@BankersPrez @WSJ @nytimes @AmerBanker Beautiful tribute - thank you for posting. I loved the chance to get to work with her.

English

Robin Cook 🛡️

278 posts

@robinrcook

US Policy @Coinbase. Former @ABABankers @CUNA @WeilGotshal. Dog dad. Law, politics, banking, crypto. Lots of my own opinions.

ABA's Naomi Camper asks for bankers at ABA wash summit to stand up if they care about stablecoins paying yield. Everybody in the room stands up.

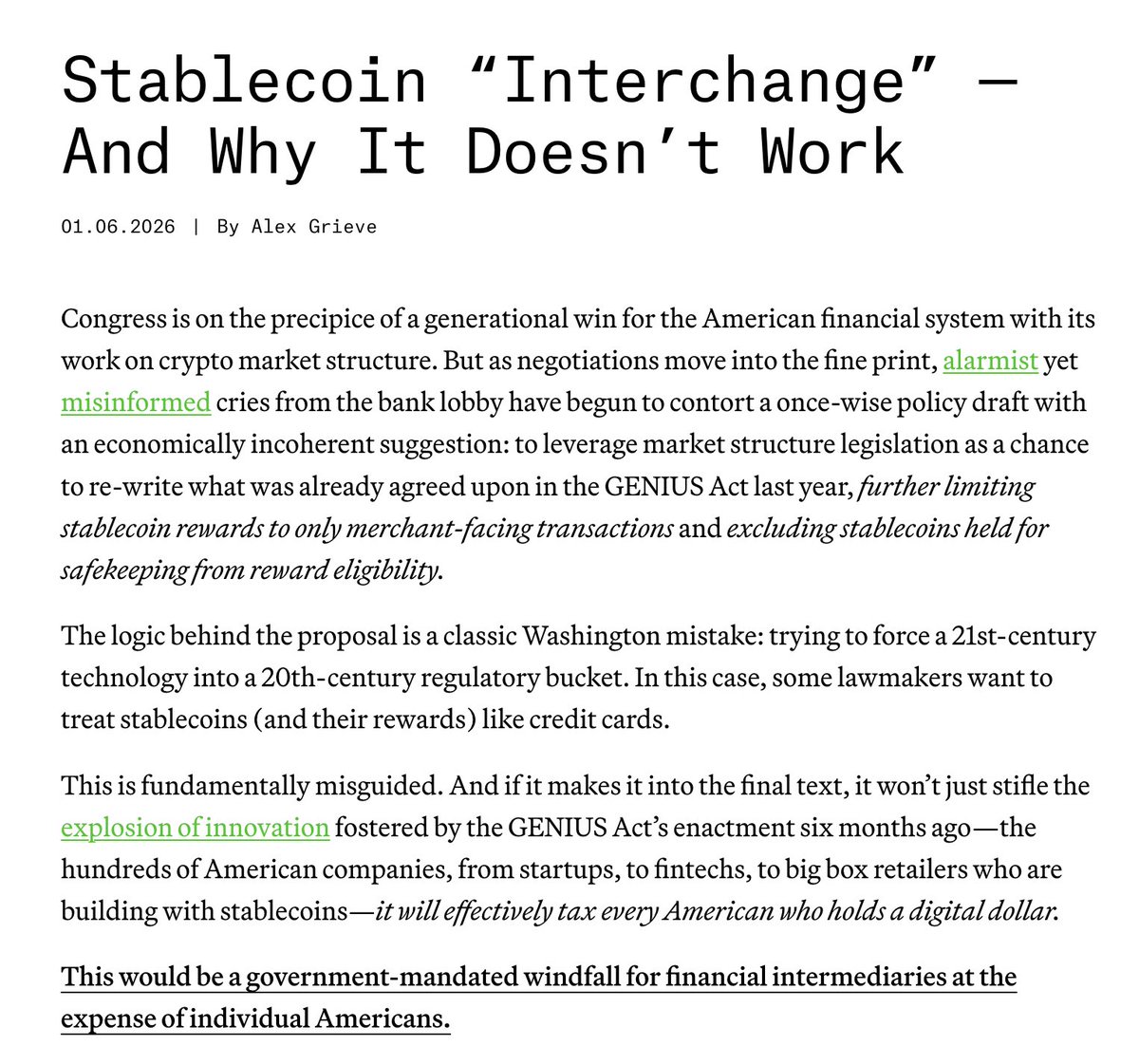

Compromise on CLARITY is compromising local lending and economic production. It's simply impossible to roll over in the fight for liquidity that powers the economies of the places we call home. This isn't hard to understand, folks.

Singing > watching. So we got millions of people watching the Big Game to sing along with us. Oh, and we put it on the world's largest LED screen @SphereVegas.

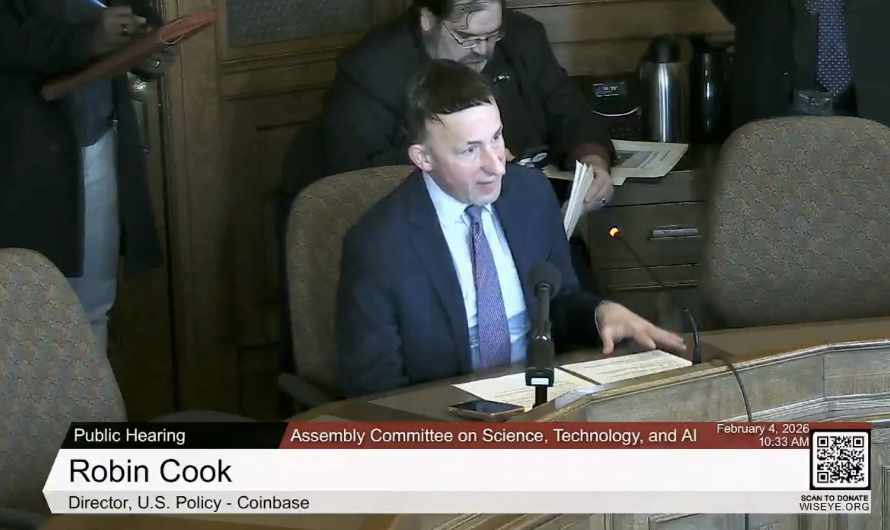

🚨BREAKING: Chairman @JohnBoozman releases updated market structure legislation ahead of January 27th markup. agriculture.senate.gov/newsroom/rep/p…

One of these is not like the others. @standwithcrypto

Banks earn 4.4% on reserves parked at the Fed... They pay you 0.01% on your savings account. And now they're lobbying Congress to make sure stablecoins can't offer you anything better. The GENIUS Act already settled this. Congress spent months hashing out a compromise. Stablecoin issuers can't pay interest directly, but platforms and third parties can offer rewards. Done. Finished. Everyone shook hands. That was a few months ago. Now the banking lobby wants to reopen it. They're calling it a "safety concern." They're worried about "community bank deposits." Independent research shows zero evidence of disproportionate deposit outflows from community banks. Meanwhile, the big banks are sitting on trillions in reserves, collecting interest from the Fed, passing almost none of it to customers. How this plays out for the most part is that your bank takes your deposit, parks it at the Federal Reserve, earns 4%+ on it, gives you basically nothing. A stablecoin platform wants to share some yield with you and suddenly that's a threat to financial stability? We saw three different lobbying pushes on this bill in the last year & every single time, the framing is consumer protection, but in reality, every single time, the actual effect would be protecting big banks and incumbent margins. What you should actually watch for: -Any amendment that bans "rewards" broadly rather than just direct interest payments from issuers. -Whether the same legislators worried about stablecoin yields have ever questioned why bank savings rates haven't moved in fifteen years. -Who's funding the "community bank protection" messaging (Usually not community banks lol) If Congress caves on this, it sets a (not good) pattern. Pass a framework, let the incumbents lobby it back open, chip away until the new entrants can't compete, and crypto companies aren't the only ones watching. Every fintech considering U.S. markets is taking notes on whether legislation here actually sticks. We signed on to this letter to show our support and conviction in moving the industry forward in the United States. The next six months will show whether the U.S. wants competitive payments infrastructure or protected banking margins under the guise of "stability" as always, thanks to @BlockchainAssn for their hard work in the industry alongside @standwithcrypto & @na_blockchain special shoutout to @TBC_Jessi @512mace & @wadepreston for pushing this along as well