Sabitlenmiş Tweet

‼️🅿️rofit Ⓜ️aker‼️

6.5K posts

@ProfitMaker_X

💰 Options 💸 Stocks 🪙 Crypto ⬆️ Futures 🌇 Real Estate ~Tweets not investment advice. Do your own research!~

$MU | 𝐌𝐢𝐜𝐫𝐨𝐧: UBS maintains 𝐁𝐮𝐲, raises 𝐏𝐓 𝐭𝐨 $𝟓𝟑𝟓 Analyst sees memory super-cycle strengthening, with pricing power and LTAs supporting long-term earnings visibility.

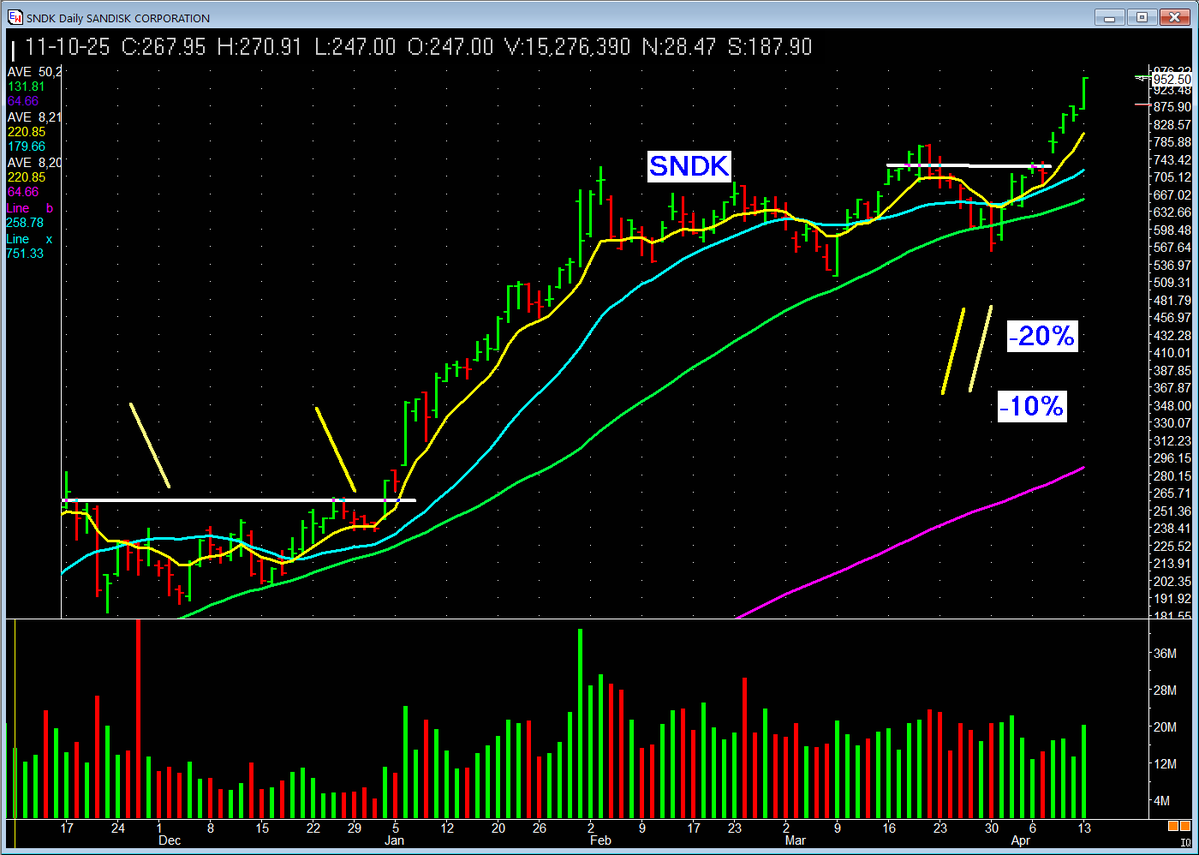

$MU $SNDK NAND >> HBM? Everyone is watching HBM. The smart money is watching NAND. The cascade nobody modeled. AI inference can't be solved by HBM alone. The capacity demand spills over: HBM → Server DRAM → NAND Each layer tightens as hyperscalers vacuum up supply. And NAND is now the most undersupplied link in the chain. The numbers: Late 2025: Some NAND types up 246% for certain buyers Nov 2025: Contract prices up 20–65%+ MoM depending on segment Q1 2026: NAND contract prices revised to +55–60% QoQ (up from earlier +33–38% estimates) Enterprise SSDs: +53–58% QoQ, a new quarterly record. Certain Enterprise NAND product have higher margins than HBM. Unbelievable times. $MU benefits on both sides. $SNDK is the pure play.

$MU $SNDK NAND >> HBM? Everyone is watching HBM. The smart money is watching NAND. The cascade nobody modeled. AI inference can't be solved by HBM alone. The capacity demand spills over: HBM → Server DRAM → NAND Each layer tightens as hyperscalers vacuum up supply. And NAND is now the most undersupplied link in the chain. The numbers: Late 2025: Some NAND types up 246% for certain buyers Nov 2025: Contract prices up 20–65%+ MoM depending on segment Q1 2026: NAND contract prices revised to +55–60% QoQ (up from earlier +33–38% estimates) Enterprise SSDs: +53–58% QoQ, a new quarterly record. Certain Enterprise NAND product have higher margins than HBM. Unbelievable times. $MU benefits on both sides. $SNDK is the pure play.

$AEHR just hit a new all-time high and is now up more than 25% 🙃