William W. Large retweetledi

William W. Large

1K posts

William W. Large

@large_williamw

Lawyer, Lobbyist, and Advocate for civil justice reform. Interests: Law, Public Policy, and Politics.

Katılım Mart 2017

2.2K Takip Edilen1.5K Takipçiler

William W. Large retweetledi

Leading School Choice Advocate John Kirtley:

"Wilton Simpson understands the path to eliminating generational poverty is through school choice in our K-12 education system. He has worked to ensure access to quality opportunities that serve the needs of Florida’s robust economy by expanding meaningful training in the trades, and inspiring the next generation of farmers by eliminating hurdles for on-campus farming programs. I am proud to endorse Wilton Simpson for Agriculture Commissioner because I know he will continue to deliver for Florida’s students and families."

English

@AGJamesUthmeier @florida_keeper Thank you for your leadership!

English

A grand jury indicted Marcus Anderson for capital murder. Instead of facing the death penalty, Orlando State Attorney Worrell gave him 4 years in prison as a “youthful offender.”

And she keeps handing out sweetheart plea deals to violent criminals. This neglect of duty must end!

English

William W. Large retweetledi

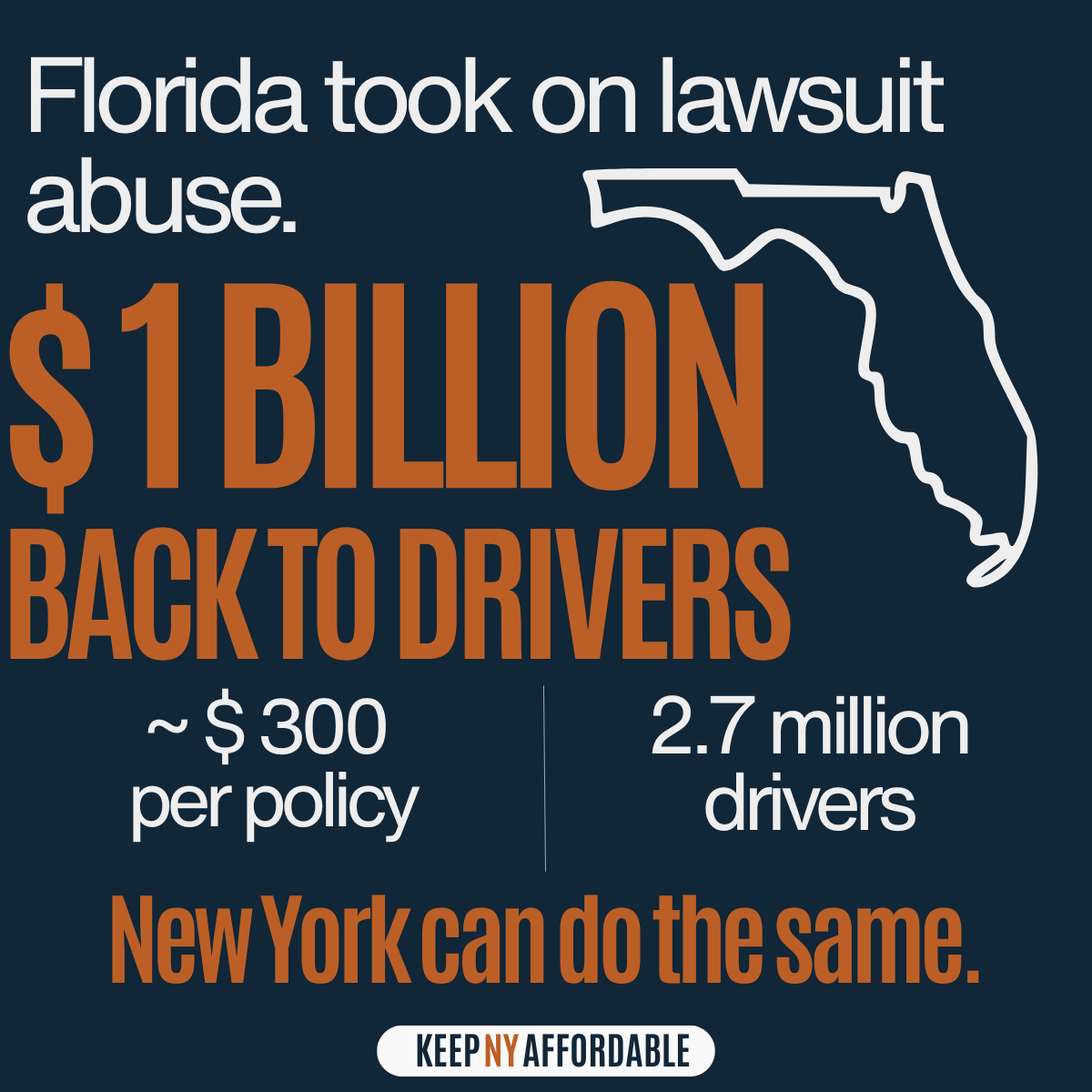

Florida cracked down on lawsuit abuse.

Drivers got nearly $1 billion back.

That is what relief looks like.

English

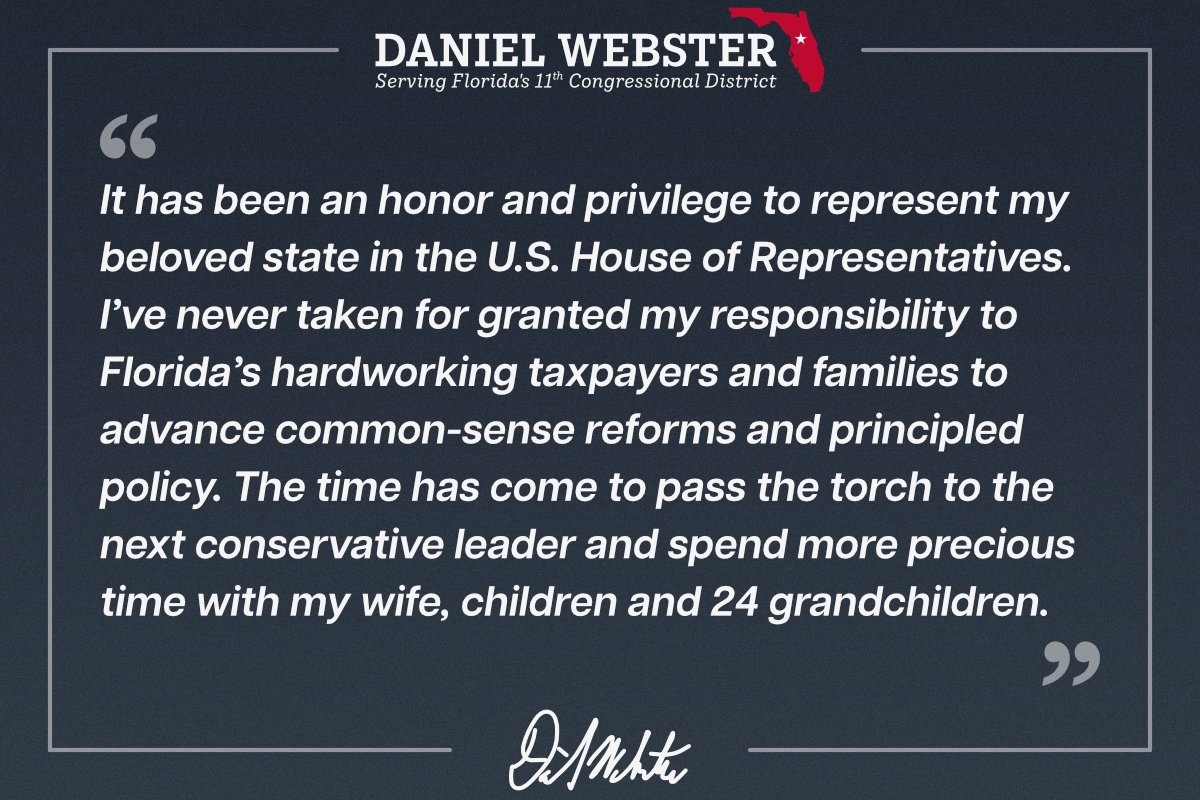

@RepWebster Thank you for your long service to our state. The state is in a better place because of your leadership!

English

After much prayerful consideration and discussion with my beloved wife Sandy, I have decided not to seek re-election to the United States House of Representatives.

To have been part of the development and passage of some most significant legislation in our time is something I will forever treasure. Read my full statement here: webster.house.gov/press-releases…

English

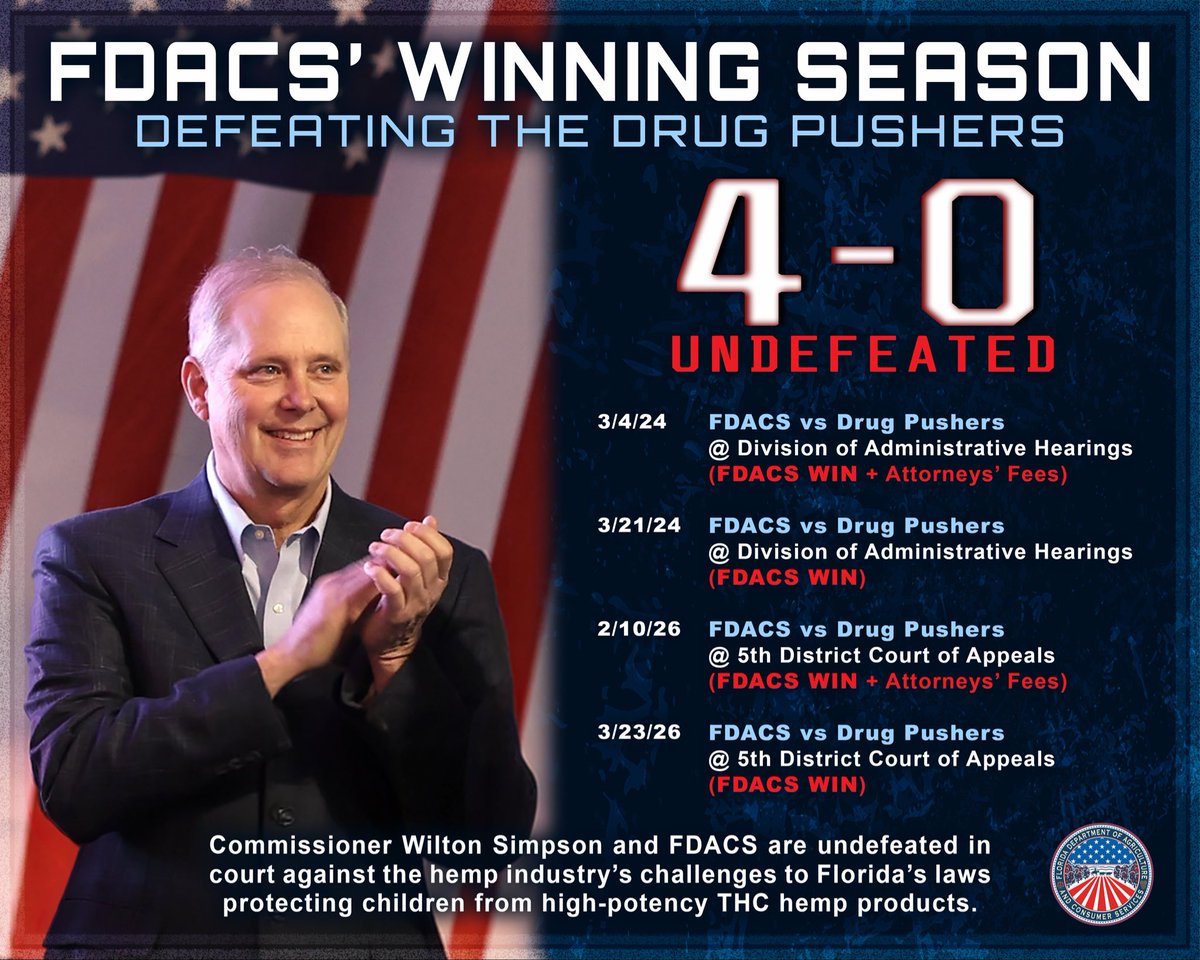

We remain undefeated in court against the hemp industry’s challenges to Florida’s laws protecting children from high-potency THC hemp products.

English

William W. Large retweetledi

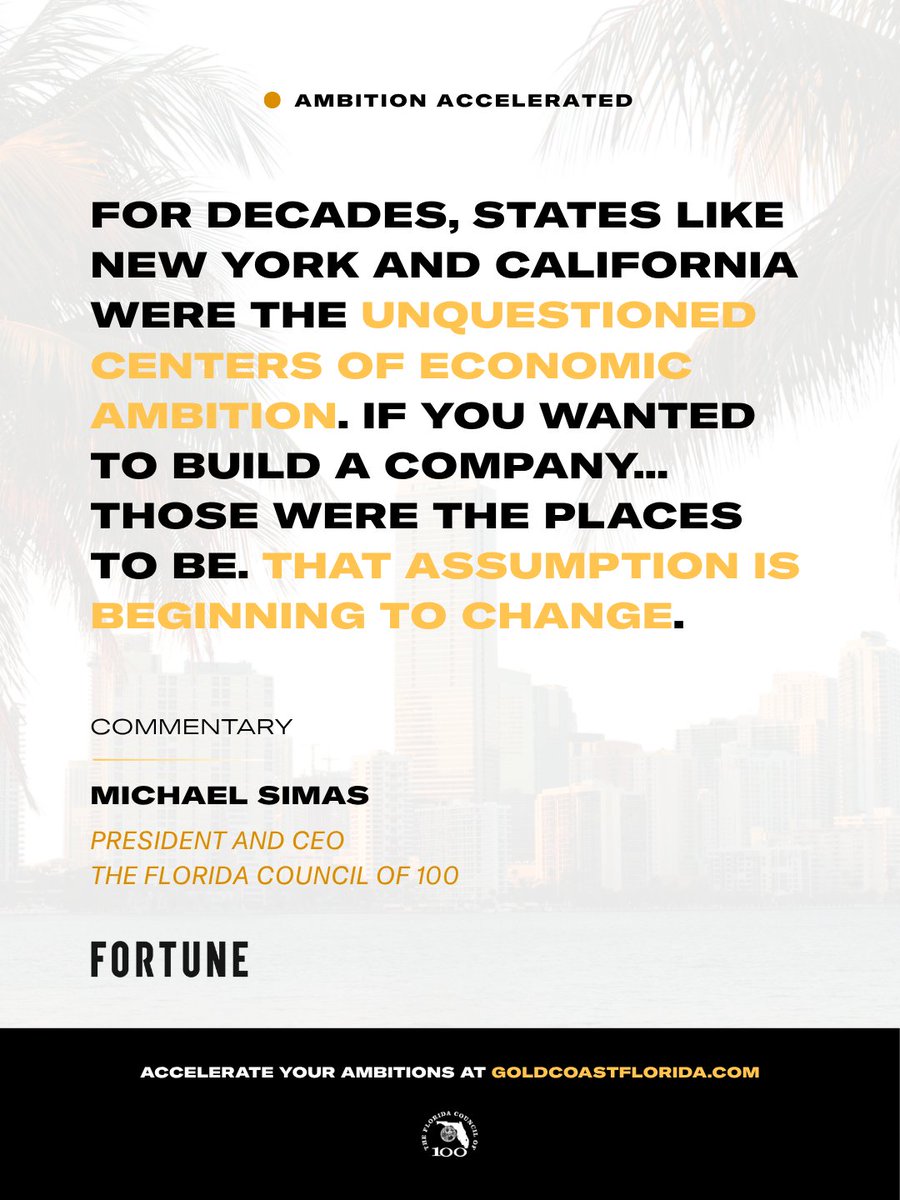

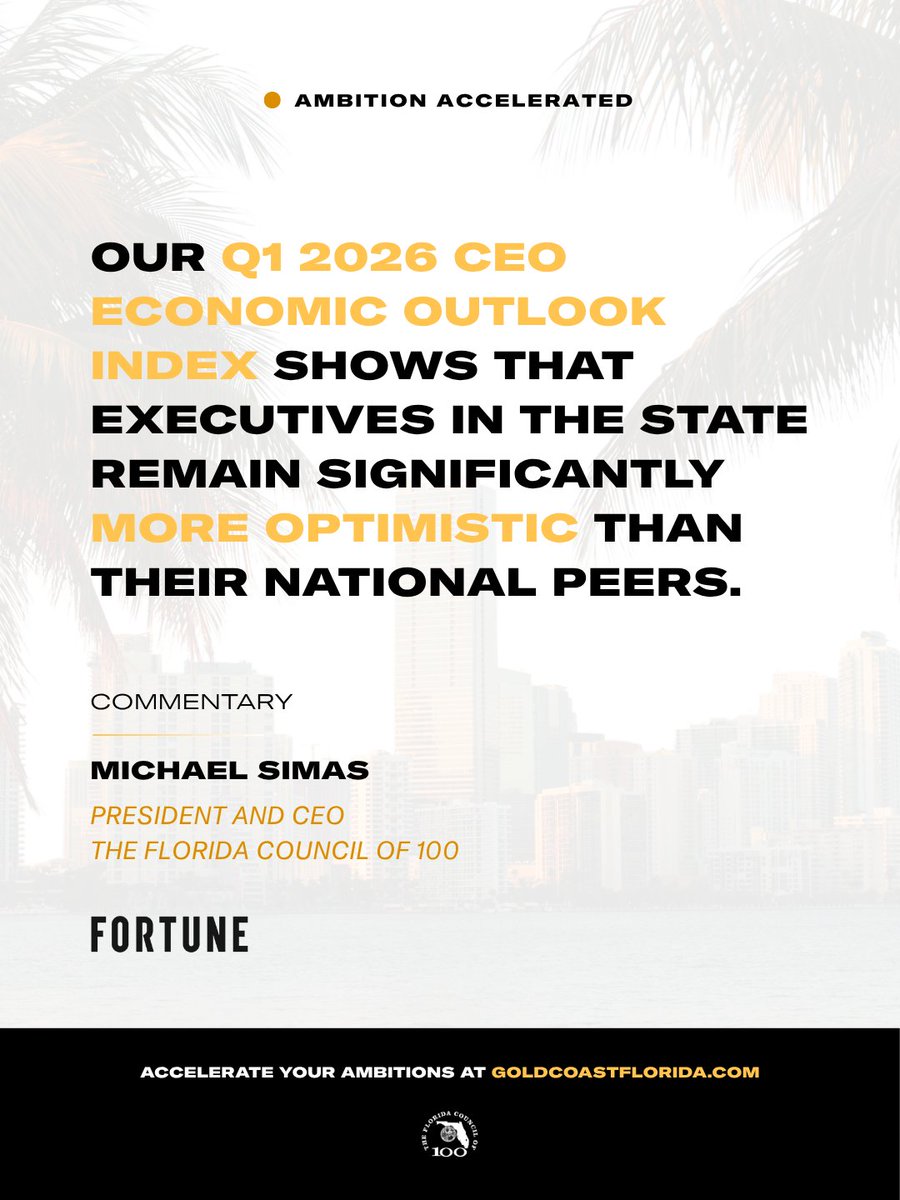

In @FortuneMagazine, FC100 CEO Michael Simas highlights a pivotal shift in business landscapes.

As companies like @apolloglobal and @FCBarcelona move away from traditional markets, Florida emerges as a top choice for investment and growth.

Winning companies choose winning conditions.

Read more: fortune.com/2026/04/02/com…

goldcoastflorida.com

English

William W. Large retweetledi

I am proud to announce the permanent protection of nearly 1,450 acres of working Florida agricultural land through our Rural and Family Lands Protection Program. These easements prevent future development of the land and allow agriculture operations to continue to contribute to Florida’s economy. Since its inception, the department’s Rural and Family Lands Protection Program has permanently preserved approximately 234,000 acres of working agricultural land, with approximately 168,000 acres preserved since I took office.

English

@FLGamingControl Great news! Mark will do a fantastic job!

English

FGCC welcomes Mark Mitchell to the agency. He will serve as the Inspector General for FGCC. Welcome to the FGCC team, Mark!

English

Safe and secure elections are at the heart of what makes us the Free State of Florida and the envy of the nation. I’m proud of the work we’ve done to ensure every legal vote counts!

Florida’s Voice@FLVoiceNews

JUST IN: @GovRonDeSantis credits Florida Agriculture Commissioner @WiltonSimpson for leading the charge in the Senate on the bulk of Florida’s major accomplishments, calling his contributions "really, really significant." "Thanks to the commissioner and thanks for what he did when he was the leader of the Florida Senate to get the bulk of what we've done."

English

William W. Large retweetledi

The Florida property insurance market is shifting. @Scott_Maxwell tells one version of the story…but he’s missing the plot. If you actually look at the data, a very different picture emerges. 👇

Jeff Brandes@JeffreyBrandes

Scott, this argument ignores both the data and basic economics. Start with Citizens. It peaked at about 1.41 million policies in 2023. Today it’s roughly 330,000 to 360,000. That’s a 75 percent shift. Markets do not move like that unless private capital is returning and taking risk. Since the reforms, about 15 new insurers have entered Florida with more than $500 million in new surplus. That is new capacity, competition, and exactly what we said the market needed. Litigation is down materially, on the order of 40 to 60 percent depending on the dataset. That was one of the core cost drivers, and it is finally moving in the right direction. The radical thing the legislature implemented was joining 49 other states that require everyone to pay their own attorneys fees. Shocking! Now add the piece people keep ignoring: 2024 was an active hurricane year for Florida, with multiple landfalls driving significant claims. Then 2025 had no landfalls, giving the market a rare chance to stabilize. That matters and I why we didn’t see this change in earlier 2025. In addition, Replacement costs for Florida homes jumped roughly 30 to 40 percent from 2022 to 2026, driven by inflation, labor shortages, and higher material costs, tariffs, and that increase is now flattening but not reversing. Florida still faces the fact that it gets hit 1.8x per year by a named storm. You cannot have all of those inputs moving up and expect premiums to instantly fall. That is not how insurance works. That is not how math works. What the reforms did was stop the spiral. Reinsurance which is 40% of premium is easing. New carriers have entered the market. Citizens shrunk rapidly. Rate filings are flattening and, in many cases, coming down. This crisis was built over more than five years. The reforms are not even three years old. You don’t walk five years into the jungle and expect to change course and be out in two. But for the first time in years, we are actually moving in the right direction. Perfect no, progress absolutely

English

There are fights worth having now, and for future generations of Floridians. I’m proud of the work we’ve done to make Florida the first state in the nation to outlaw untested, synthetic "cultivated meat" products, and thrilled that a Federal Court has upheld this law.

flvoicenews.com/federal-court-…

English

@WiltonSimpson @alexhaleygr Thank you for your leadership!

English

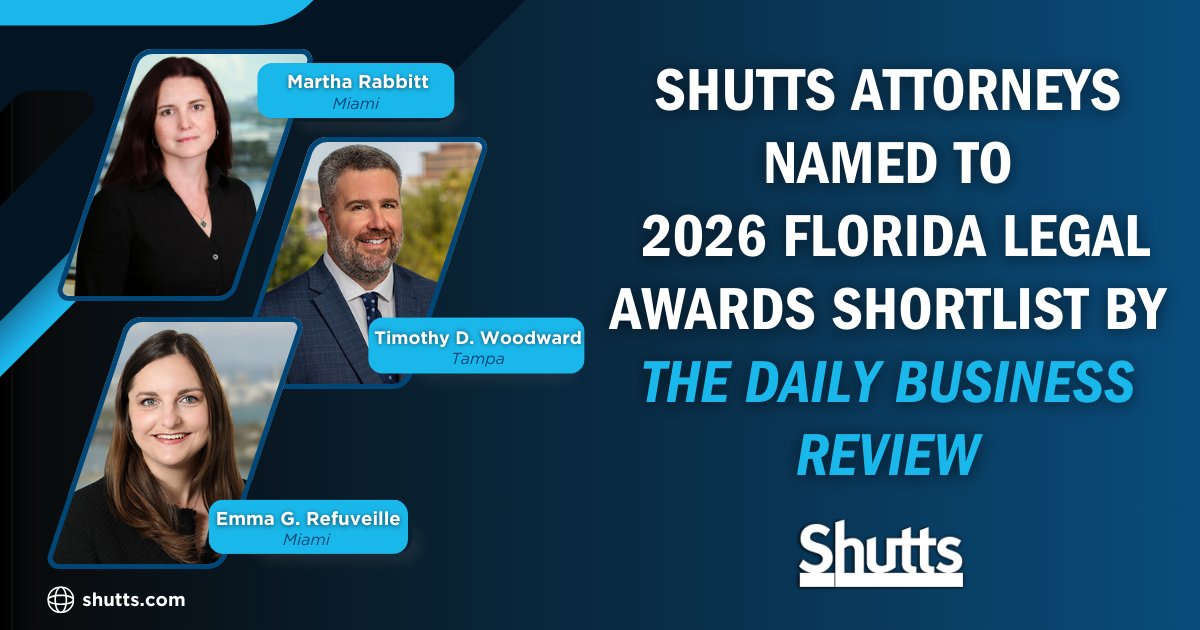

#Shutts & Bowen LLP is proud to announce that three of its attorneys have been named to the 2026 Florida Legal Awards Shortlist by the @dbreview.

shutts.com/news-Shutts-Bo…

English

@RonDeSantis @BryanDGriffin Thank you for your leadership!

English

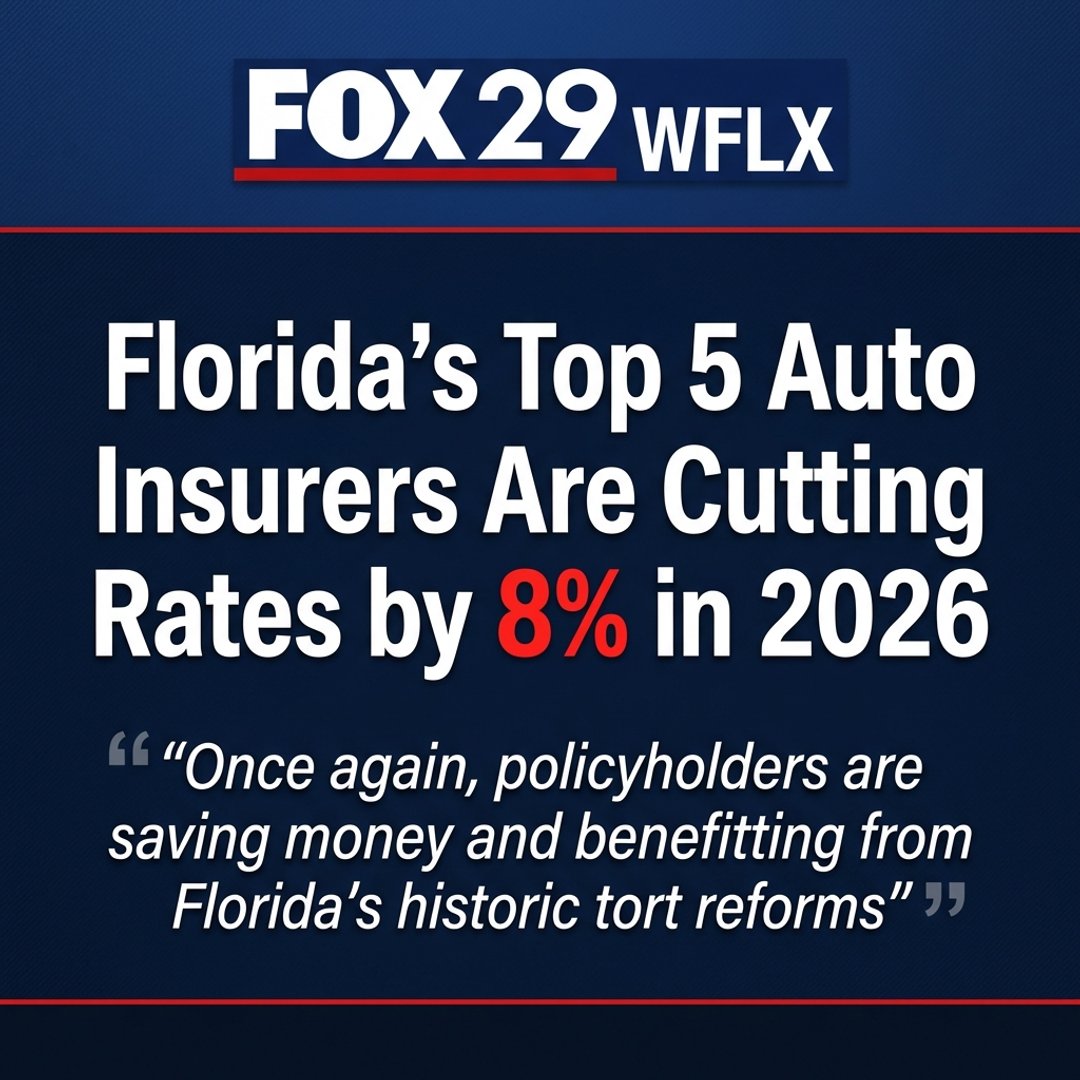

William W. Large retweetledi

Good to see more filings for rate decreases in auto insurance premiums due to FL’s reforms.

One group is averaging a 16.5% rate reduction.

Florida Office of Insurance Regulation@FLOIR_comm

Commissioner Yaworsky Announces More Significant Auto Rate Decreases for Florida’s Top 5 Auto Insurance Groups 🚗🚗 Commissioner Yaworsky: “The historic legislative reforms continue to drive auto insurance rates down—with nearly 80% of Florida’s auto policyholders seeing lower rates for 2026. Florida’s top five auto writers are already indicating an -8% rate change for 2026, with one group even indicating an -16.5% rate change. This is great news, and we anticipate this trend to continue for the auto market.” floir.gov/newsroom/archi…

English

William W. Large retweetledi

BIG NEWS!

"Florida's top 5 auto insurers are cutting rates by 8% in 2026" following historic reforms to crack down on lawsuit abuse.

Read more: wflx.com/2026/03/05/flo…

English

@FloridaC100 @eMergeAmericas Great news! Melissa is a respected leader in the technology and innovation space.

English

Please join us in welcoming Melissa Medina to The Florida Council of 100 Board of Directors.

As Co-Founder and CEO of @eMergeAmericas, Melissa has played a defining role in positioning Florida as a global hub for technology and innovation.

Her insight and global connectivity in this space will further strengthen the Council’s efforts to support resilient, high-growth industries across the state.

English

@WiltonSimpson @ChaseBrannanFL Thank you for your leadership!

English

I am proud to announce another win for Florida through our Rural and Family Lands Protection Program today. We are permanently protecting nearly 2,600 acres of productive timberland in Baker and Gilchrist Counties to ensure it stays in private hands and continues working for Florida families. These easements protect private property rights, keep government from owning and managing more land, and ensure Florida families can continue producing the food, fiber, wildlife habitat, and economic opportunity that fuel our state.

Since its inception, the department’s Rural and Family Lands Protection Program has permanently preserved approximately 230,000 acres of working agricultural land, with approximately 165,000 acres preserved since I became Ag Commissioner.

English

William W. Large retweetledi

Florida drivers are beginning to see the benefits of recent legal reforms. Highlighted by @GovRonDeSantis, State Farm plans to return an average of $173 per vehicle through dividends, complementing earlier discounts and rate reductions from @progressive, @USAA, and @AAAnews.

Ron DeSantis@GovRonDeSantis

Due to Florida’s legislative reforms, State Farm has announced a major dividend that will yield FL policyholders an average savings of $173 per vehicle on auto insurance. This is on the heels of rebates and/or rate decreases by Progressive, USAA and AAA — all due to the FL reforms.

English