Dennis retweetledi

Dennis

4.6K posts

Dennis retweetledi

Fun fact…

$AMD now trades at a NTM P/E multiple that is 2x bigger than the $NVDA NTM P/E multiple.

$AMD trading at 46x NTM EPS

$NVDA trading at 23x NTM EPS.

Which stock do you think has more upside over the next 12 months from current prices?

Jonah Lupton@JonahLupton

SK Hynix just reported 2026 Q1 earnings. Revenues up +198% YoY Net income up +405% YoY Net income margins of 77% …and SK Hynix trades at 4x NTM EPS 🤣 These are wild times for memory stocks 😳 NFA. DYOR. *We own SK Hynix at @FirstWaveFund

English

Dennis retweetledi

Looks like it’s finally happening… the FDA is now prepared to move at least 14 peptides to the Category 1 list which means US based compounding labs/pharmacies will be able to make and sell them for human consumption.

This is great for $HIMS because they own both 503a and 503b facilities. This move by the FDA will destroy the grey market (90% comes from China) which has exploded over the past few years.

Ironically, I placed my typical biweekly peptide order this morning… soon I’ll be spending this money with $HIMS as will millions of other people.

I’ll be a guest on the @HimsHouse podcast next week to discuss my 3+ year investment thesis on $HIMS and why I think peptides will play a major role in the next phase of growth for the company.

NFA.

DYOR.

*We own $HIMS at @FirstWaveFund and added to our position this morning which is our first add in the last couple weeks.

English

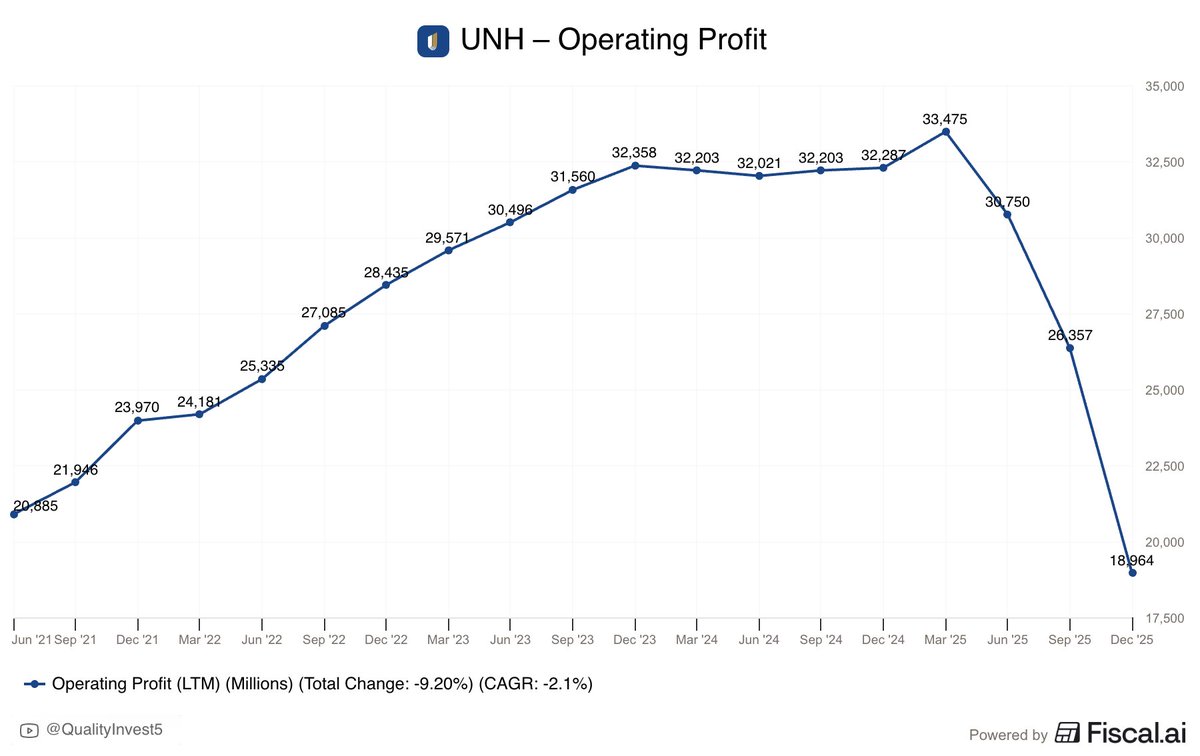

@ariaradnia Profits fells due to margin compression. They’re facing temporary reimbursement and cost pressures, not a declining business.

2025 revenue of 447 billion was a record high.

English

Dennis retweetledi

$META at 15x 2027 earnings is a buying opportunity regardless of what doomers say.

It’s now top pick at Morgan Stanley.

There are two things pressing the stock down now:

- Elevated capex

- Social media addiction cases

Elevated capex is not a problem as almost all of it is growth capex and it’s not speculative. It’s already seeing tangible ROI from AI spending in the form of higher ad conversion rates and quality. This is what led to reacceleration of growth in the last 2 years.

Legal worries about the potential accumulation of social media addiction charges are also unfounded. $META won’t be like Big-Tobacco in 1990s as its product isn’t “necessarily” harmful, unlike tobacco. Social media is being used in many productive ways.

So, the current discount is based more on false narratives than real risks.

If the current macro and geopolitical headwinds weighing on the broader market subside, $META should quickly recover provided that they deliver on 2026 targets.

Overall, it’s a great risk/reward here.

Sean@Sean14978416

$META: New Top Pick at Morgan Stanley.

English

@MMatters22596 I own SOFI around 19 and love the potential return but wouldn’t expect returns similar to massive tech hyper scalers.

Also own NBIS.

English

$SOFI

-42% YTD

If you ask me, $SOFI currently offers one of the most attractive setups in the market.

The entry zone has remained unchanged for months.

A move toward $100+ is possible over time.

To put this opportunity into perspective:

It feels similar to...

$PLTR at $25

$NBIS at $20

$ASTS at $17

Early, overlooked — before the real move.

Are you invested in $SOFI?

English

@SixSigmaCapital 41% operating margin a PEG at 0.9 a forward p/e of 20.

20% growth for META vs MSFT 12% or APPL 6-8%

Half of the planet uses at least one of their apps.

520 is a great entry. 450 is perfect. 400 or less is a rare opportunity.

Don’t overthink it.

English

What’s people’s thoughts on $META here?

Opportunity or trap? Cheap or expensive

English

Dennis retweetledi

$META is without a doubt the best opportunity in the MAG 7.

With a ~$1.3T market cap, it trades at a forward P/E of ~17, the lowest in the group.

At the same time, revenue is expected to grow ~30% in Q1 2026. Excluding $NVDA, it is the fastest-growing company in the MAG 7.

$META owns the three most used social media platforms in the world, and 3.5B people use at least one of its apps every day.

If Meta builds an AI model that is truly competitive, it could put it in the hands of billions of people overnight and monetize it immediately. Its distribution power is unmatched.

Smart glasses are also starting to put up serious numbers. Around 20M units are expected to be sold in 2026, and Meta owns roughly 80% of that market.

WhatsApp monetization finally seems close.

On top of that, Meta is becoming more efficient and is showing it can reduce headcount meaningfully through AI adoption.

Very few buys look as obvious as $META right now.

English

Dennis retweetledi

Gap is widening again.

Reminder:

$META is expected to produce $80 OCF/share in 2028.

English

Dennis retweetledi

Dennis retweetledi

Weighted average exercise price of the 2031 $META option plan is ~$2770.

Consensus right now for 2031 is ~$60-70/share in EPS, 42x P/E vs. today at ~20x which tells you how much management thinks they can beat estimates by over the next 5 years.

Majority of the plan has strikes of ~$3100-$3700.

English

Dennis retweetledi

From today’s conference with Morgan Stanley:

“We’re now securing upfront payments from customers, up to and including, in some cases, customers paying 100% upfront.”

— Marc Boroditsky, CRO of $NBIS

English

Dennis retweetledi

Quick take on the new $NBIS vs. $IREN debate.

We now have a lot more data.

In the last 3 months, $NBIS has:

- confirmed twice its $7–9B ARR guidance is on track

- confirmed ~60% of capex is already funded

- confirmed dilution will be less than expected

- received approval for a 1.2GW data center

- raised guidance to 2.5–3.0GW of contracted power (completely disproving the “Nebius will never secure enough power” argument)

- acquired Tavily

- launched Token Factory

- launched Aether

- had market data point to multiple subsidiaries being worth several billion dollars and growing fast

- noted pricing is increasing

- noted contract durations are increasing

- noted customers are increasingly paying in advance (sometimes 100%)

- confirmed 100% of customers use their software

- I have to stop here, but the full list would be incredibly long, I could literally add 20 more points just on product updates that will all increase the TAM massively and have great effects on stickiness and retention

My takeaway: Nebius is raising capital more efficiently and getting better deal terms because it looks like the serious long-term winner in the “new hyperscaler / neocloud” category, and a real competitor to AWS over time.

Other public players like $IREN (and others) face tighter financial constraints and dependencies, less integration across the stack, and less product depth than $NBIS.

The gap is clearly getting way bigger and more visible over time.

I tried to completely stop talking bad about stocks, especially stocks I do not hold in my own portfolio, but every now and then we have to talk about what's really happening.

English

Dennis retweetledi

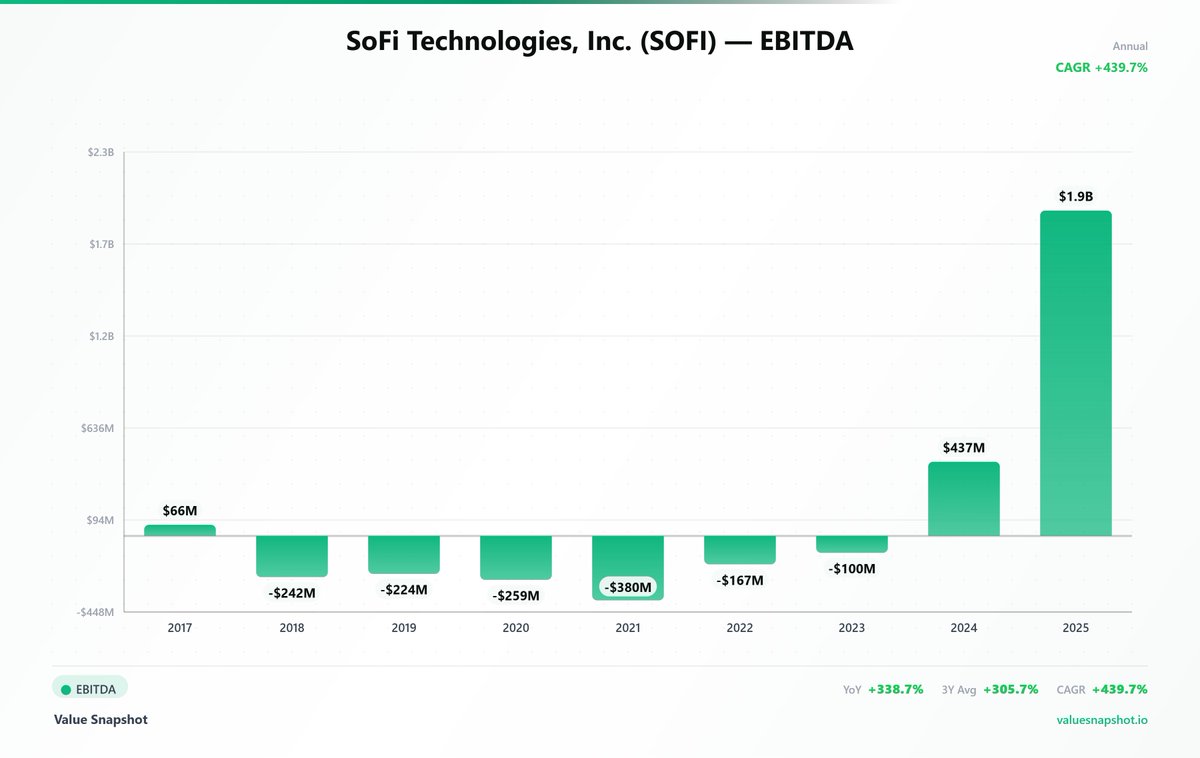

$SOFI five years ago...

~$17.76 per share

~Revenue of $1.1B

~Net income of -$484M

~Net margins of -44.5%

~EBITDA of -$380M

$SOFI now...

~$17.76 per share

~Revenue of $4.8B

~Net income of $481M

~Net margins of 10.1%

~EBITDA of $1.9B

Yeah... I like the stock here. Don't you? 👇

English

Dennis retweetledi

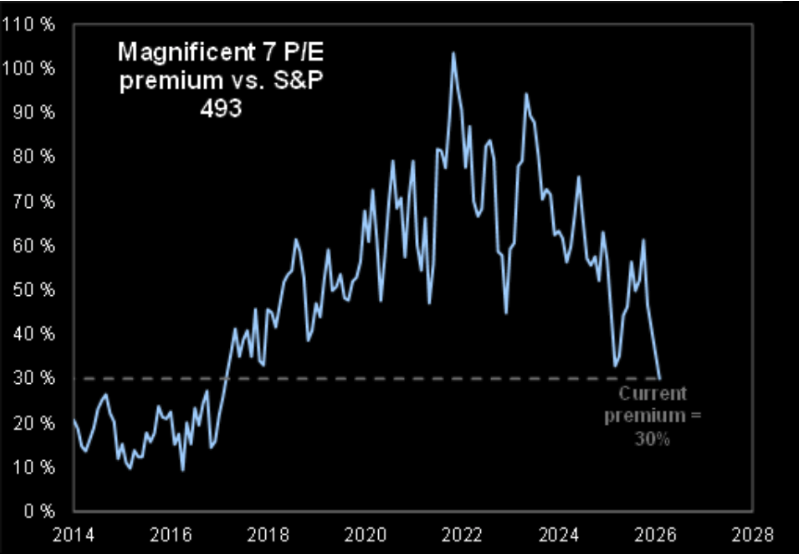

The Mag-7 used to trade at a 100% premium over the rest of the S&P. It's now collapsed to a 10-year low.

Do you realize what's happening?

English

Dennis retweetledi

$ZETA

*ZETA GLOBAL Q4 EPS $0.23, EST. $0.23

*REVENUE $395M, EST. $379.25M

*ZETA GLOBAL SEES Q1 2026 REVENUE $369M–$371M, EST. $362.19M

*ZETA GLOBAL RAISES FY2026 REVENUE VIEW TO $1.749B–$1.762B, EST. $1.73B

English

Dennis retweetledi

$SOFI five years ago:

• $18/share

• 1.9M members with ~$360M gross profit run-rate

$SOFI today:

• $18/share

• 13.7M members with ~$2.2B gross profit run-rate

Same price. Very different business.

Shay Boloor@StockSavvyShay

$SOFI is now below the ~$23B market cap requirement for S&P 500 eligibility. Any near-term inclusion hopes likely get delayed.

English

Dennis retweetledi

New strong $NVO oral Wegovy prescription numbers:

This is how prescriptions have increased week over week since launch:

4,290 → 20,382 → 26,794 → 29,410 → 38,423 → 52,299.

For comparison, same weeks (insured patients only):

• Wegovy injection: 174 → 1,017 → 1,925 → 3,296 → 5,756 → 8,925

• Zepbound (Eli Lilly): 1,911 → 10,040 → 20,162 → 27,960 → 23,967 → 29,838

Insured patients only. Symphony data.

#StocksToWatch #investing

English

Dennis retweetledi

Growth stocks crashing. Value stocks near all time highs. Just a matter of time until this is flipped. The only question is when…

English

Dennis retweetledi

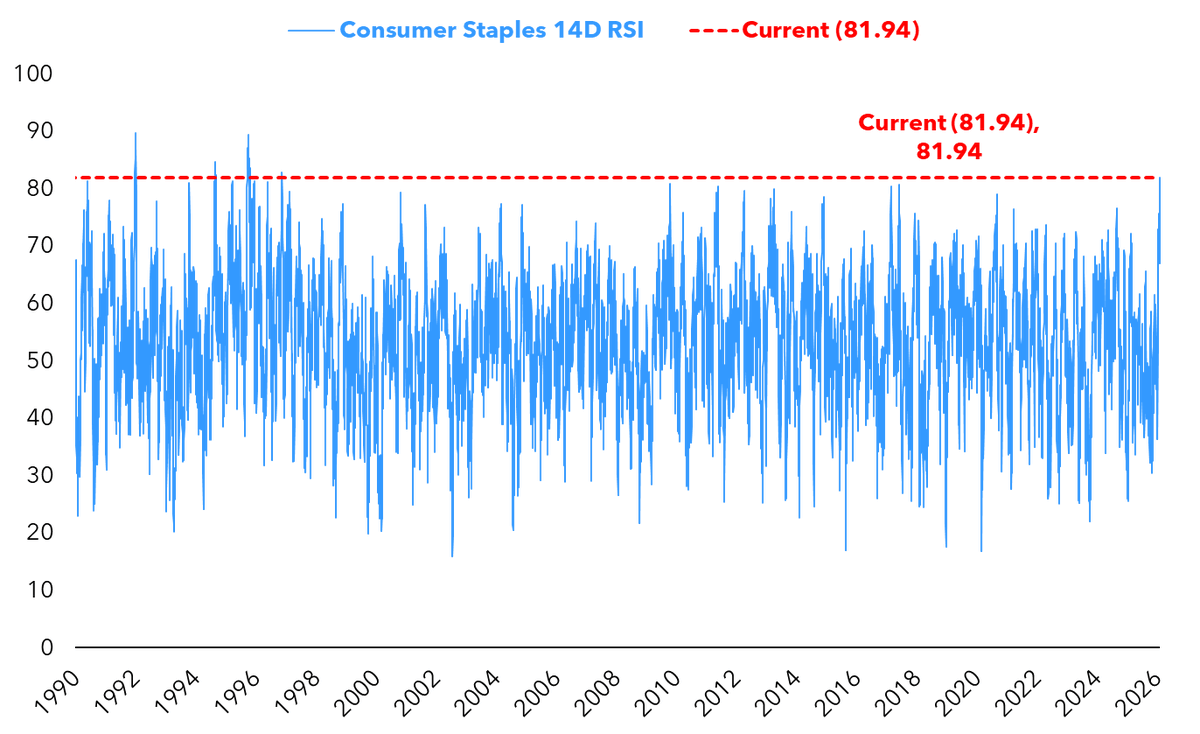

Consumer Staples are the most overbought since Nov, 1996.

That's nearly 30 years.

English