Liberty Mutual is forcing me and my cat back to an asbestos contaminated apartment, despite having ample policy coverage. The violations are nakedly obvious and the contradictions are too many to count. They make no effort to feign compliance or conceal egregious bad faith.

The practice of "Delay, Deny, Defend," in all its permutations is an impenetrable stonewall that no consumer can overcome. It is not only deeply unethical, it is profoundly immoral. The constellation of this strategy is the definition of bad faith. It is time to codify into law that our society will no longer tolerate systematic cruelty toward consumers, especially when they are in crisis.

If the individual statutes comprising bad faith practice were a sufficient deterrent, then the abuse would stop. Big Insurance acts as if they have absolute impunity. Because they do. There are no commensurate consequences. They ruin lives and pay a thousand-dollar fine. When a consumer commits insurance fraud, they go to prison. When an adjuster does it, nothing. This legal double standard must end now.

Regulatory fines for violations are a cost of doing business like overhead. That is not a deterrent. It is a cost-efficient invitation to engage in financial violence against consumers. Without real consequences, there will be no real compliance.

Have you noticed that the only time an insurer will change their position, is not when compelled by a regulator, but rather when embarrassed by public ridicule. When shining a light on the cockroach is more effective than the spray, it is safe to conclude that established regulations are impotent.

The existing statutory regime has failed the public and caused immeasurable hardships. These statutes need to be changed from civil to criminal. Adjusters who knowingly engage in fraud, retaliation, misrepresentation, and other deplorable behaviors, known as "unfair claims settlement practices," must be held criminally accountable, at every level of the enterprise.

VIGNETTE:

I have lived in the same apartment for almost 20 years. For almost as long, I did the responsible thing by maintaining a renter's insurance policy in case the unforeseen were to happen. It happened!

In the middle of the night on February 9th, I was woken up and evacuated by the fire department due to multiple gas leaks and high levels of carbon monoxide. It's a miracle the building did not explode.

A condemnation notice was affixed to the house on Feb. 9 and remained there until March 12.

After satisfying my deductible, I requested that Liberty Mutual start covering the hotel. That was the beginning of the horrors.

That First Denial:

While getting checked for CO poisoning, I got Covid. Several days later, I became extremely sick. I went back to the ER on Feb 16th. This time they admitted me for an acute kidney injury and put me on an IV.

Early on Feb 17th, I received my first denial letter and a phone call from the housing vendor (who paid for the past three days at the hotel). The vendor notified me that the hotel was being terminated.

I told the rep that I'm in the hospital on an IV while my cat and my belongings are at the hotel. I asked her, what do you want me to do? The housing vendor extended the hotel for two additional days, not Liberty Mutual. They were fully content to throw my cat and my evacuated belongings onto the street while I was hospitalized.

Feb 18th, was my first day back from the hospital. Despite severe exhaustion, instead of resting and recuperating, I had to immediately begin writing letters to prevent the imminent termination of the hotel on the 20th. I spent hours upon hours writing, editing, and curating arguments.

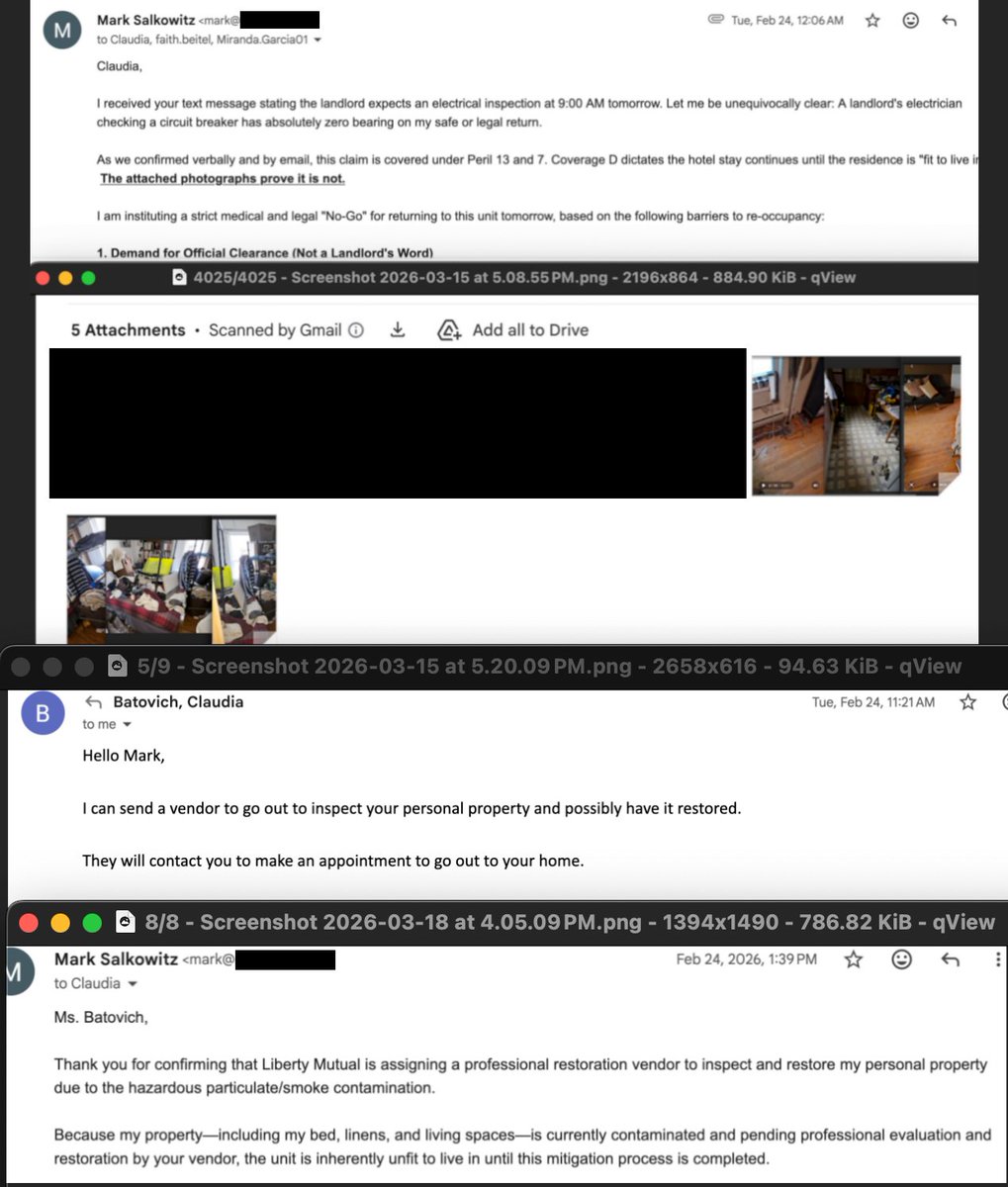

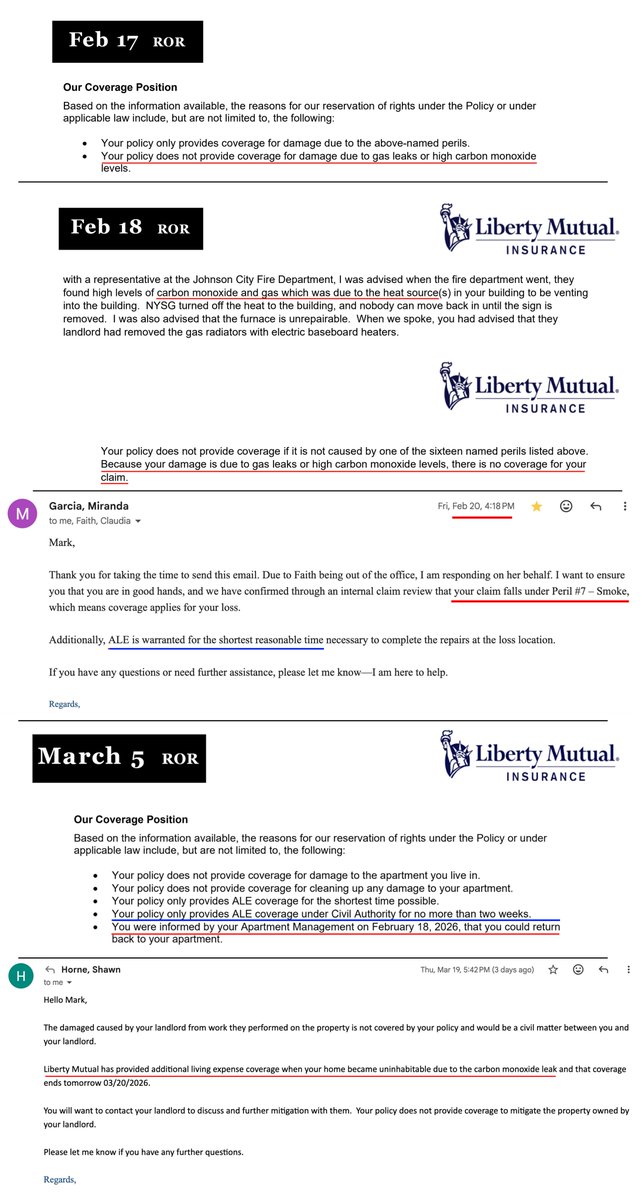

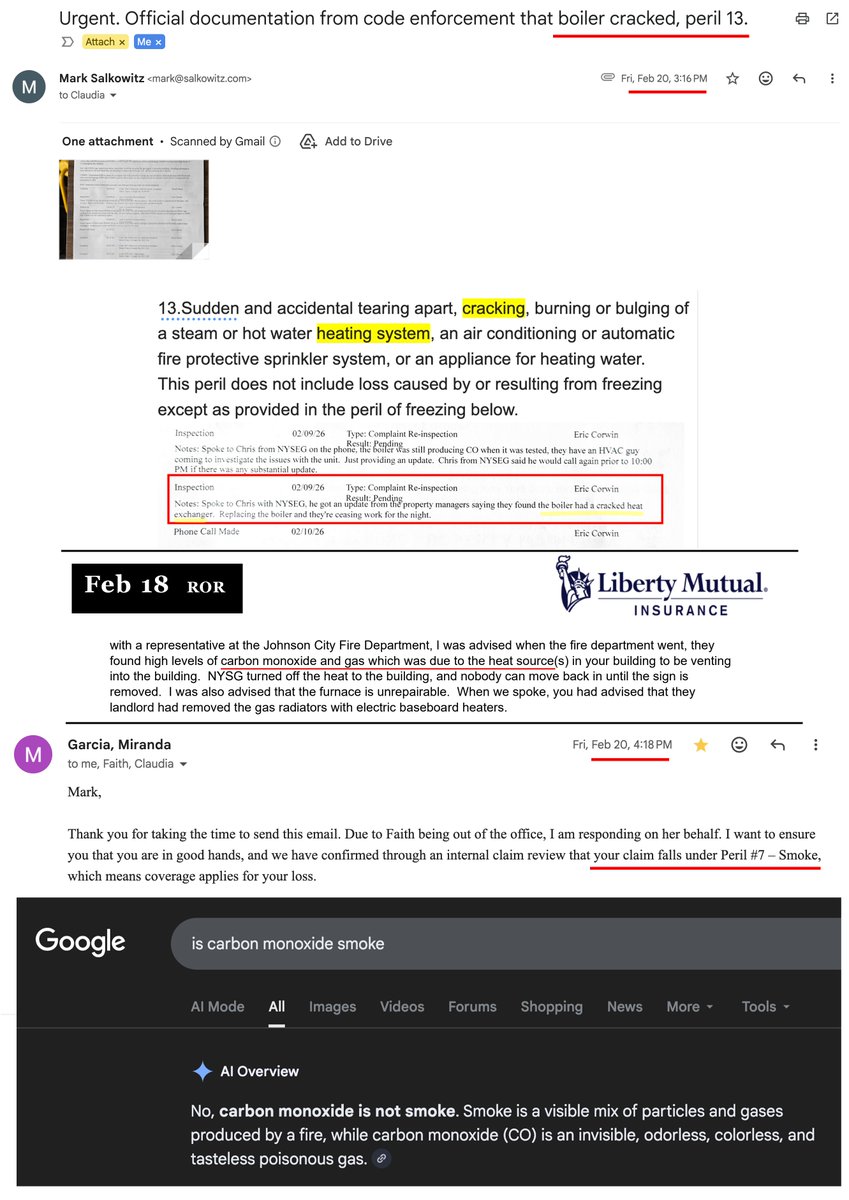

On February 20th, I finally had documented proof to satisfy Peril 13 (broken heater). Only after proving Peril 13, did they decide to cover my claim under Peril 7 (smoke). However, there was never any smoke...

The 72 Hour Cycle

The 72 hour cycle was identified as the most effective way of creating the highest amount of stress for claimants. The entire apparatus is designed to cause the maximum psychological attrition. The weaponizing of housing is quite literally cruelty and anxiety by design.

My time was not my own. I missed follow up appointments and could not schedule follow up tests because I did not know my status for the next three days. And all three days were spent writing arguments for the next three days.

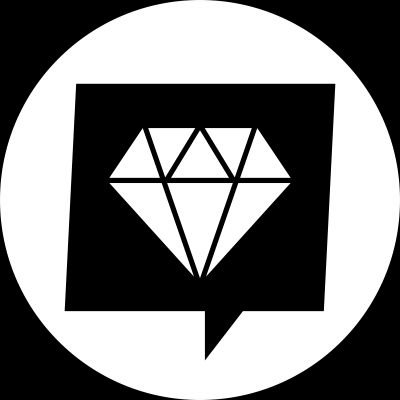

Between February 20th and March 5th, there were multiple attempts to end coverage. I was told that the condemnation notice was removed when it was not, but the hotel was terminated anyway. I was told that I received a notice when I did not, but the hotel was terminated anyway. I was told a vendor would inspect my apartment for damage; but they never did.

Shifting Coverage Positions (Shell Game)

First they said there was no coverage for carbon monoxide. Then they said that I received coverage for carbon monoxide. Their own denials (RORs) admit to peril 13, yet they refuse to honor the correct peril. First Additional Living Expenses (ALE) did not apply. Then it applied for the "shortest time." Then it applied for two weeks. Then it became completely arbitrary.

These contradictions arise when an insurer operates without a consistent, sound basis for coverage. If my claim were being handled properly and normally, the rationale wouldn't completely reverse into a 180-degree contradiction after 30 days.

Asbestos

According to public records, the house was built in the 1920s. In the 1920s asbestos was used for pipe insulation. Within a few hours two of the landlord's handymen sawed through and ripped out all the radiators from five units. My apartment had four of them.

On March 18th, I received a call from the vendor. When I asked if he was certified for asbestos, he said he needed to call the adjuster.

The adjuster promptly withdrew the vendor. He stated that the vendor could not perform the kind of cleaning I was requesting. I called the vendor back and asked if he was able and certified for asbestos. He told me that he was fully certified, but the adjuster told him that my renters policy didn't cover it.

Malice:

The adjuster said that when there is a potential for a toxic environment, it needs to be tested by an environmental hygienist. The very next day, he said the code inspector (who checks electrical and fire codes) determined the apartment was safe. The next day he cited the landlord as verifying the apartment was safe. And the next day all coverage ended.

My apartment remains very-likely contaminated with asbestos. I have a $30,000 policy for property damage and a well documented covered claim. Yet Liberty Mutual will not even release funds so I can replace contaminated linens, bedding, or wash contaminated clothes, nothing. They will not provide the required ROR explaining why.

They stopped paying for the hotel on Friday. I have been paying for it since then. On Tuesday I will no longer be able to maintain the hotel and will be forced to return to an asbestos-contaminated apartment or seek public assistance, despite being fully covered for such events.

@SenGillibrand and @SenSchumer even though you accept donations from Liberty Mutual, please show the public that they did not purchase favor.

@NYDFS @TishJames @AOC @SenWarren @BernieSanders @SenatorSlotkin @RepMaxineWaters @HawleyMO @ProjectLincoln @MeidasTouch

#DelayDenyDefend #BadFaithInsurance #InsuranceReform #ConsumerRights

English