@turtlespeed2020 Lockup period ending for some larger holders

English

Adam Till, CMT

11.5K posts

@MainSailfund

In trading it doesn't matter if your right or wrong as long as you make $$$$

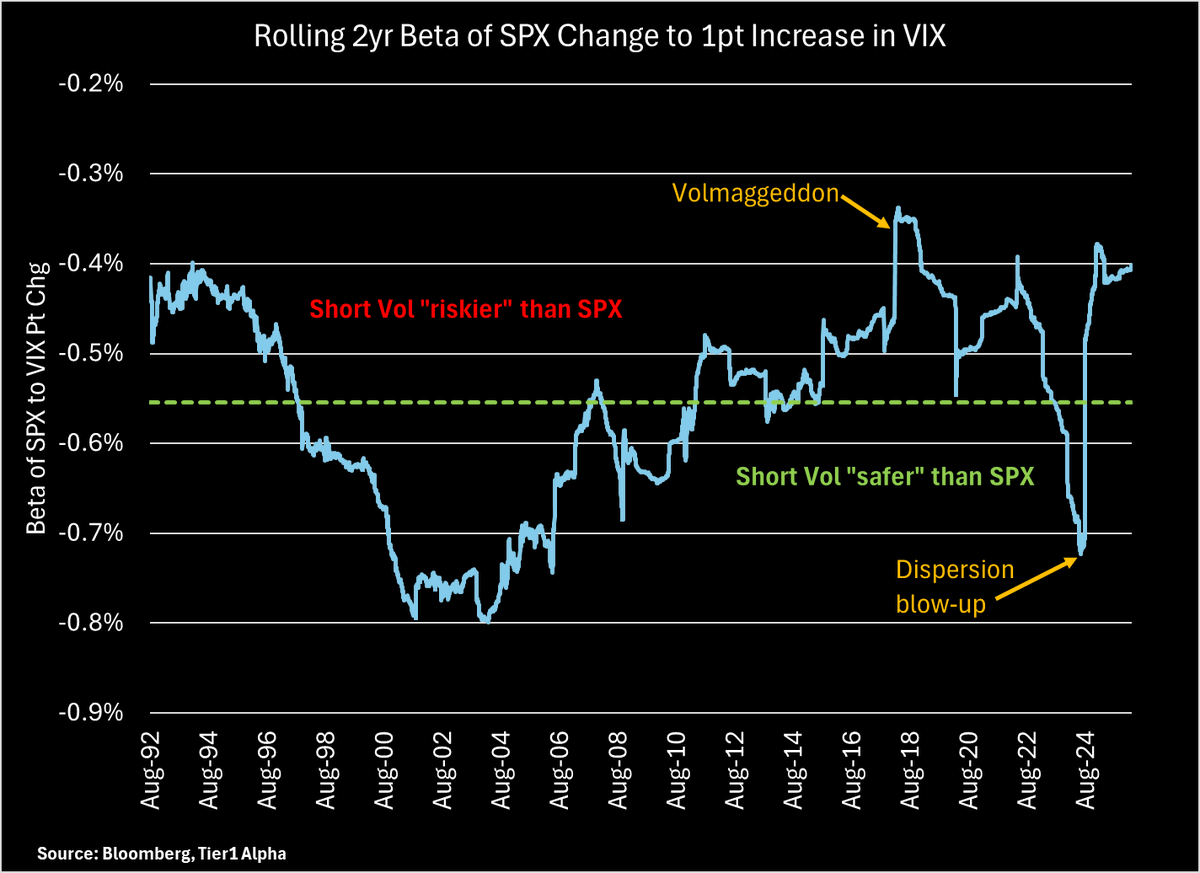

McElligott goes on to say that the current situation of high implied volatility and low realized volatility has three "Captain Obvious" conclusions: - “Nothing Ever Happens,” as “Worst-Case Scenario” tail-risks fail to materialize... then seeing Spot rally and Vol melt, as Hedges roast / decay... -“Extremely Steep Skew Creates Conditions for a Crash"... and we do... as the Hedges themselves create the “accelerant flow” Downside energy for an accident... [or] -The most perverse scenario, however, is a further Equities grind sideways to slightly down, but no “Crash” / no shocks... In other words, the Downside Hedges / Gamma people are spending risk-budget on fail to pay out because there’s no “Crash” and just a grinding leak, which only further drags already weak Equities performance. He goes on to say that he thinks we're in the last of these and notes the results of his back test: when VIX outperformance vs Spot SPX is this extreme on both a 1 week and 1 month -trailing windows, the prior 24 times on the average have seen VIX get absolutely CLOBBERED in the forward return profile...with median move down massive -16% to -35%, extreme hit rates (low % = VIX down) and most importantly, at significant excess hits vs standard vol bleed….with the only outlier where Volatility continued to shock higher being GFC and COVID -crashes, which needed “Economic Crisis” scenario.

If Iran allows China and India oil through the Strait, that's more than half of normal oil traffic already (7mmb/d). Throw in the Saudi East-West pipeline for redirection (another 7mb/d) and the blockade suddenly shrinks a lot

From Block's results $XYZ: “General and administrative expenses increased by $68.1m ... The increase was primarily driven by … an in-person company event held in Q3 2025" Can someone please explain: a) what kind of in-person event costs $68m? b) how can I get invited? 🌳🙏

FED’S SCHMID WARNS RATE CUTS COULD PROLONG INFLATION Fed’s Christopher Schmid says current rates aren’t slowing the economy and keeping inflation near 3% justifies restrictive policy. Productivity gains may support faster growth without fueling prices—but “we are not there yet.” Strong demand still outpaces supply, and transitory price shocks require focus on the Fed’s 2% inflation target. Opportunities exist to reduce bank reserves and shrink the Fed’s balance sheet.

I am working on something $PLTR.