@jrouldz @stevenfiorillo Bad ideas need to be called out as such. Debate is the only way

English

PhilDozer

435 posts

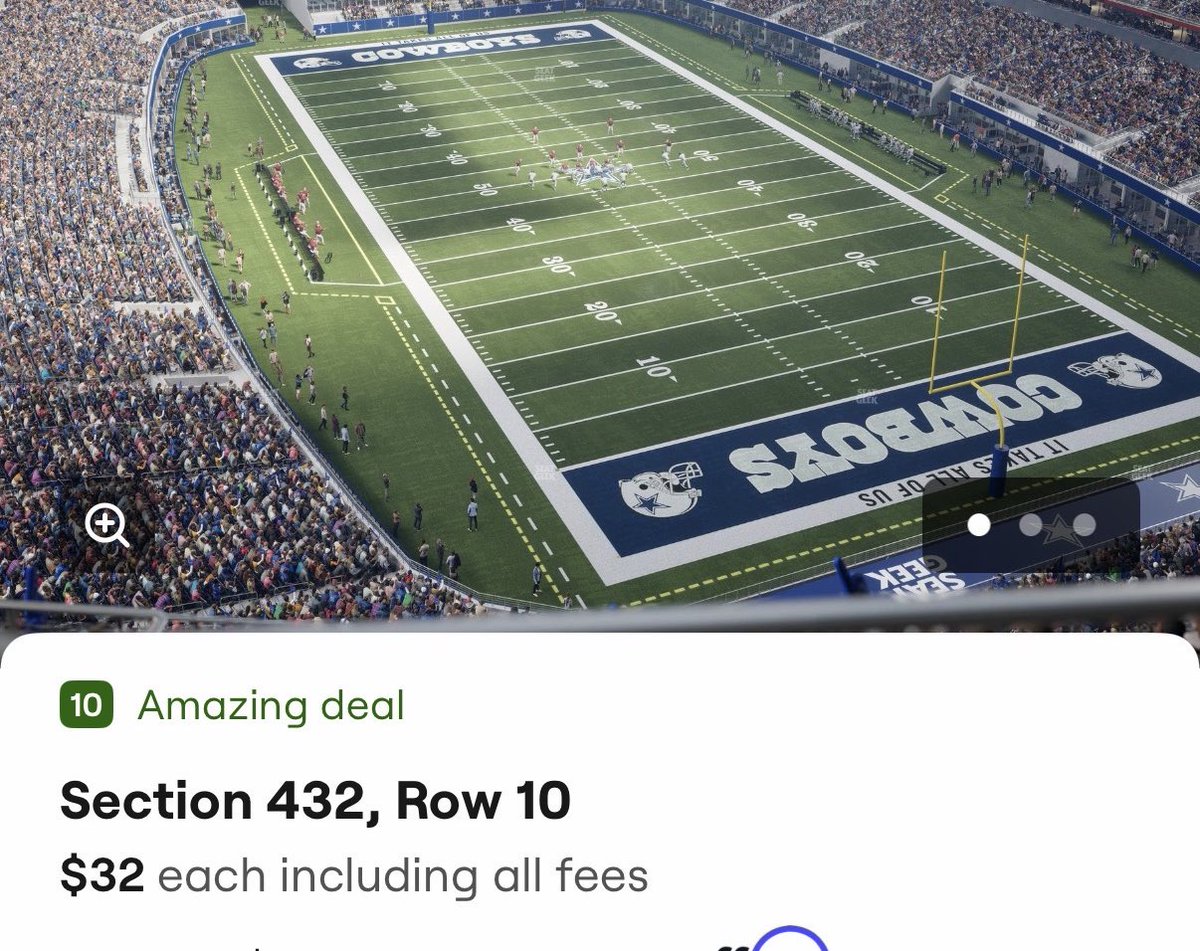

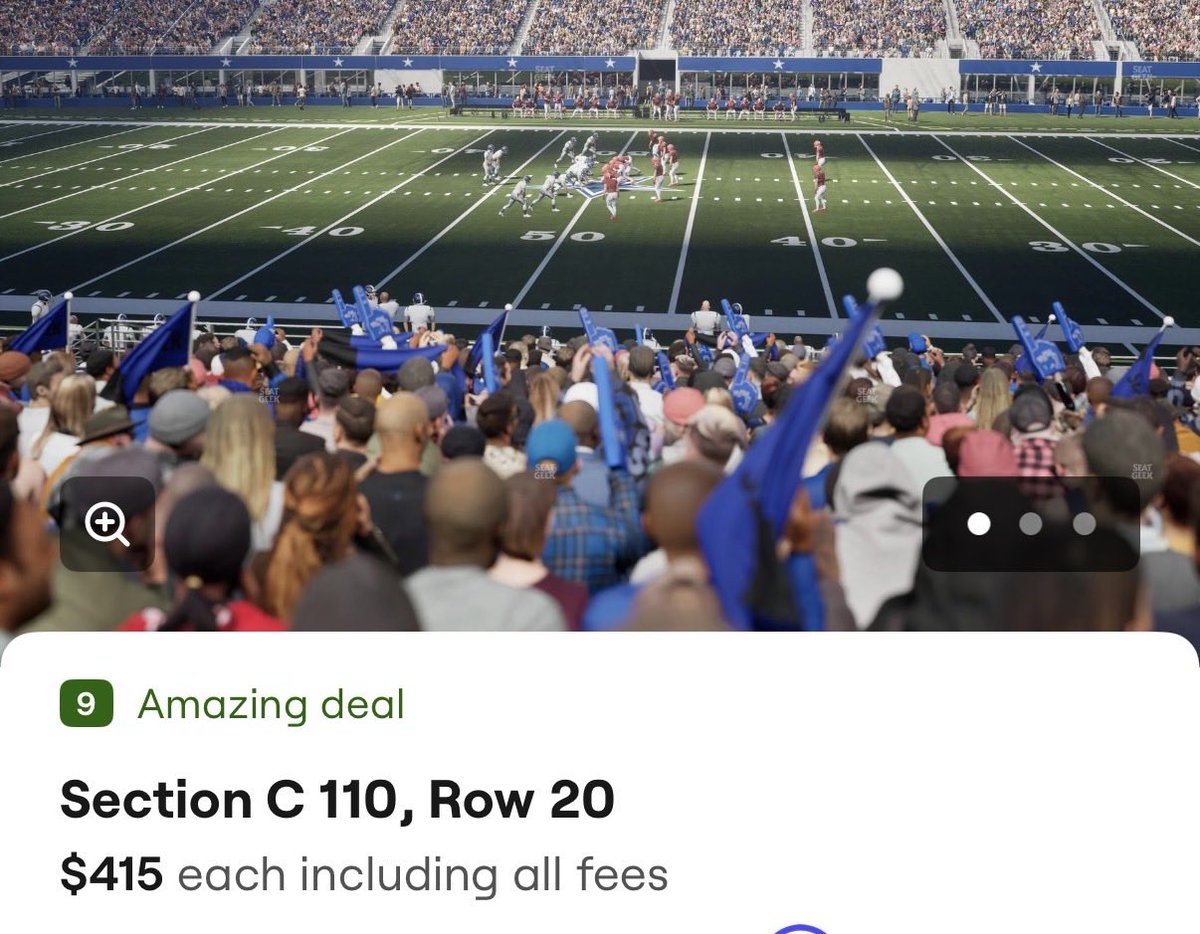

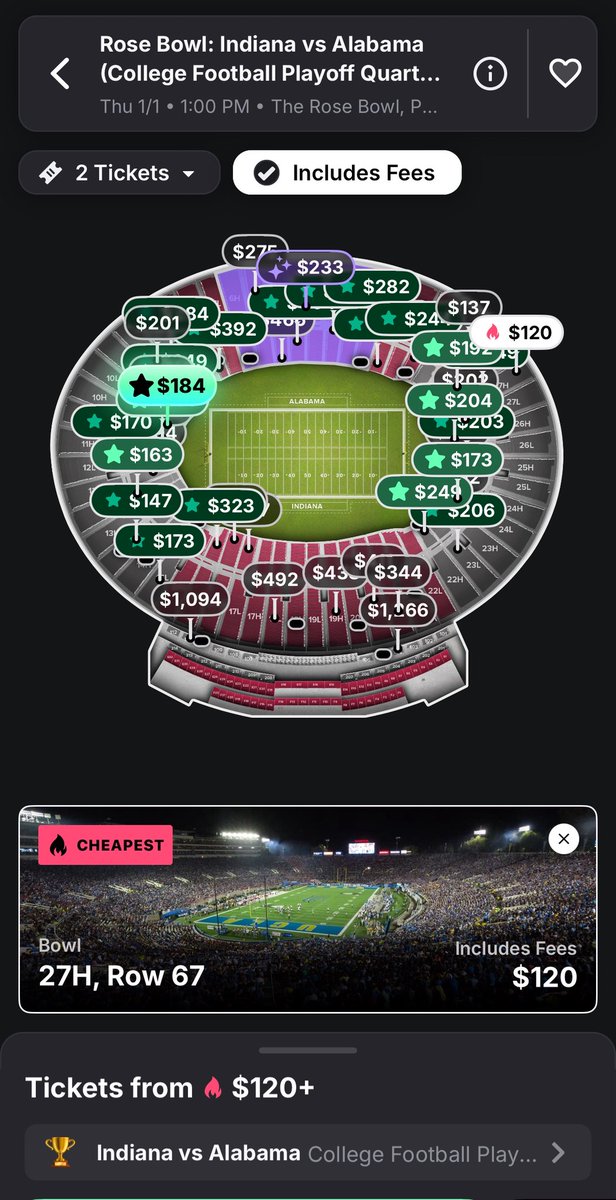

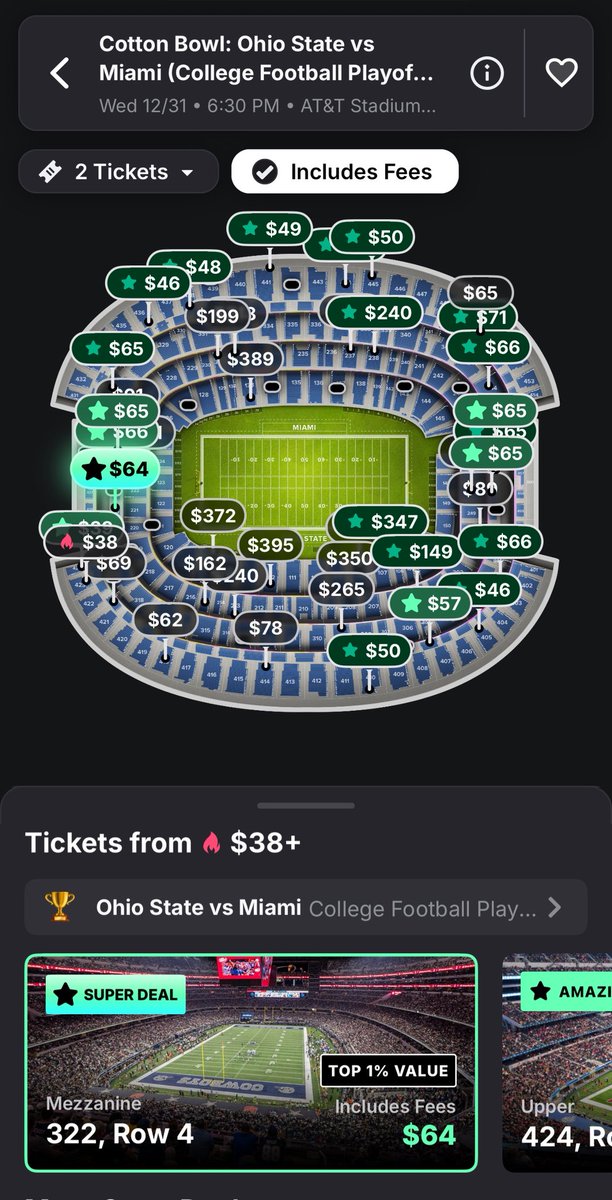

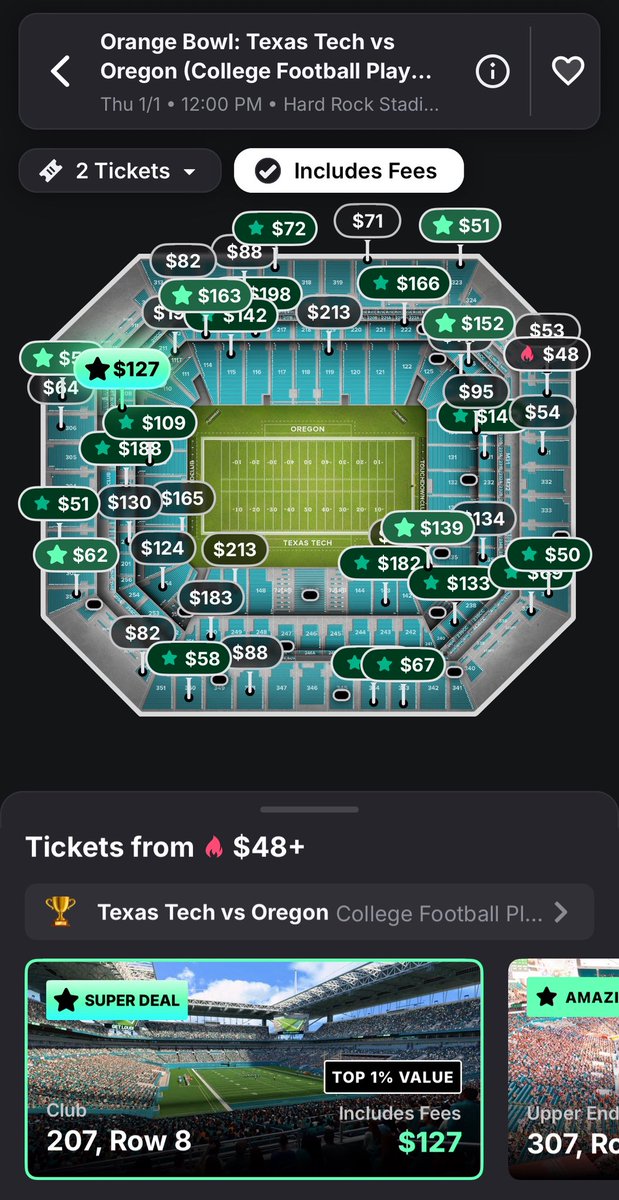

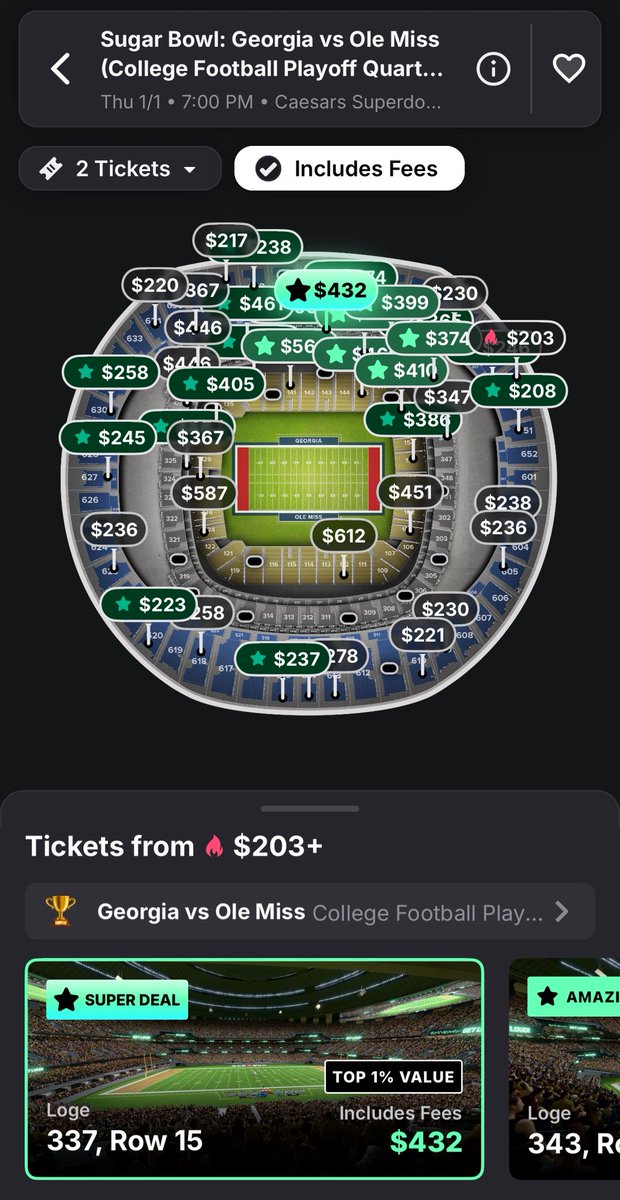

Ticket market for the new year CFP games is abysmal $120 get in for the Rose Bowl is unprecedented + the Cotton and Orange bowl likely will not sell out If this isnt proof we need on campus QF games idk what is. 3 games in 3 weeks is way too much travel to put on a fanbase

The "California Effect" is when you read on social media that a place is "hell on earth," and then you go visit it and wonder why you don't live there.

JUST IN: Large numbers of users are allegedly rushing to close accounts at JP Morgan following a premeditated attack on $MSTR shareholders.