پن کیا گیا ٹویٹ

$Pypl love that the CEO uses the rocket emoji…think stock is ready to run!!

Alex Chriss@acce

@PatMcAfeeShow @Venmo 💪🏻🚀

English

Rodney A. Lambert

351 posts

@PatMcAfeeShow @Venmo 💪🏻🚀

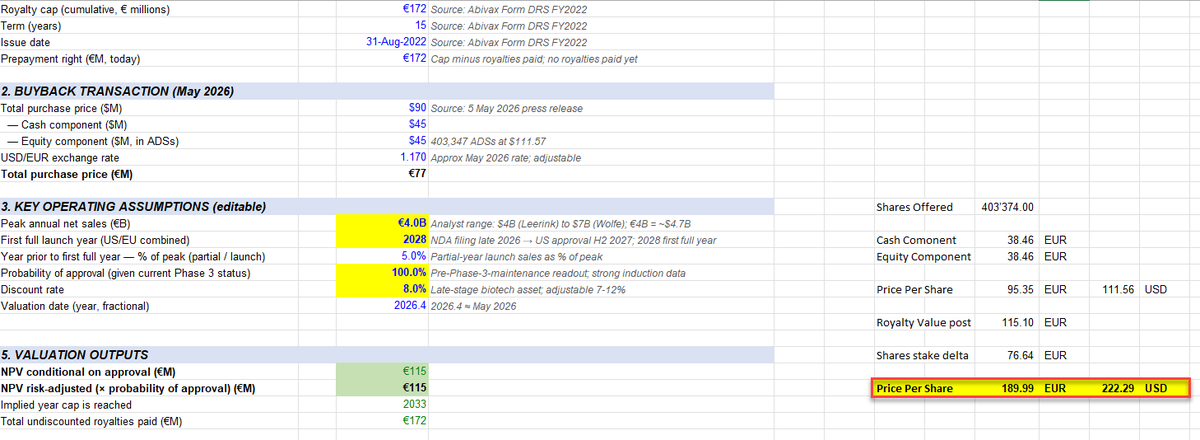

***Free alpha*** Part 2 Now many of you bought the dip and/or many of you are waiting for a certain price to breakeven, but IF $abvx go at it alone , what is fair price? (so any sale below this number you're selling below fair value and no M&A premium) Again 3 snippets: 1. Assumptions, imho opinion despite being one of the biggest bulls, I have taken conservative numbers and also factored in future dilution to fund launch till profitability 2. Full DCF projections up until the patents should hold ~2039 ( PMs like @Biohazard3737 shared that they had some of the best lawyers validate this and many sources have since then validated the fact protection should run to around 2039) 3. Value per share $153.17, still another 44% still to go ($106 right now) to accurately reflect what $abvx is worth without M&A (again super conservative numbers)

Bought 1/2 position in $ABVX at 70.30. Not my usual style, but think the odds of a rebound by end of week are greater than continued price degradation. Likely a short-term trade for me.

6 am paris time tomorrow confirmed