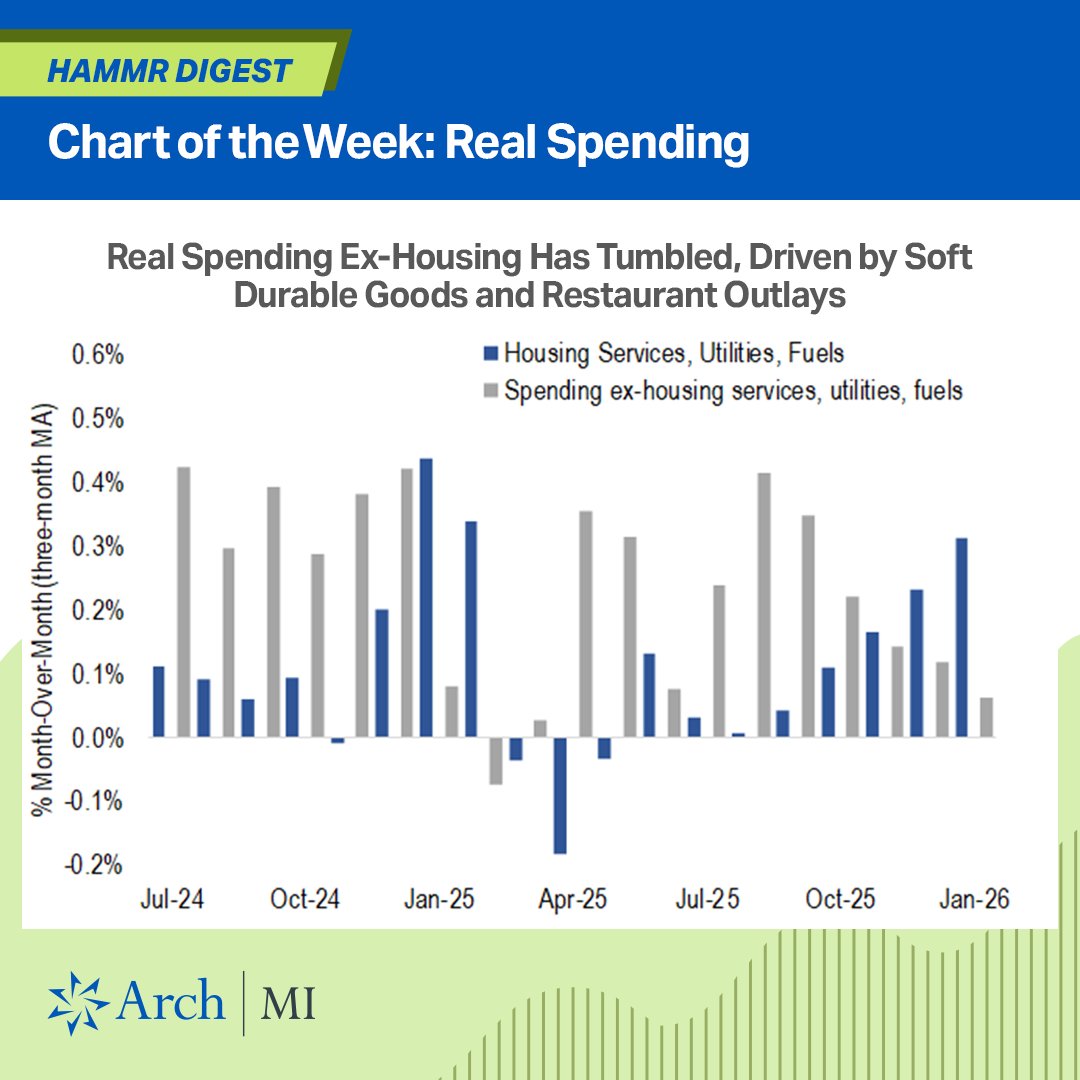

New in HaMMR Digest: Will the rise in energy prices be the final blow to a consumer that was already tightening the discretionary purse strings? Catch up on the data with @Econ_Parker and Leonidas Mourelatos. spr.ly/6017B6rSbt

English

@bryanrbeal this guy is a famous artist named peter draws, not a consumer packaged goods product manager lol. checkout his art he is a beast

English

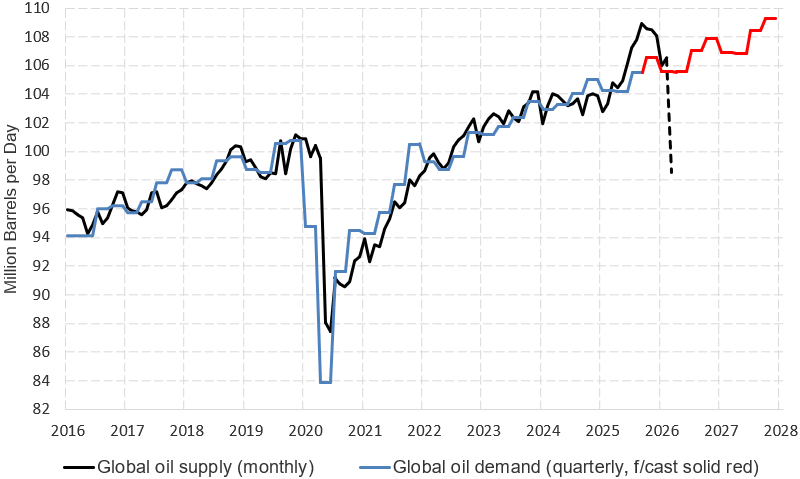

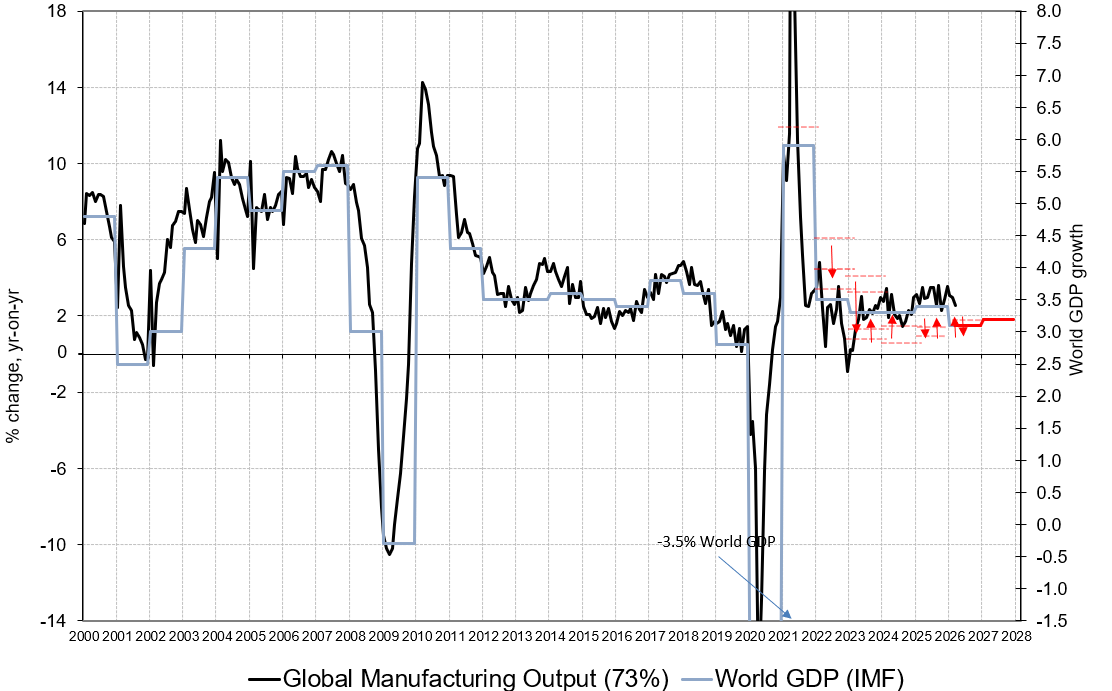

@takis2910 What is the source of this chart? I would very much like to recreate it. Thank you! @takis2910

English