Mathgrün

249 posts

Mathgrün

@mathgrun

Aktien - Mandelbrot ist mein liebstes Brot.

Sumali Haziran 2019

1.3K Sinusundan69 Mga Tagasunod

English

@nitininvests @schinskytrades They are also getting a bunch of that cash back from the warrants fwiw. Like $2m if I remember correctly. Glad this overhang is gone

English

Took some profits here. Again, my position is entirely in options, and if the recapitalization happens, the NAV will reduce. I will hold the remaining 10% position and sell right before earnings. If my calculation is accurate, the NAV should increase around $1.40–$1.80 driven by Schylling. If the recap happens, the NAV gets reduced. The ideal scenario would be for the stock to sell off on earnings and then rebuy if the recap actually happens but a sale doesn’t. If $GAIN announces a potential sale of Schylling, the stock could continue to go higher (scenario we covered in the deep dive), but I will be more than comfortable missing out if that actually happens.

Nitin Gupta@nitininvests

$GAIN sold a decent chunk of my options for 65-75% gains. As I said, the options were severely mispriced. Ultimately, I want to be prudent with profits given that if I am right and the recapitalization actually happens, the NAV might drop drastically, which might present another opportunity to enter later. Congrats to anyone else who was riding this with us.

English

@evfcfaddict eqs-news.com/de/news/direct…

The CEO and founder shows his opinion regarding the sell-off

English

@absreturnchaser Why did you delete your last post regarding $EVD.DE?

English

@nitininvests @cynicitycottier The situation surrounding Mike Zoi is also interesting for another reason: so far, his Class B shares have prevented a 20% dilution (warrants issued in July 2024 with pending approval). If he loses his controlling stake, the dilution will likely Happen (950,000 shares at $2.17)

English

That’s a genuine question. From what I have read about Driven, it appears that this is a very small position for them and they are only selling the Class A shares. There is no mention of $MSGM on their website either. Even if they sell their entire Class A shares, they will still retain majority voting rights for the company through their Class B shareholding, which implies they probably still see upside in the business. I also think their capital allocation with this specific venture has been pretty poor, given that they went long near $20, bought at the wrong time, and perhaps are selling at the wrong time too. Additionally, there could be myriad reasons for selling, but I think the valuation and the catalysts ahead present a classic heads I win, tails I don’t lose much scenario at this point, which I get extremely excited about given the market backdrop.

English

@dogwatercap Maybe also the credite line and the implications for the use of the cash: development of new games with unclear ROIC. And on the surface $MSMG just looks like another gaming shit co.

I am invested and i think we are at just at the very beginning of the discovery process.

English

Anyone here bearish on $MSGM?

I’d like the negative thinking here cause I can’t figure out why it pulled back under $4 after such a strong print.

Best I got is no financing partner announced yet for console, but feels weak. Doesn’t seem like it’s Zoi.

Could just be a gift.

English

@hidden_returns So einfach kann es sein. Ich würde eine Besprechung 2 Jahre später sehr interessant finden!

Deutsch

1/3 Mit Seneca Foods $SENEA haben wir uns dieses Mal den möglichen Profiteur in einem schrumpfenden Geschäftsfeld angeschaut, das langweiliger nicht sein könnte: Gemüsekonserven. Der Case ist dafür längst nicht so langweilig.

Darüber hinaus...

hiddenreturns.eu/episode/7-sene…

Deutsch

@nitininvests The new credit line does have favorable terms, but it should not be necessary given the expected cash flow +funding partner. The fact that the credit line was agreed upon nonetheless makes me skeptical.

English

@nitininvests Is the sell-off based on uncertainty regarding future capital allocation? I am invested, but my biggest fear is empire building instead of good capital allocation.

English

$MSGM has no real reason for the sell-off other than the overhang of almost ~28% of the total o/s shares held by Mike Zoi imo, as I mentioned in the article. In March he has accounted for 11% to 31% of the daily selling volume. So there is a good chance that at least 20% of the total 1.5M shares traded yesterday and today were sales by him, meaning roughly 50% of the shares he intends to sell have already been sold. I believe once this downward pressure ends, the stock should rerate.

Nitin Gupta@nitininvests

$MSGM delivered a brilliant quarter across all metrics imo. The valuation disconnect is baffling. The company has roughly 5.1 million shares o/s and a market cap of around $23 million. With a $6 million cash position (as of February 2026), the enterprise value is just $17 million. EBITDA for the year was $7.3 million, putting the stock at 2.4x EV/EBITDA. They carry zero debt, maintains a clean balance sheet, and generated consistent positive operating cash flow (~$300K/month in 2025). Deferred revenue grew sequentially from $1.11 million to $1.13 million. Since the v1.2 DLC was fully delivered in Q4, that revenue should have been recognized in Q4, implying the remaining balance is almost entirely driven by RaceControl subscriptions. Management confirmed ~26,000 subscribers generating $200,000 in monthly recurring revenue (MRR) at year-end implying an ARPU of ~$7.50/month, heavily suggesting widespread adoption of the sticky $84 annual package. Management also noted that January and February 2026 saw the largest subscription revenue jumps yet. The company appears on track to hit a $3 million ARR run rate for RaceControl sooner than I expected, potentially as early as March. I was expecting to happen in June driven by the Le Mans 24 hour race. This segment along with the licensing segment has over 90%+ margins and significantly enhances the profitability profile. Q1 is shaping up to be even stronger, with a $1M+ per quarter high-margin baseline from RaceControl and licensing, plus immediate top-line contribution from the new DLC pack launched on March 23rd. The core business is scaling rapidly, yet the stock is priced as if bankruptcy is imminent. The ongoing selling overhang from Mike Zoi remains the primary artificial drag on the share price imo. Once that clears, the strong fundamentals should drive a dramatic rerating. I don’t see another reason for the current valuation. The presence of the Sidoti analyst on today’s call (first time in a long while) suggests institutional interest is building, and we may see coverage initiations soon. The turnaround appears complete and hopefully aggressive growth should follow from here.

English

@TheAppInvestor @AdmiralRisky @ReneSellmann @CCM_Brett First success for the activist: The CEO is stepping back and the incentives are getting way better. But it seems, nobody cares (except me). Friday market reaction for $GRVY : -0,5%

nikkei.com/article/DGXZQO…

English

@AdmiralRisky @ReneSellmann @CCM_Brett Where did you get that GungHo, who themselves have been doing dividends (sporadically), have asked Gravity not to?

There's also an activist investor shaking the tree in GungHo, which may change their attitude towards shareholder together. At least they're trying.

English

Gravity $GRVY is a textbook example of changes in market structure.

English

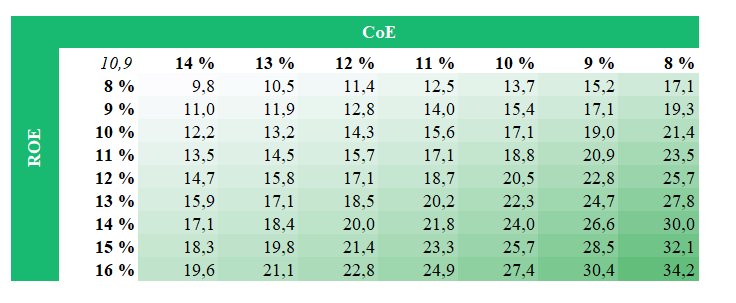

@BuffDawgg I think for the most people the biggest risk are low quality Credits in the books, so no rerate today.

English

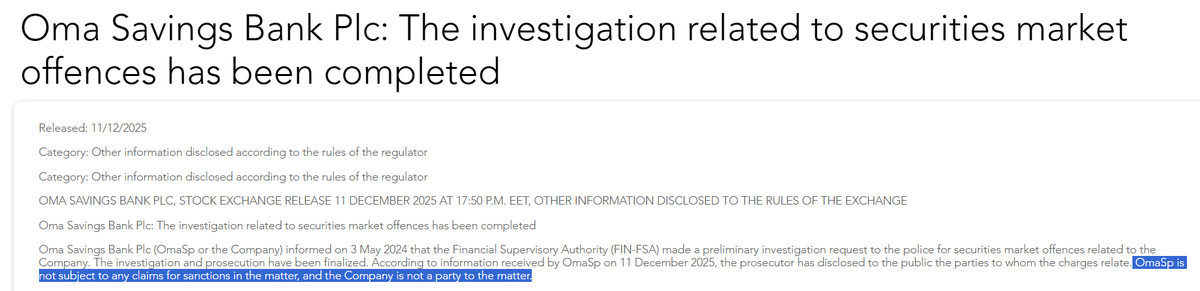

Finnish prosecutors have closed the securities-offence case tied to $OMASP, confirming the bank isn’t a party and faces no sanctions. Now that the major legal overhang is gone, could it rerate at open tomorrow? Still at ~0.6x TBV, so let's see.

English

@TurboToni4 LOL. It's actually trading at 0.6 currently. So not just one guy that wanted to get in.

English

$IMB.AX very significant and transformative acquisition

- NZ 89.5 million revenue and NZ 10.9 million EBITDA before synergies.

- Acquired at four times EBITDA.

- Fully funded through debt and cash flow.

- Strong recurring revenue base

cdn-api.markitdigital.com/apiman-gateway…

English

@finance_schmidt Stabiler Konsum, wenn das beim letzten Quartalsupdate noch nicht so war 😃

Deutsch

While updating my trades in Portfolio Performance, I noticed something that really surprised me. This year I crossed a milestone: I have now withdrawn more money from my portfolios than I ever put in. My total net investment is now minus 75k EUR.

English

Aus dem Schnitt dürfen wir euch mitteilen: Am Sonntag kommt die längste Folge der Podcast-Geschichte und sie ist voll gepackt mit Updates über $LEAT $IRIX $IMB.AX und $NOW.V.

Deutsch

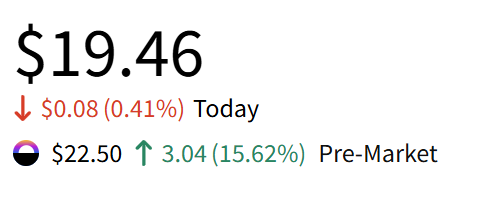

@romanp000 Little Insider trade from the CEO. 9000 shares for 12,8 Nok. Makes me a little bit less sceptical

English

$MPCES MPC Energy Solutions signs an agreement to sell 2 of their projects (equity) for $27m. They also have around $9m in cash and 2 additional projects that might get sold too. The Marketcap is around $21m. They intend to distribute most of the cash to shareholders 1/2

English

@CloneShameless Ich hoffe für dich, dass du dich dran gehalten hast :D

Deutsch

$JAKK

the quarterly JAKKs roundtrip. Traders heaven, buy under 20$, sell over 25/30$ :D

English