@CCapLP @darkstarsats @dan_tmt @WaltLightShed Agreed. They could not have a more powerful argument on force majeure here. It spells out directly being forced to stop network build

English

Chris Lytle

908 posts

@chlytle33

Partner at Smith Point Capital

*AMAZON IN TALKS TO BUY $9B SATELLITE GROUP GLOBALSTAR: FT

NEWS SpaceX/Starlink is one of the potential bidders for the FCC's AWS-3 spectrum auction linkedin.com/posts/mikedano…

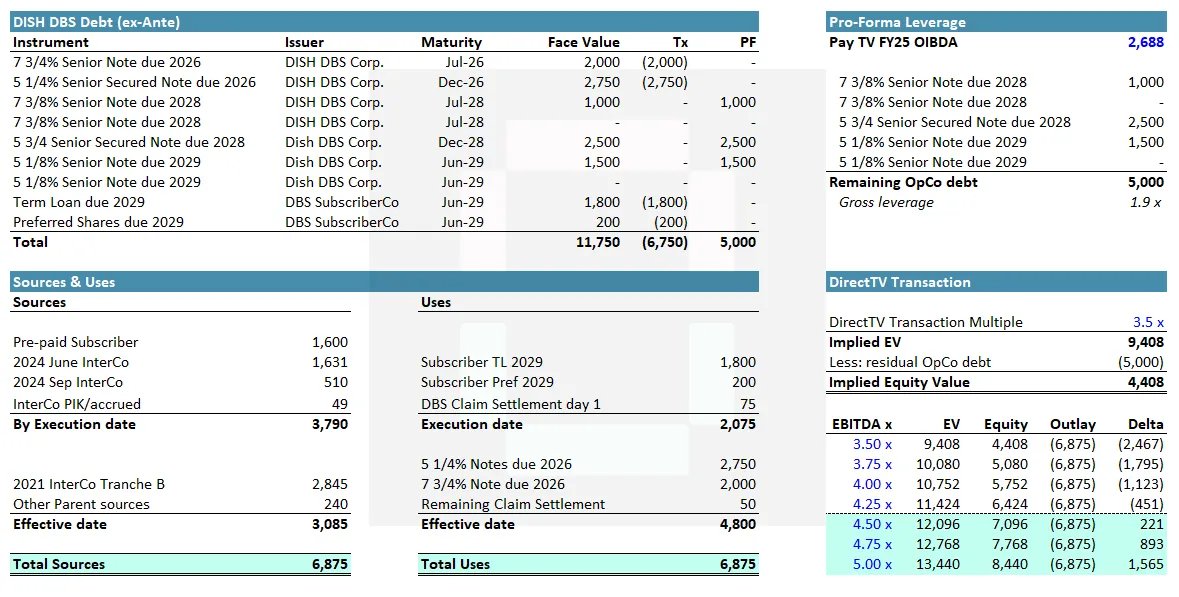

Had a moment to briefly scan through the RSA on the EchoStar DISH DBS restructuring Lots of moving parts but in short: (i) paydown of DBS SubscriberCo TL and preferred shares (ii) paydown of all the 2026 Notes (iii) funded via settlement of InterCo loans (through DNC) (iv) $125M Claims Settlement (v) further protections / cash sweep on residual notes Per my initial note the clean-up paves the way for a combination with DirecTV (and only makes sense in that context given the non-recourse nature of the OpCo debt). The RSA/TS is also riddled with references to a potential transaction. From a pure numbers perspective we know this is irrelevant to the core EchoStar $SATS thesis. Fwiw I estimate the deal to be cash neutral to the business on a >4.25x FY25 EBITDA sale to DirecTV. The value here is in accelerating the transition towards a new narrative as a Space Investment HoldCo, shedding legacy luggage and repositioning the Company with a new shareholder base.

$SATS RSA (and parent support through push down of interco loan) only makes sense in the context of a sale to DirectTV which I assume will also be announced in due course Pretty neutral to our core thesis with SpaceX