@jackprandelli I was interested until you referred to 2022 as a “major market crash” 😂😂

English

NFW

86 posts

Athene sells Fixed Indexed Annuities. The pitch to retirees: "You get some of the S&P 500's upside with none of the downside." To deliver that promise, Athene buys call options on the S&P 500 from investment banks. Market goes up, the option pays, Athene pays the retiree. The retiree thinks she owns a savings product. She owns the other side of a derivatives trade. The numbers: $8.1 billion in fair value derivative assets against $4.1 billion in capital. The derivative book alone is 2x the capital base. 78% is S&P 500 call options. 1-2 year maturities. The annuity liabilities they hedge last decades. Every year the hedges must roll — at whatever the market is charging. In a vol spike, option costs can triple. The cost of keeping the promise can exceed the profit earned on the entire investment portfolio. Two French banks — Societe Generale ($2.04B) and BNP Paribas ($1.69B) — hold $3.7B in fair value derivative exposure. Nearly the entire $4.1B capital surplus is concentrated in two counterparties. Citibank's potential exposure alone is $590 million — 15% of total capital from one name. $655 million in cash collateral posted. Hundreds of millions more in corporate bonds pledged as initial margin. In a liquidity crunch, that collateral is trapped. The NAIC's own "Potential Exposure" metric — what Athene could lose if counterparties default — is $2.1 billion. Half the capital. Estimated total notional: $120-160 billion against $4.1 billion in capital. 30-40x the capital in derivative exposure alone, stacked on top of 69:1 leverage on the invested asset portfolio. This extends beyond Athene. The dealers who sold these calls — SocGen, BNP, Barclays, BofA — delta-hedge by holding S&P 500 stocks and futures. If the economics of rolling break in a vol spike, the dealers unwind those hedges. That is a sell program the equity market does not see coming because it is embedded in the options market. Athene is one insurer. The entire FIA industry runs the same playbook through the same 8-10 dealers. The collateral is pro-cyclical — market stress reduces collateral values, triggers margin calls, forces liquidation, reinforces the decline. The derivative book is not a hedge that makes the company safer. It is a transmission mechanism connecting the S&P 500 options market, the European banking system, and American retirement savings into a single point of failure. Max pain is a simultaneous equity sell-off and vol spike — Q4 2008 conditions. Equities drop, so the call options Athene holds lose value. Vol spikes, so the cost of rolling triples. Credit widens at the same time, impairing the bond and mortgage portfolio. Collateral values fall, triggering margin calls from the same French banks. Margin calls force liquidation of illiquid private credit at distressed prices. Realized losses erode capital. Rating agencies downgrade leading to more capital calls. Headlines hit. Policyholders surrender. Surrenders require cash. More liquidation. More losses. Dealers unwind delta hedges. More equity selling. More vol. The loop feeds itself. The closest analog is AIG. AIG sold credit protection to banks. Athene buys equity protection from banks. The direction is reversed but the mechanic is the same — a massive concentrated derivative position with a handful of counterparties, on a balance sheet with insufficient capital to absorb a tail event, wrapped in an insurance company that the public trusts because the word "insurance" is in the name. AIG needed $182 billion from the Fed. Athene's balance sheet is comparable in size. This structure has never been stress-tested by a real crisis. It did not exist in 2008. This reads to me as lot like Leland O'Brien Rubinstein. Page 9,599 has the verification table. Pages 6,401 through 9,598 have every individual position. The filing is public. I am inviting every derivative structurer, risk manager, and counterparty credit analyst to open Schedule DB and tell me what I am missing. @jam_croissant The filing: athene.com investor relations, AAIA Q4 2025 Annual Statement.

See the relationship between: - Round size - Valuation - Dilution Does that help?

Citadel CEO Ken Griffin on why the AI boom might be the most overhyped tech cycle we have ever seen: This year alone, data center spending in the United States is projected to exceed $500 billion. And Griffin wants to know what all of that money is actually buying. "You're not going to generate this kind of spend unless you're going to make a promise. You're going to profoundly change the world." In his view, the scale of the capital commitment demands the scale of the promise. And when the promise has to be that big, hype becomes inevitable. "Is it hype? Of course." Griffin isn't arguing that AI is worthless. He sees real impact in certain areas like call centers and software engineering. But for the broader white collar workforce, he's far less convinced. He points to a recent Harvard paper that coined the term "AI work slop." It looks impressive on the surface, but falls apart the moment you look closer. He saw it firsthand inside Citadel. A colleague running their commodities business handed him a report generated by an AI engine. "The first few sentences like, 'Wow, that's really insightful.' And then you go down below that and it's all garbage." For Griffin, this is the defining tension of the current AI cycle. The industry needs to promise transformation to justify the investment. But the actual productivity gains, for most jobs, haven't shown up yet. We have seen this pattern before. Transformative technology attracting massive capital well ahead of proven results. When the hype finally settles, will AI have actually changed anything at all?

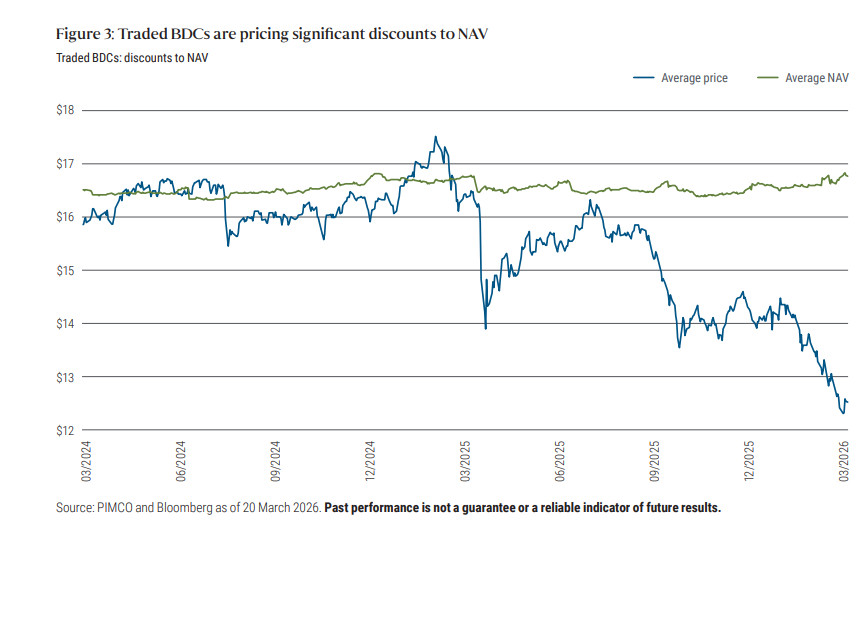

"Unprecedented" Withdrawal Requests Now Hitting Private Credit zerohedge.com/markets/unprec…

I am reaching out to the @X community for advice with the likely risk of sharing TMI. I have been sufficiently upset about the whole matter that I have lost sleep thinking about it and I am hoping that this post will enable me to get this matter off my chest. By way of background, I started a family office called TABLE about 15 years ago and hired a friend who had previously managed a family office, and years earlier, had been my personal accountant. She is someone that I trusted implicitly and consider to be a good person. The office started small, but over the last decade, the number of personnel and the cost of the office grew massively. The growth was entirely on the operational side as the investment team has remained tiny. While my investment portfolio grew substantially, the investments I had made were almost entirely passive and TABLE simply needed to account for them and meet capital calls as they came in. While TABLE purchased additional software and other systems that were supposed to improve productivity, the team kept increasing in size at a rapid rate, and the expenses continued to grow even faster. While I would periodically question the growing expenses and high staff turnover, I stayed uninvolved with the office other than a once-a-year meeting when I briefly reviewed the operations and the financials and determined bonus compensation for the President and the CFO. I spent no time with any of the other employees or the operations. The whole idea behind TABLE was that it would handle everything other than my day job so that I would have more time for my job and my family. Over the last six years, expenses ballooned even further, employee turnover accelerated, and I became concerned that all was not well at TABLE. It was time for me to take a look at what was going on. Nearly four years ago, I recruited my nephew who had recently graduated from Harvard and put him to work at Bremont, a British watchmaker, one of my only active personal investments to figure out the issues at the company and ultimately assist in executing a turnaround. He did a superb job. When he returned from the UK late last year after a few years at Bremont, I asked him to help me figure out what was going on with TABLE. When I explained to TABLE’s president what he would be doing, she became incredibly defensive, which naturally made me more concerned. My nephew went to work by first meeting with each employee to understand their roles at the company and to learn from them what ideas they had on how things could be improved. He got an earful. Our first step in helping to turn around TABLE was a reduction in force including the president and about a third of the team, retaining excellent talent that had been desperate for new leadership. Now here is where I need your advice. All but one of the employees who were terminated acted professionally and were gracious on the way out (excluding the president who had a notice period in her contract, is currently still being paid, and with whom I have not yet had a discussion). The highest compensated terminated employee other than the president, an in-house lawyer (let’s call her Ronda), told us that three months of severance was not enough and demanded two years’ severance despite having worked at the company for only two and one half years. When I learned of Ronda's request for severance, I offered to speak with her to understand what she was thinking, but she refused to do so. A few days ago, we received a threatening letter from a Silicon Valley law firm. In the letter, Ronda’s counsel suggests that her termination is part of longstanding issues of ‘harassment and gender discrimination’ – an interesting claim in light of the fact that Ronda was in charge of workplace compliance – and that her termination was due to: “unlawful, retaliatory, and harmful conduct directed towards her. Both [Ronda] and I [Ronda’s lawyer] have spoken with you about [Ronda’s] view of what a reasonable resolution would include given the circumstances. Thus far, TABLE has refused to provide any substantive response. This letter provides the last opportunity to reach a satisfactory agreement. If we cannot do so, [Ronda] will seek all appropriate relief in a court of competent jurisdiction.” The letter goes on to explain the basis for the “unsafe work environment” claim at TABLE: “In early 2026, Pershing Square’s founder Bill Ackman installed his nephew in an unidentified role at TABLE, Ackman’s family office. [His nephew]—whose only work experience had been for TABLE where he was seconded abroad for the last four years to a UK watch company held by Ackman—began appearing at TABLE’s offices and conducting interviews of employees without a clear explanation of his role or the purposes of these interviews. During this period, he made a series of inappropriate and genderbased [sic] comments to multiple employees that created an unsafe work environment. Among other things, [his nephew] made remarks about female employees’ ages (“Tell me you are nowhere near 40”), physical appearance (“Your body does not look like you have kids”), as well as intrusive questions about family planning and sexual orientation (“Who carried your son? Who will carry your next child?”). These incidents were reported to senior leadership at TABLE and Pershing Square. Rather than being addressed appropriately, the response from senior management reflected, at best, willful blindness to the inappropriateness of [his nephew]’s remarks and, at worst, tacit endorsement.” The above allegations about my nephew had previously been brought to my attention by TABLE’s president when they occurred. When I learned of them, I told the president that I would speak to him directly and encouraged her to arrange for him to get workplace sensitivity training. The president assured me that she would do so. When I spoke to my nephew, he explained what he actually had said and how his actual remarks had been received, not at all as alleged in the legal letter from Ronda’s counsel. I have also spoken to others at the lunch table who confirmed his description of the facts. In any case, he meant no harm, was simply trying to build rapport with other employees, and no one, as far as I understand, was offended. Ironically, Ronda claims in her legal letter that TABLE didn’t take HR compliance seriously, yet Ronda was in charge of HR compliance at TABLE and the person who gave my nephew his workplace sensitivity training after the alleged incidents. In any case, Ronda, as head of compliance, should have kept a record or raised an alarm if indeed there was pervasive harassment or other such problems at the company, and there is no evidence whatsoever that this is true. So why does Ronda believe she can get me to pay her nearly $2 million, i.e., two years of severance, nearly one year of severance for each of her years at the company? Well, here is where some more background would be helpful. Over the last two months, I have been consumed with a major family medical issue – one of my older daughters had a massive brain hemorrhage on February 5th and has since been making progress on her recovery – and I am in the midst of a major transaction for my company which I am executing from a hospital room office next to her . While the latter business matter is publicly known, the details of my daughter’s situation are only known to Ronda because of her role at our family office. Now, let’s get back to the subject at hand. Unfortunately, while New York and many other states have employment-at-will, there has emerged an industry of lawyers who make a living from bringing fake gender, race, LGBTQ and other discrimination employment claims in order to extract larger severance payments for terminated employees, and it needs to stop. The fake claim system succeeds because it costs little to have a lawyer send a threatening letter and nearly all of the lawyers in this field work on contingency so there is no or minimal cash cost to bring a claim. And inevitably, nearly 100% of these claims are settled because the public relations and legal costs of defending them exceed the dollar cost of the settlement. The claims are nearly always settled with a confidentiality agreement where the employee who asserts the fake claims remains anonymous and as a result, there is no reputational cost to bringing false claims. The consequences of this sleazy system (let’s call it ‘the System’) are the increased costs of doing business which is a tax on the economy and society. There are other more serious problems due to the System. Unfortunately, the existence of an industry of plaintiff firms and terminated employees willing to make these claims makes it riskier for companies to hire employees from a protected class, i.e., LGBTQ, seniors, women, people of color etc. because it is that much more reputationally damaging and expensive to be accused of racism, sexism, and/or intolerance for sexual diversity than for firing a white male as juries generally have less sympathy for white males. The System therefore increases the risk of discrimination rather than reducing it, and the people bringing these fake claims are thereby causing enormous harm to the other members of these protected classes. So what happened here? Ronda was vastly overpaid and overqualified for the job that she did at TABLE. She was paid $1.05 million plus benefits last year for her work which was largely comprised of filling out subscription agreements and overseeing an outside law firm on closing passive investments in funds and in private and venture stage companies, some compliance work, and managing the office move from one office to another. She had a very good gig as she was highly paid, only had to go into the office three days a week, and could work from anywhere during the summer. Once my nephew showed up and started to investigate what was going on, she likely concluded that there was a reasonable possibility she would be terminated, as her job was in the too-easy-and-to-good-to-be-true category. The problem was that she was not in a protected class due to her race, age or sexual identity so she had to construct the basis for a claim. While she is female and could in theory bring a gender-based discrimination claim, she reported to the president who is female and to whom she is very close, which makes it difficult for her to bring a harassment claim against her former boss. When my nephew complimented a TABLE employee at lunch about how young she looked – in response to saying she was going to her 40-year-old sister’s birthday party, he said ‘she must be your older sister’ – Ronda immediately reported it to our external HR lawyer. She thereby began building her case. The other problem for Ronda bringing a claim is that she was terminated alongside 30% of other TABLE employees as part of a restructuring so it is very difficult for her to say that she was targeted in her termination or was retaliated against. TABLE is now hiring an external fractional general counsel as that is all the company needs to process the relatively limited amount of legal work we do internally. In short, Ronda was eminently qualified and capable and did her job. She was just too much horsepower for what is largely an administrative legal role so she had to come up with something else to bring a claim. Now Ronda knew I was a good target and it was a good time to bring a claim against me. She also knew that I was under a lot of pressure because on March 4th when Ronda was terminated, my daughter had not yet emerged from consciousness, she was not yet breathing on her own, and my daughter and we were fighting for her life. I was and remain deeply engaged in her recovery while at the same time I was working on finishing the closing for the private placement round for my upcoming IPO. Ronda also knew that publicity about supposed gender discrimination and a “hostile and unsafe work environment” are not things that a CEO of a company about to go public wants to have released into the media. And she may have thought that the nearly $2 million she was asking for would be considered small in the context of the reputational damage a lawsuit could cause, regardless of the fact that two years of severance was an absurd amount for an employee who had only worked at TABLE for 30 months. She also likely considered that I wouldn’t want to embarrass my nephew by dragging him into the klieg lights when her claims emerged publicly. So, in summary, game theory would say that I would certainly settle this case, for why would I risk negative publicity at a time when I was preparing our company to go public and also risk embarrassing my nephew. Notably, she hired a Silicon Valley law firm, rather than a typical NY employment firm. This struck me as interesting as her husband works for one of the most prominent Silicon Valley venture firms whose CEO, I am sure, has no tolerance for these kinds of fake claims that sadly many venture-backed companies also have to deal with. I mention this as I suspect her husband likely has been working with her on the strategy for squeezing me as, in addition to being a computer scientist, he is a game theorist. My only advice for him is to understand more about your opponent before you launch your first move. All of the above said, gender, race, LGBTQ and other such discrimination is a real thing. Many people have been harmed and deserve compensation for this discrimination, and these companies and individuals should be punished for engaging in such behavior. Which brings me to the advice I am seeking from the X community. I am not planning to follow the typical path and settle this ‘claim.’ Rather, I am going to fight this nonsense to the end of the earth in the hope that it inspires other CEOs to do the same so we shut down this despicable behavior that is a large tax on society, employment, and the economy and contributes to workplace discrimination rather than reducing it. Do you agree or disagree that this is the right approach?

Well deserved follow. But I’m floored. I knew it was bad. I sensed it was dogsh*t. But this is infinitely worse than I expected. When this goes, and it will… the most disheartening piece is….. the Fed will print to cover it. They will blow up the scapegoats, the global economy will teeter, but the $10-20T they will inject …. Sigh 🫣🤬 It will just go to enrich all of us who have assets. And Josh, Mary, and Joe. As well as every wage earner on earth, will get completely blown out of the system. It’s heartbreaking. @MikeyyyyG

I believe everyone in PE and PC knows exactly what is going on. PE is remarkably proficient at kicking the can down the road, but it looks like the end of the road to me.

143x is an INCREDIBLE return... But being an angel investor in something that is now worth $852B and only seeing 142X your money? Holy Dilution