Spurious🦋Spelunker@SpuriousSpelunk

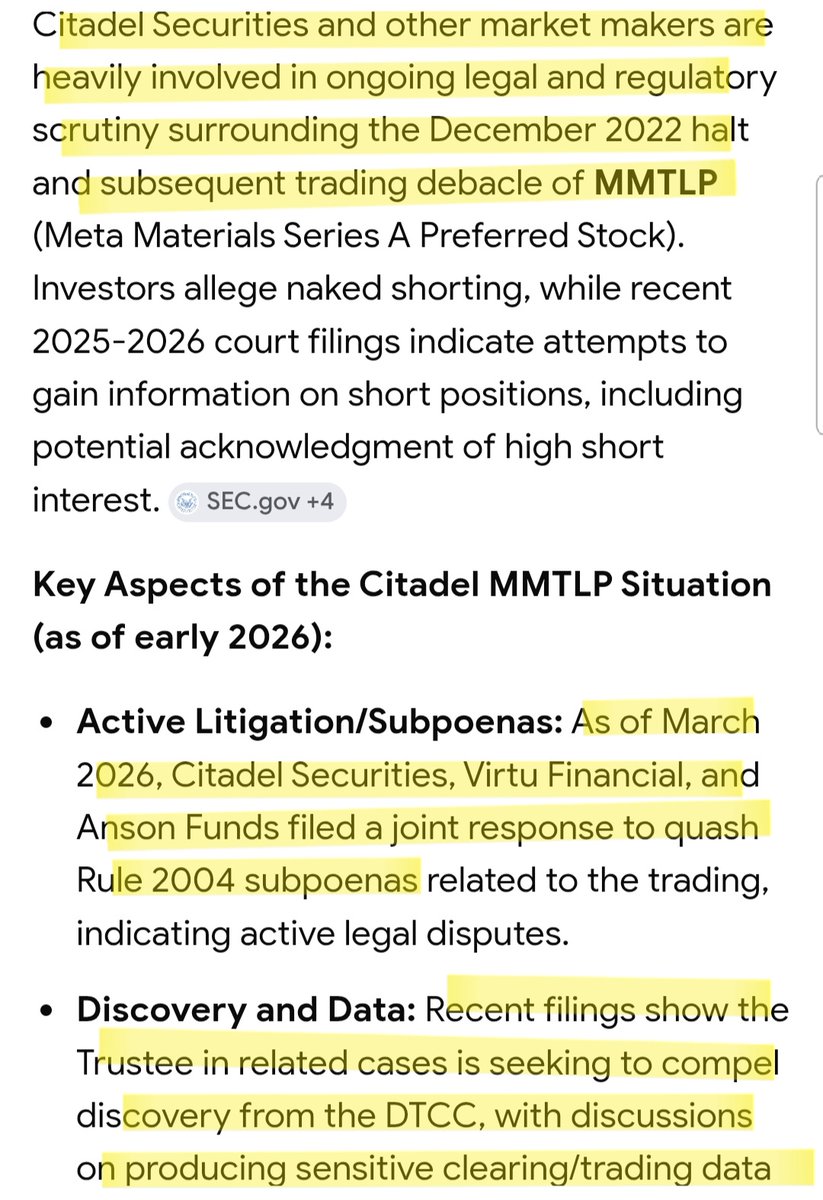

MMAT (also MMTLP/Torchlight-related) Hearing for a Motion to Quash Subpoenas ("Discovery")

02/20/26

I've never written much about MMAT (I never bought any MMTLP when it was available) but I've been talking about them for years, I want others who know nothing about their case to see the significance to us ALL, so here's a preface:

In terms of market manipulation as a topic, and litigation against cases of it, retail investors are ALL on the same side of the issues-

It's not retail who is spoofing orders to influence prices up and down.

It's not retail who is wash-trading nonstop every day all day long via High-Frequency-Trading algorithms, to suppress prices.

It's not retail who is funneling the VAST majority of BUY-orders into Dark Pools, again to keep price from being able to rise in many specific companies' tickers.

It's not retail who is paying for order flow, to match buy and sell orders against each other exactly so as to keep the price profitably where somebody wants it.

It's not retail who literally signs up to be a "market-maker" for special market-maker privileges so that they can functionally naked-short legally (hi hedge funds).

These things plague us all in common, we experience them all throughout US "free and fair" open exchanges. That's why I've said for years that MMTLP investors' pushing at Congress to make the regulators show the blue sheets and FINRA's dastardly breaking of their own rules to side with naked shorting players over lawful longs is something we should ALL be rooting for. When their landmark case is won, it will be a win for everyone who isn't one of the crooks. And it will show a specific pattern of crimes and set precedent so that other cases can follow, because we all know this isn't happening in merely one or ten or even one hundred stock tickers.

When they win, we'll all win. And they're not gonna stop until they win. I know this from listening to their Spaces, you can hear the gritty determination in their voices, it's inspiring. Where we go one, we truly go all.

*****

Hearing notes:

This hearing's date: 02/20/26

Meta Materials, Inc. (Chapter 7)

Case Number: 24-50792

US Bankruptcy Court, District of Nevada

Assigned Judge: Gary Spraker

Repository of (most) docket filings: courtlistener.com/docket/6902957…

I haven't followed this case very very closely, but I've been bearing it in mind peripherally, so to the actual shareholders with stakes in this, if I get something wrong here please let me know. Also trying to write more approachable so everyone not involved gets the main idea quicker.

This was always gonna be an important hearing because it's pivotal, this hearing was about establishing (or not) the more extensive Discovery that one side, the Debtor (MMAT, and the US Trustee speaking on behalf of it), is asking for. They want records handed over from the market-makers (Citadel and Virtu specifically), the Nasdaq stock exchange, and one specific hedge fund (Anson Funds Management LP).

The specific subject in question for this hearing was Bankruptcy Rule 2004, which grants broad Discovery (orders for each party to produce any relevant evidence/info/data requested by other parties). Essentially it allows subpoenas. This case is pretty straightforward in terms of Rule 2004 indeed being applicable and appropriate here. However, the Movants (Citadel, Virtu, Nasdaq, Anson Funds) of this Motion to Quash (disallow) subpoenas of the relevant records (Blue Sheets, order-books, trade execution histories) in MMAT's trading on open exchanges argued against Rule 2004's applicability in the MOST ABSURD WAYS. Look at these arguments that were laboriously made by the market players here:

One of the Movants' lawyers: "The burden is real here for Nasdaq." There's thousands of companies on the Nasdaq exchange. Nasdaq shouldn't be subjected to producing unlimited trading records every time a listed company enters bankruptcy.

Judge Spraker: "That's not what we're establishing here." ... 'If I deny [the subpoenas as Movants wish] then a publicly traded company that is facing bankruptcy will never be able to get any trading records.'

Movants' lawyer: We already produced 6 months of trading records for the other side (the Debtor, MMAT). We're not saying we refuse to produce records "if concensual..."

Judge: So another 6 months would be ok.

Movants' lawyer: "We would prefer not to even have another 6 months" but the more data the Trustee asks for, the higher the "burden" for Nasdaq, and the need for such information goes down.

Translation: Waaaaah please don't make us produce more data, it's too haaaaard and nobody needs it!

Judge: Remind me again what records were actually requested by the Debtor.

Movants' lawyer: 3.5 years of additional production (records). But that won't show participant ID's, the Trustee and Debtor won't be able to tell who's doing the trading from Nasdaq's data...

Translation: Please don't ask for more long-term evidence...

Citadel's lawyer: The prices of the stock trades in question wouldn't be affected by such a potential short-term manipulation as "spoofing."

Non-alternative Fact: The stock price would ABSOLUTELY, OF COURSE be affected by spoofing. ESPECIALLY in the short-term, but also cumulatively in the long-term.

Citadel's lawyer: The debtor already went to a third-party company, "Share Intel," spent money on them and got info about trades from them, that should be enough to illuminate the situation!

What he wouldn't say out loud: the data that that company provides is all based on PUBLICly available trading data which is extremely limited, so OBVIOUSLY that's not enough information to determine definitively whether foul play affected the stock price.

Citadel's lawyer: "Our client is a market-maker. We trade securities all day, every day. If a Rule 2004 subpoena can properly issue, in a public company bankruptcy, based on the idea the stock was theoretically manipulated, we could be subject to Rule 2004 Discovery in every single case! And it's not just Citadel Securities, every broker-dealer, every exchange... would be subject to the new rule that the Trustee is articulating."

My opinion: YEAH, and they SHOULD! That's the entire point. In situations where there are preliminary signs of concerted interference with stock trading, subpoenas SHOULD be permitted to request relevant trading data from the exchanges and market-makers who are executing the exact trades themselves!

Citadel's Lawyer: "Your Honor, one of the questions remaining unanswered is 'Why us?' Why is the Trustee seeking info from Citadel, from Virtu, from Anson Funds? And that's a question that remains unanswered. The reason we believe it's unanswered is because the Trustee doesn't want to name a litigation target... Once a Trustee identifies a litigation target, Rule 2004 is inappropriate."

My reaction: LOL

Translation: 'Boohoo Your Honor, they're picking on us! They won't formally declare us a litigation target, on purpose!'

The reason why: Of COURSE they won't name them a formal target yet, this is a very preliminary stage and the Trustee doesn't have anywhere near the whole of relevant data to determine who the case should be made against, nor even whether that specific case should be sought to be made at all. Obviously relevant data is needed before anything more specific can be seen/decided.

[IMO the best, simple, straightforward point made in the hearing, it makes you look at Nasdaq and think hmmmmmmm:]

Debtor's lawyer: We initially requested 6 months of data. Our experts began to review the data and it looked fine at first, but then "Nasdaq hired outside counsel, and they put the brakes on and refused to work with us any further. And as you know they then filed a motion to Quash..." ... 'Nasdaq's arguments about burden, relevance, over-breadth, need to be taken with a heavy grain of salt... Nasdaq already produced 6 months of data... they've shown they are able to produce the data. All we're talking about is spreadsheets. We're not asking for emails, letters, powerpoints... just spreadsheets of trades. The same spreadsheets they've produced for 6 months, we just want them to expand to the total 4 years and include the "Order Type" field... The burden of producing 4 years should be identical to 6 months... We got the initial production in 30 minutes after requesting. All they have to do is plugin the criteria and generate a larger spreadsheet... We're confused by Nasdaq's reluctance to give the additional spreadsheets... They haven't defined what their "burden" is, not in terms of hours nor cost, they just throw out the boilerplate "burden," which any party objecting to any Discovery can say. But it can't be that any Discovery is burdensome because then there wouldn't be any Discovery in any case... If not now then when? If not in this case, then would any succeed?'

About halfway through the 3-hour hearing, Wes Christian Appeared. If you don't know who he is, he's fantastic, he has decades of experiences leading cases against naked shorting, spoofing, and other specific market manipulations. He spoke back and forth for some time with the Judge, representing the debtor.

Wes Christian: The arguments the Movants are making against Discovery are premature. We're not making the full case yet, we just need data to do research for our analysts to know more... Movants are talking as though they are Accused. There is reason to believe counterfeit shares have been sold, but we don't know who the parties are that did that. We need more information to be able to plead with specificity.

...

Wes Christian: We'll eliminate the request for emails for now to reduce the burden. Just give us the Consolidated Audit Trail data which they ALREADY actively give to the market regulators on an ongoing basis.

Judge: If there is an inkling of possible market manipulation, why wouldn't this be a situation for Rule 2004?

Anson Funds' lawyer: Because we haven't heard the Trustee said that they believe that our clients engaged in Market Manipulation.

Judge: "No, because you engaged in the market! It may have been you, or the entity next to you, but you engaged in the market. To understand the totality of the situation, they need to know about the trades."

Anson Funds' lawyer: There is no basis that our client has engaged in market manipulation.

Judge: We're way before that, that's the whole point!

...

Anson Funds' lawyer: Unless their argument is that [this is a bad short-selling issue]-

Judge: "We're not there yet. We're not at the end of the race." We're not at the point of specific accusations. "That's the problem."

Debtor's lawyer: All we're asking for is the production of that 4-year period. It shouldn't be any more burdensome to produce the longer period because "all we're talking about is a spreadsheet that's bigger or smaller than another spreadsheet."

Judge: My assumption is that it's really just a wider computer search?

Debtor's lawyer: Correct... that should just require some employee to plugin those criteria and generate a spreadsheet, and send it to us... it would be market-wide data sought on behalf of the Trustee for counsel to do analysis.

Result of hearing: By the end, the MMAT Estate asked to produce a mere 161-day additional period of data to review for specific indications of manipulation. Judge Spraker agreed and allowed responses from parties for the arguments made on both sides within a 10-day turnaround. He mentioned that-

Judge: "August 9th, 2026 is the Statute of Limitations, so this will be done in plenty of time one way or another... If Rule 2004 is to be granted, then it needs to be done in time to serve its purpose." The more we continue to argue, the more it's shortening that "fuse." If the parties can come to agreement amongst themselves, great. "I'm assuming they cannot. But I need the appropriate information to make the right decision."

My last 2 cents: This was an objectively beneficial hearing in terms of advancing toward the most important facts, evidence, and truth. It was good for MMAT the Estate, it was good for MMTLP-holders whose situation will benefit from more price-manipulation being unearthed and proven in their predecessor's stock, and it was good for retail investors in general that the Nasdaq, multiple market-makers, and FINRA be forced to have more ACCOUNTABILITY. If it takes a bankruptcy court to wring the relevant facts out of them and THEN it just so happens that it's seen that they were manipulating stock nefariously and/or turning a blind eye to it, so much the better for the historical record, for all damaged companies' cases, and all household investors in general.