ทวีตที่ปักหมุด

I was one of the earliest people at @RedotPay

Let me explain exactly why you've never heard of it.

RedotPay didn't build for the English-speaking crypto Twitter crowd.

It built for everyone else.

Arabic. Hindi. Spanish. Bahasa. Tagalog.

Native content, native communities, native trust.

You won't find it in your feed because it was never meant for your feed.

The users aren't only crypto traders.

They're the unbanked. The underbanked.

People whose currencies are devaluing faster than they can save.

Crypto Twitter is loud. But it's a small room.

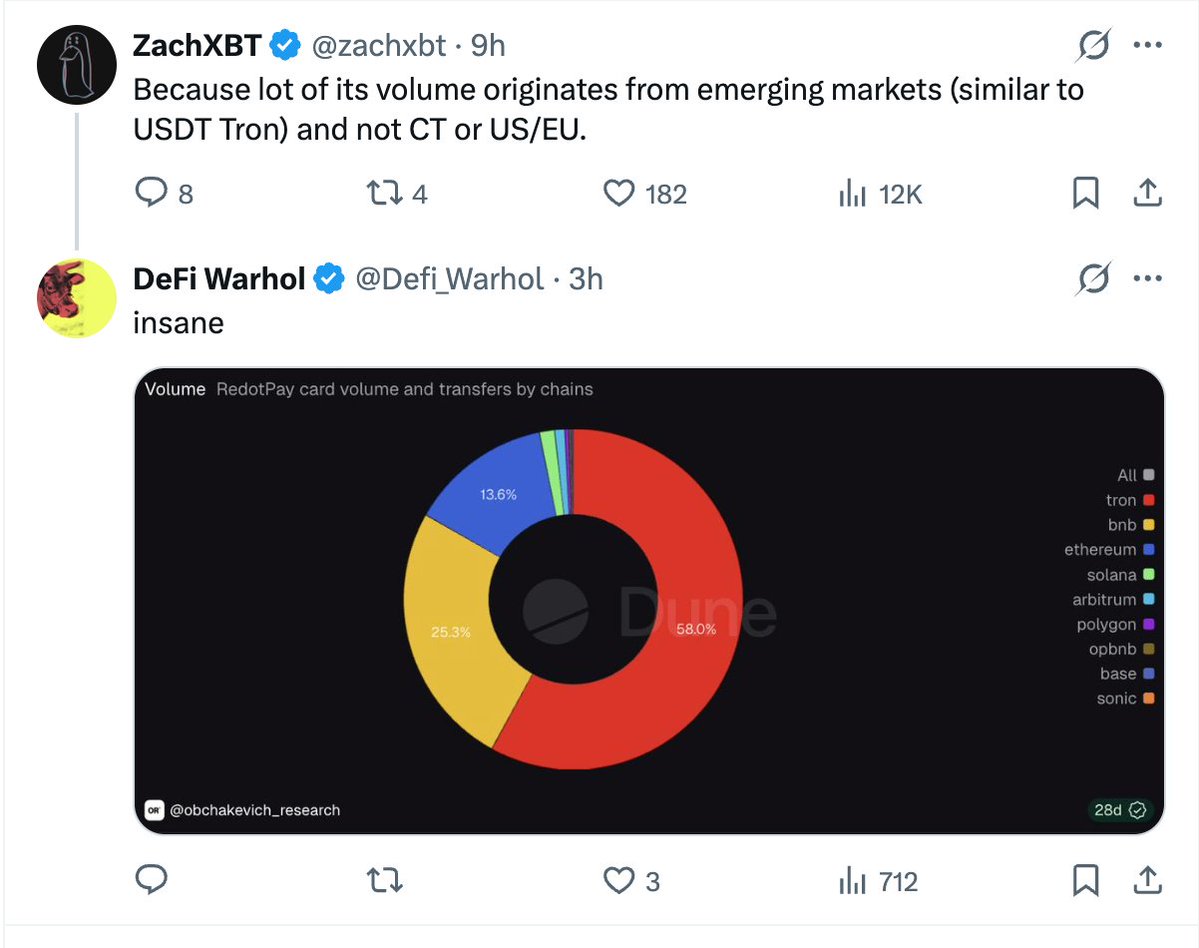

The real volume lives on Facebook groups in Lagos, TikTok reels in Manila, Instagram in Cairo.

Hundreds of thousands of people showing their RedotPay card working at a local store, paying a bill, sending money home.

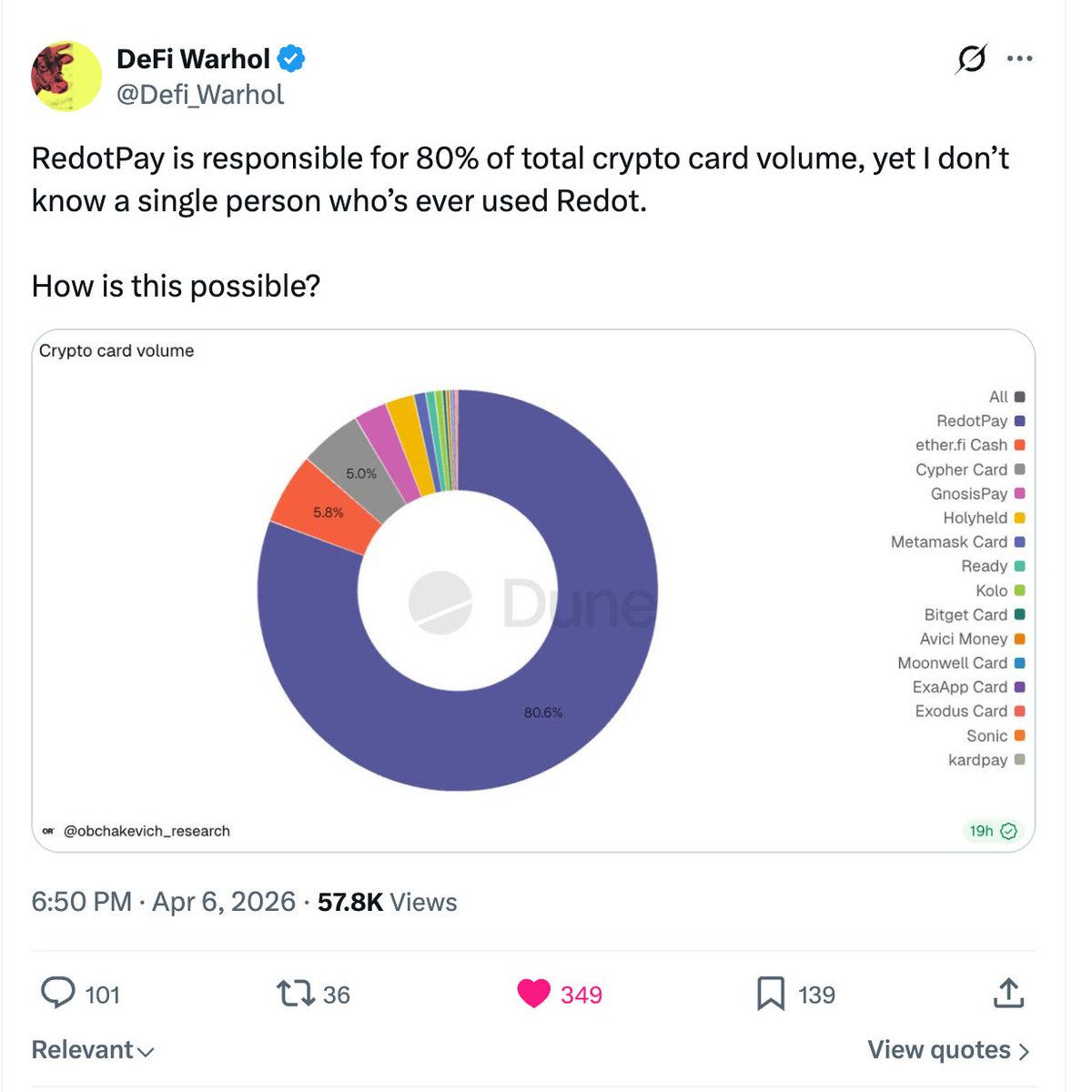

80% of crypto card volume didn't come from people who know what a DEX is.

It came from people who just needed a better way to pay financially.

That's the market nobody was watching.

RedotPay was.

DeFi Warhol@Defi_Warhol

RedotPay is responsible for 80% of total crypto card volume, yet I don’t know a single person who’s ever used Redot. How is this possible?

English