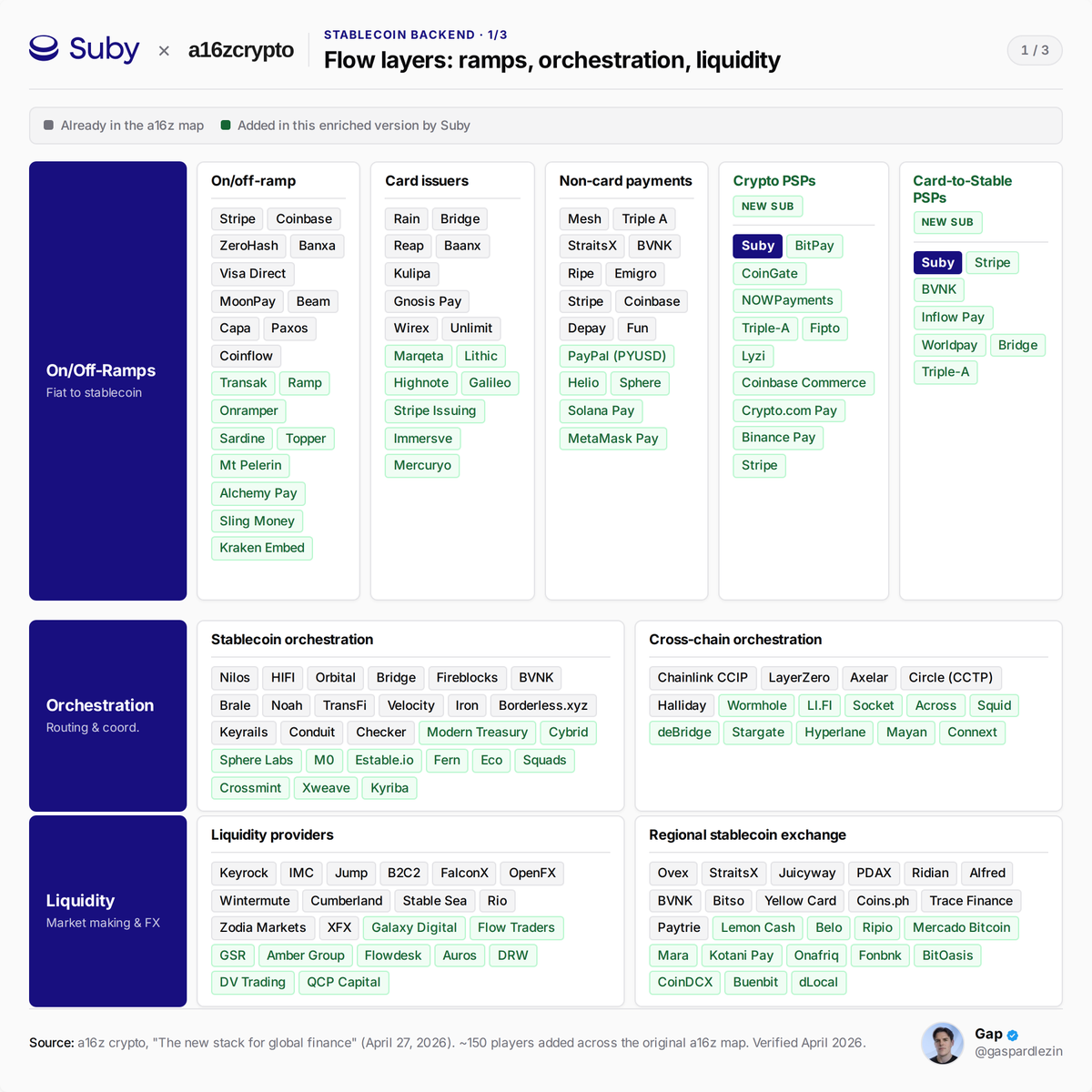

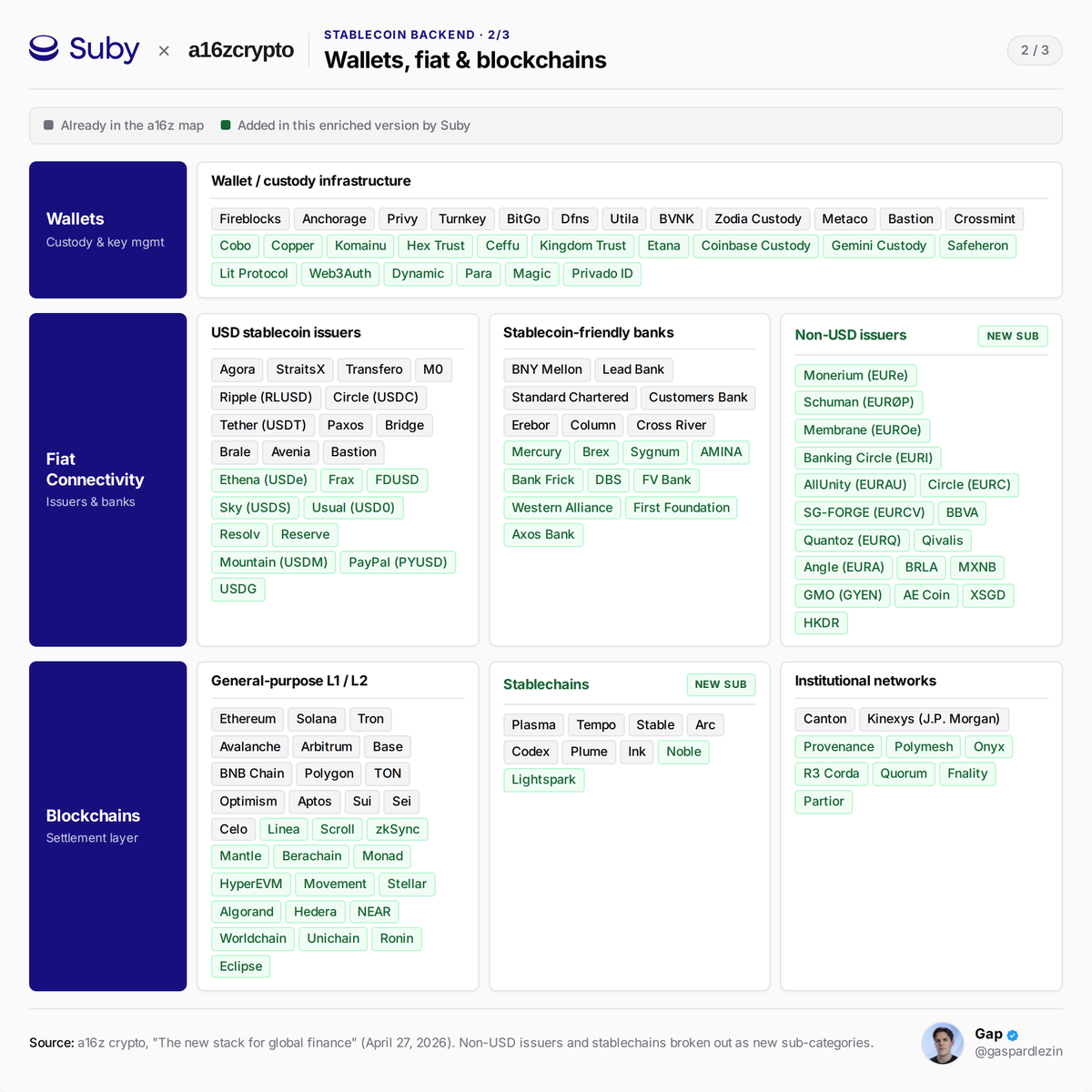

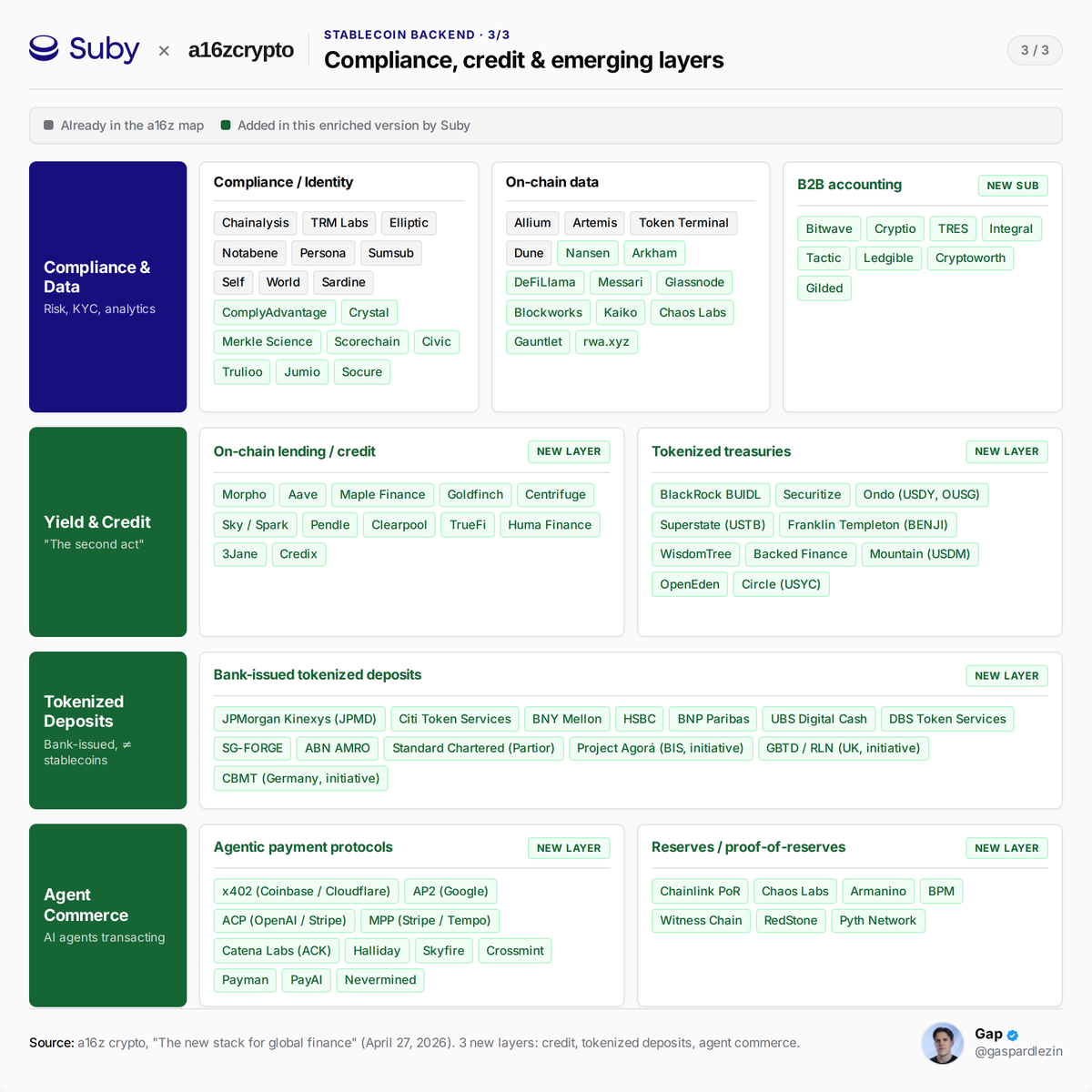

hunter@hxxntrr

Your 720 credit score is worth $250,000

not joking btw

Not in some "good credit unlocks opportunity" way

Literally. Right now. Chase, Amex, and US Bank will approve you for $250,000 in 0% business credit this week if you apply in the right order

Most people with a 720 score are using it to get a slightly better rate on a car loan

The people who understand what a 720 score actually unlocks are using it to fund entire businesses on bank money at zero interest

Here's the exact value of your score in dollars:

Below 680: $30K-$80K available. Limited banks. Shorter 0% windows

680-720: $80K-$150K available. Most major banks approve. Full 12-15 month windows

720-760: $150K-$250K available. Every bank approves. Maximum limits. Longest windows

760+: $250K-$400K+. Banks compete for you. Limits get disgusting

The difference between a 680 and a 760 isn't "better credit"

It's $170,000 in additional available capital at 0% interest

Most people treat their credit score like a report card. Something to feel good or bad about. Something that determines whether they get approved for a personal card with a $5K limit

The people running real businesses treat it like a borrowing capacity number. A specific dollar amount sitting at specific banks waiting for a specific sequence of applications

Here's what $250K at 0% actually means in practice:

You borrow $250K from Chase, Amex, and US Bank. Zero interest for 15 months.

You deploy it into your business. At month 10 you apply for a new round of 0% cards at different banks. Use the new cards to pay off the old ones. 0% window resets for another 12-15 months

People have been running this cycle for 5 years without paying a cent of interest

The total cost of accessing $250K in perpetual capital: roughly $6,000-$7,500 per year in processing fees to convert credit lines to cash

Compare that to:

SBA loan at 8% on $250K: $20,000/year in interest

MCA at 60% effective APR on $250K: $150,000/year in fees

VC funding at 15% equity on $250K exit at $5M: $750,000 in equity given away

Your 720 score is worth $250,000 in capital at a cost of $6,000/year

The bank designed the product this way on purpose. They're betting you'll forget to cycle before the 0% expires and start paying 24% APR forever. That's their entire business model on these cards

Most people do forget. You won't because you'll have a spreadsheet tracking every expiration date 12 months out

The application sequence that gets you to $250K:

Week 1: Amex first. Always. If you have any existing Amex card they don't hard pull existing cardholders. Apply for Amex Blue Business Plus and Amex Blue Business Cash simultaneously. Zero new inquiries if you're an existing cardholder. Expected: $50K-$100K

Week 2: Chase. They pull Experian in most states. Your Experian is clean because Amex didn't touch it. Apply for Chase Ink Business Unlimited and Chase Ink Business Cash. Expected: $50K-$75K

Week 3: US Bank, Wells Fargo, PNC. Each pulls a different bureau. Each sees a clean file. Expected: $30K-$75K

Total: $150K-$250K in 3 weeks. All at 0% for 12-18 months. None of it reporting to your personal credit bureau

Your 720 score has been sitting there the whole time

You just didn't know what it was worth

(We build the full stack. Bureau mapping, bank sequencing, application timing, everything. 700+ score required. Average deployment $175K. Link in bio)