Sabitlenmiş Tweet

AI plays with MASSIVE growth potential:

$TSLA - FSD (most advanced real world AI)

$PLTR - Extracts more value out of an orgs data

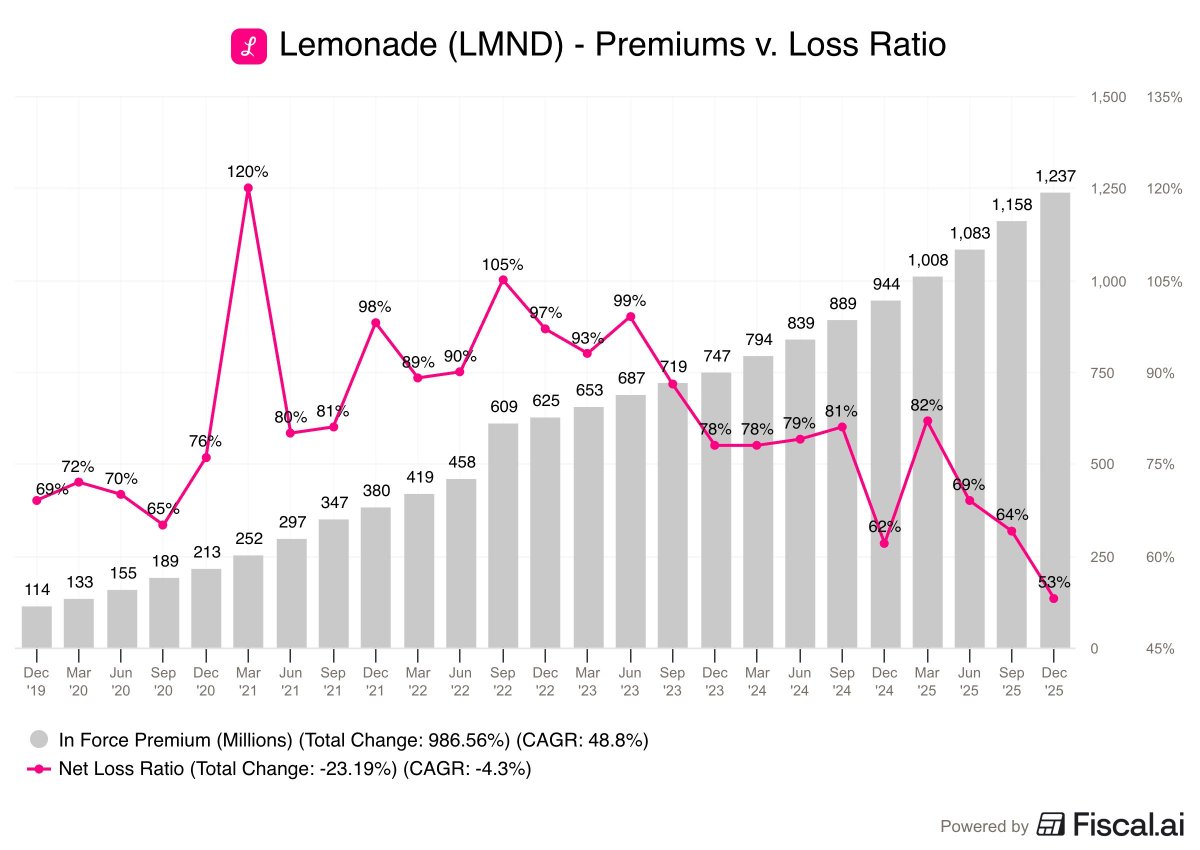

$LMND - AI driven data flywheel to reduce insurance costs

$DNA - Syn-bio shovels provider. Each shovel sold provides data to improve the next shovel

English