@FriendlyCapMgmt Who would be your top-3 alternative GPs if you decide to redeem?

English

No More Parties

740 posts

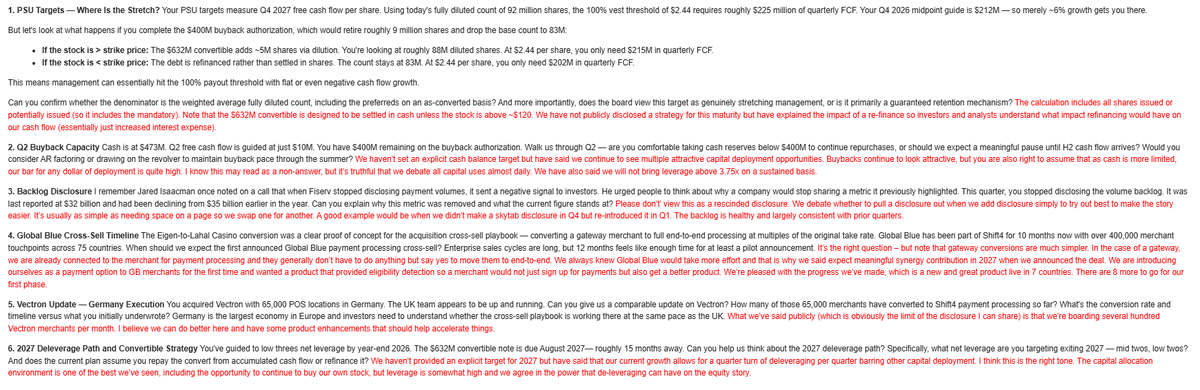

I think most of you know my bull case for $FOUR by now. But being bullish doesn't mean being blind. I have some tough questions for management that I think the investment community deserves answers to. Not sure if @Speedwell_LLC can help facilitate again like they did last quarter. Here are my 6 questions. 1. PSU Targets — Where Is the Stretch? Your PSU targets measure Q4 2027 free cash flow per share. Using today's fully diluted count of 92 million shares, the 100% vest threshold of $2.44 requires roughly $225 million of quarterly FCF. Your Q4 2026 midpoint guide is $212M — so merely ~6% growth gets you there. But let's look at what happens if you complete the $400M buyback authorization, which would retire roughly 9 million shares and drop the base count to 83M: If the stock is > strike price: The $632M convertible adds ~5M shares via dilution. You're looking at roughly 88M diluted shares. At $2.44 per share, you only need $215M in quarterly FCF. If the stock is < strike price: The debt is refinanced rather than settled in shares. The count stays at 83M. At $2.44 per share, you only need $202M in quarterly FCF. This means management can essentially hit the 100% payout threshold with flat or even negative cash flow growth. Can you confirm whether the denominator is the weighted average fully diluted count, including the preferreds on an as-converted basis? And more importantly, does the board view this target as genuinely stretching management, or is it primarily a guaranteed retention mechanism? I'm honestly not sure where the challenge is in these numbers. 2. Q2 Buyback Capacity Cash is at $473M. Q2 free cash flow is guided at just $10M. You have $400M remaining on the buyback authorization. Walk us through Q2 — are you comfortable taking cash reserves below $400M to continue repurchases, or should we expect a meaningful pause until H2 cash flow arrives? Would you consider AR factoring or drawing on the revolver to maintain buyback pace through the summer? 3. Backlog Disclosure I remember Jared once noted on a call that when Fiserv stopped disclosing payment volumes, it sent a negative signal to investors. He urged people to think about why a company would stop sharing a metric it previously highlighted. This quarter, you stopped disclosing volume backlog. It was last reported at $32 billion and had been declining from $35 billion earlier in the year. Can you explain why this metric was removed and what the current figure stands at? 4. Global Blue Cross-Sell Timeline The Eigen-to-Lahal Casino conversion was a clear proof of concept for the acquisition cross-sell playbook — converting a gateway merchant to full end-to-end processing at multiples of the original take rate. Global Blue has been part of Shift4 for 10 months now with over 400,000 merchant touchpoints across 75 countries. When should we expect the first announced Global Blue payment processing cross-sell? Enterprise sales cycles are long, but 12 months feels like enough time for at least a pilot announcement. 5. Vectron Update — Germany Execution You acquired Vectron with 65,000 POS locations in Germany. The UK team appears to be up and running. Can you give us a comparable update on Vectron? How many of those 65,000 merchants have converted to Shift4 payment processing so far? What's the conversion rate and timeline versus what you initially underwrote? Germany is the largest economy in Europe and investors need to understand whether the cross-sell playbook is working there at the same pace as the UK. 6. 2027 Deleverage Path and Convertible Strategy You've guided to low threes net leverage by year-end 2026. The $632M convertible note is due August 2027— roughly 15 months away. Can you help us think about the 2027 deleverage path? Specifically, what net leverage are you targeting exiting 2027 — mid twos, low twos? And does the current plan assume you repay the convert from accumulated cash flow or refinance it? @tlaubers @rookisaacman

🎙️ New Podcast Released! In this fantastic interview, we spoke with the CEO and CFO of Shift4! We covered everything from: 🔹 Capital allocation 🔹 Global Blue acquisition 🔹 What sets Shift4 apart from competition If you're interested in $FOUR, this is a must listen 👇