Jared Lawrence

9.6K posts

Jared Lawrence

@Beyondfinancee

Trader & Investor of 10 years 📈 Founder of Beyond Finance - Helping others build wealth within the Bittensor Eco-system. Free weekly 'Beyond Alpha' report 👇

Katılım Nisan 2021

607 Takip Edilen2.8K Takipçiler

We have yet to push @heydittoai to the CT masses.

We are almost there.

A Bittensor Awakening will be spawned.

Yan Liberman@YanLiberman

English

Jared Lawrence retweetledi

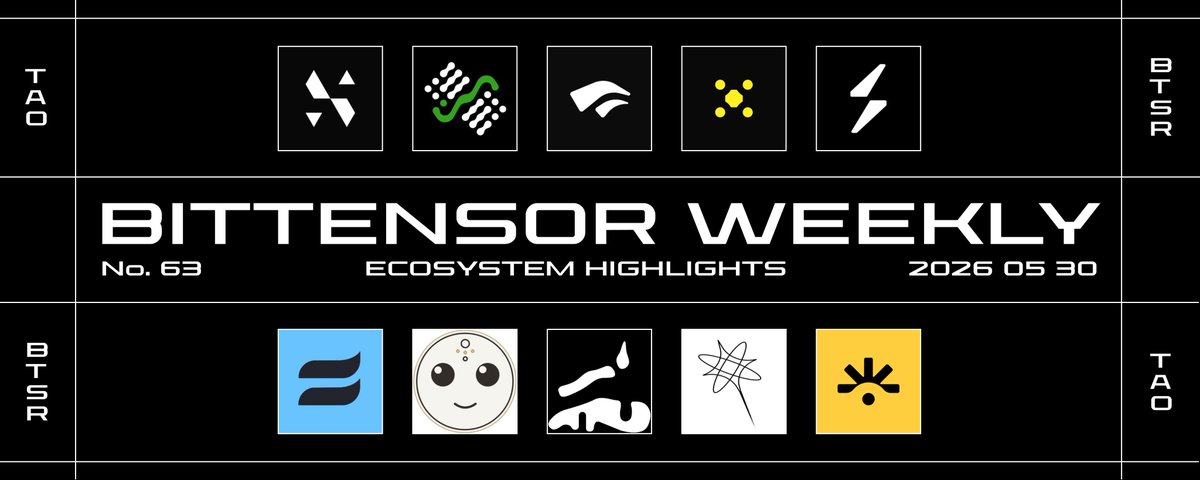

Bittensor Ecosystem Highlights of the Week #63

// SUBNET UPDATES & ACHIEVEMENTS

➤ @chutes_ai SN64

Jon Durbin successfully demonstrated decentralized training of a 176B-parameter model across four internet-connected nodes using Parallax.

(bit.ly/4ecgYYd)

Chutes rebuilt its infrastructure, significantly reducing model saturation and improving reliability across its flagship models.

(bit.ly/49vTXwO)

➤ @webuildscore SN44

They have deployed their first vision agent in production on an Avia fuel station.

(bit.ly/4dPwo3h)

➤ @zeussubnet SN18

Zeus launched their new rebuilt website. You can try their weather forecasting API without a key on it.

(x.com/zeussubnet/sta…)

(x.com/wouterhar/stat…)

➤ @heydittoai SN118

DittoCode is live, you can now build and share apps on Ditto.

(x.com/heydittoai/sta…)

➤ @SwarmSubnet SN124

Swarm developed a proof of concept of a real-time fire detection from an autonomous drone, using @manakoai to detect the fire and @chutes_ai to decide what to do.

(x.com/SwarmSubnet/st…)

They’re expanding beyond individual drone challenges with a new robotics lab, broader benchmarks, and a focus on general autonomous flying agents.

(x.com/SwarmSubnet/st…)

➤ @actualinc SN95

Actual Client v0.14.0 is now live for private beta users, with a major UI update across macOS, Linux, and Windows.

(x.com/Tom_A_Lynch/st…)

➤ @TargonCompute SN4

Over the past month, they have repurchased 2000 TAO of SN4 alpha using organic revenues.

(x.com/TargonCompute/…)

➤ @theminos_ai SN107

Minos expanded its live variant-calling benchmark to chromosome 21.

(x.com/theminos_ai/st…)

Minos will be presenting two works at The American Society of Human Genetics (ASHG) this fall.

(x.com/theminos_ai/st…)

➤ @QuasarModels SN24

They dropped their Quasar-Preview model on Hugging Face.

(x.com/QuasarModels/s…)

➤ @404gen_ SN17

404 showcased an early agent-built browser game using procedurally generated Three.js assets from their upcoming competition.

(x.com/404gen_/status…)

➤ @desearch_ai SN22 x Ditto SN118

Ditto agents are integrating Desearch as their native search layer.

(x.com/desearch_ai/st…)

➤ @QuantumSN48 SN48

Half-price quantum compute is live.

(x.com/QuantumSN48/st…)

➤ @yanez__ai SN54

Yanez is showcasing Proof of Humanhood and Proof of Uniqueness as a way to prevent fraud without exposing identity data.

(x.com/yanez__ai/stat…)

➤ @b1m_ai SN105

Beam teasing Beam Transfer Studio, a platform for orchestrating distributed data transfers across clouds, databases, and storage providers.

(x.com/b1m_ai/status/…)

➤ @Ninja_Subnet SN66

Ninja shipped a POLAR-style rollout pipeline to turn live coding-agent competitions into training data. (x.com/Ninja_Subnet/s…)

➤ @trishoolai SN23

Trishool’s Halo improved its F1 score from 75% to 87%, closing the gap with QwenGuard.

(x.com/xnavkumar/stat…)

They also shared their updated product roadmap.

(x.com/trishoolai/sta…)

➤ @affine_io SN120

They’re invited by @Alibaba_Qwen to attend the very first global Qwen Conference in Singapore.

(x.com/affine_io/stat…)

➤ @ai_detection SN32

They released a Canvas LMS plugin, to bring AI-generated content detection directly into schools and universities' existing workflows.

(x.com/ai_detection/s…)

➤ @mvtrx_79 SN79

GenTRX is live on mainnet.

(x.com/mvtrx_79/statu…)

// SUBNET INVESTMENT

➤ @IOTA_SN9 SN9

@stillcorecap has invested in SN9 alpha token.

(x.com/markjeffrey/st…)

// NEW SUBNET

➤ @say_gm_ SN28

The Venice of Bittensor is here.

(x.com/mogmachine/sta…)

➤ @Taolepathy SN25

@KeithSingery finally decided to end the embryon competition and use his slot to develop his own subnet.

(x.com/KeithSingery/s…)

// BITTENSOR ECOSYSTEM

➤ @opentensor

Conviction upgrade is now live on mainnet.

(x.com/bloomberg_seth…)

// PODCASTS & ARTICLES

➤ @opentensor Novelty Search with @const_reborn on the mechanics of Conviction

(x.com/opentensor/sta…)

➤ Hash Rate by @markjeffrey with @centrum_blue from @theminos_ai

(x.com/markjeffrey/st…)

➤ @VenturaLabs podcast with @peytonspencer and @sebyrubino

(x.com/VenturaLabs/st…)

➤ Ventura Labs podcast with @Swamination from @YumaGroup

(x.com/VenturaLabs/st…)

➤ Inventive Mechanisms podcast with @macrocrux and @Austin_Aligned on @Apex_SN1 x @AureliusAligned

(x.com/MacrocosmosAI/…)

➤ @SubnetSummerTAO AMA with @babelbit

(x.com/babelbit/statu…)

➤ Subnet Summer AMA with @vocence_bt

(x.com/SubnetSummerTA…)

$TAO

English

Exactly! I’m not sure people have fully clicked what @heydittoai is doing here yet… so many subnets can be plugged into ditto to give them more exposure and improve what they are doing.

Once built it will be the full bittensor stack that you can plug into businesses where it utilises all the best subnets to produce a complete operating system back end + front end.

It’s what has been missing to allow mass adoption

English

The end game was never hundreds of disconnected subnets.

The end game was coordination.

One interface.

Many specialized services underneath.

Users don't need to understand the machinery.

They just need something that works.

And that's where things get interesting.

Ditto@heydittoai

We just supercharged DittoCode and Deep Research. DittoSearch is now LIVE! Powered by Bittensor's very own @desearch_ai All Ditto agents now default to the SOTA service of Desearch which means; Try it for yourself today ↓

English

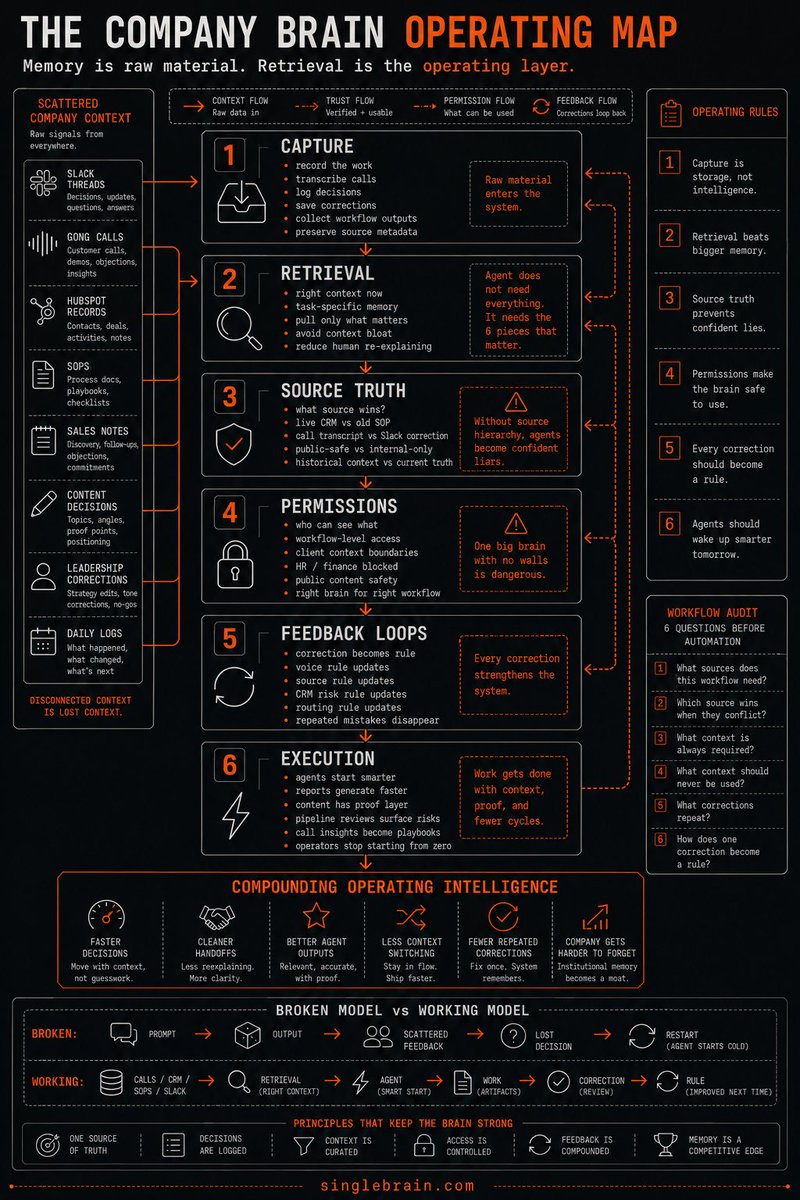

Every company is missing the same layer:

A company brain.

Right now, the memory of the business is scattered across calls, docs, Slack threads, dashboards, SOPs, and people's heads.

That's the part people miss when they talk about a company brain.

The value isn't a giant folder of company knowledge. Every company already has that.

The real advantage is the intelligence layer that sits between all that context and the work your team needs done.

This is the layer every AI-native company will need:

ericosiu@ericosiu

English

@markjeffrey And then the cycle repeats!

But yess Argentina is a beautiful place

English

@Beyondfinancee I dunno. Dude runs Palantir, can see all.

He thinks where you at is the place to be :)

English

@jordan_ross_8F check out @heydittoai you can connect your hermes or openclaw and make it 10x better

English

Hermes can either make you a F ton of money or waste ALL of your time.

Learn from my mistakes and start using this software properly.

If you started building with Hermes in the last 30 days, you will want to know the big mistakes to watch out for that will kill your productivity.

Jordan Ross@jordan_ross_8F

English

Jared Lawrence retweetledi

Great pod with Grant on @heydittoai -- which I'm fascinated with + using right now.

It's an agentic front end that is tying all the Bittensor subnets together.

x.com/VenturaLabs/st…

Ventura Labs@VenturaLabs

Ep. 95 - Peyton Spencer & Seby Rubino Peyton @peytonspencer is building Ditto @heydittoai Seby @sebyrubino created BigTensor @bigtensorai Timestamps 0:55 - Introduction 1:37 - Ditto as Agentic Operating System 4:55 - Ditto Apps: Replace Patreon & Shopify 6:54 - Subnet 118: Agent Memory Architecture 9:57 - Harness vs. Infrastructure Competitions 11:53 - Mac Mini Mining on Bittensor 14:38 - Earning on Ditto Outside Mining 15:29 - Vibe Mining: Agent-Driven Bittensor 17:47 - API & Agent Sandbox Integrations 18:41 - Const's Agent-Native Sign-Up Feature 20:34 - Knowledge Graph Licensing & Monetization 25:35 - Building a Shopify Store With One Prompt 26:51 - Live Demo: Background Agent Tasks 29:32 - Multi-Pronged Memory Search & LongMemEval 30:31 - Miners Optimizing Agent Memory 32:39 - Claude Desktop + Ditto MCP Demo 35:11 - Ditto Hub: Sharing & Monetizing Knowledge 37:58 - Monetizing Code & AI Knowledge 41:11 - BigTensor: Bittensor Builder Studio 43:31 - BigTensor Tokenomics 45:11 - BigTensor Cohort & Future Launches 46:08 - Peyton's BigTensor Experience 47:53 - Roadmap: Ditto Code, Desearch & Leadpoet 50:31 - Monetizable Artifacts by End of June 52:39 - Deleting Slack With Ditto 53:29 - Advice for Builders

English

@heydittoai coming out strong with SN integrations...

@hippius_subnet ☑️

@desearch_ai ☑️

Guess who's next?!?

Desearch.ai@desearch_ai

Ditto agents are integrating Desearch as their native search layer. @heydittoai gives agents memory and workspace context. Desearch brings real-time web intelligence into those workflows. Agent memory now has native decentralized search.

English

Do you ever sleep @heydittoai ???

The updates keep on coming and this one is a BIG ONE.

Ditto@heydittoai

DittoCode is LIVE! Build and share apps with the world! Now the only constraint is your imagination. Next, you will be able to monetization your creations to anyone on the internet. We can't wait to see what you make!

English

@_0xVerm @heydittoai Nice thanks for sharing this will check it out! Yeah there are many layers to building good architecture that is effective and efficient and many tools that do a number of things well but not everything in one place. This is what @heydittoai is doing

English

@Beyondfinancee @heydittoai Will check it out. Recently discovered AtomicMemory though and it reframes the problem entirely, recall is only half of it, governance and contradiction detection is where most solutions fall short. github.com/atomicstrata/a…

English

Jared Lawrence retweetledi

If you're struggling with memory recall with your agent or across agents then I'd highly recommend giving @heydittoai a try.

- Data storage impoved

- Recall 10x better

- API cost cut significantly

and this is them just getting started!

Wait for what is coming very soon........... ⛏️⛏️

Ditto@heydittoai

Non-Ditto agents can sign up or login to Ditto from ANYWHERE. 1. Copy and send prompt to your agent 2. Click the secure link 3. Login or sign up Every agent you operate can now share artifacts and maximize memory, from anywhere. The agents are accelerating.

English

@csouthai @bigtensorai @sebyrubino @zipcodenetwork I’d like to see the mechanics behind the shorting first but my initial first thoughts were that it seems like it would be net negative for a lot of subnets because you could easily game it but if it’s a way to decrease extraction without too much damage elsewhere then maybe..

English

@Beyondfinancee @bigtensorai @sebyrubino @zipcodenetwork Nice. Thoughts on shorts? Doing a clip with Gordon on prospective shorts? If so will wait and see.. TIA

English

As I warned many times - DO NOT fade @sebyrubino

@zipcodenetwork looking like it wants much higher here and with lots in the pipeline for the upcoming weeks I wouldn't be fading him here either!

and some alpha for you... 👀

Zipcode finance buybacks will make @zipcodenetwork deflationary from 100% buy and burns. Coming soon!

Rand Group@randgroup

name the project

English

BUT being outside and active to clear your mind WILL create a positive flywheel of good health, better thoughts, more energy etc... which then leads to better QUALITY of time spent IN Bittensor NOT just quantity of time.

This is where most people go wrong - you can't keep up that speed forever so look after your health too 🙏

English

Bittensor is my only hobby…

Stopped playing golf, basketball, and surfing when I bought @zipcodenetwork.

And I’m still trying to find more time for $TAO.

It would be sacrilegious if I didn’t direct all my energy to leveraging Bittensor to improve the world?

English

👇

tennismandu22@tennismandu22

This is actually a very important point from @markjeffrey. When he says Ditto could become the “front-end interface” of Bittensor, I don’t think he means just another AI app. I think he means a consumer-facing memory + coordination layer sitting on top of the entire Bittensor ecosystem. Today Bittensor already has: - world class infrastructure - decentralized compute - inference - vision - speech - agents - storage …but most of it is still invisible to normal users. What Ditto is starting to build feels different. A clean interface. Persistent memory. Agent coordination. Context that compounds over time. Not just “chat with AI”. More like: an operational layer for interacting with an open AI economy. That’s potentially a much bigger idea. Let’s see what Ditto really has under the hood in the coming weeks!!! 👀👀👀

ART

English

whenever a small subnet sees strength

5GuRL is there to knock it down

today's victim: sn85 @vidaio_

yesterday's victim: sn118 @heydittoai

yall @ridges_ai holders better hope (s)he doesn't get bored

#bittensor $TAO $dTAO

English