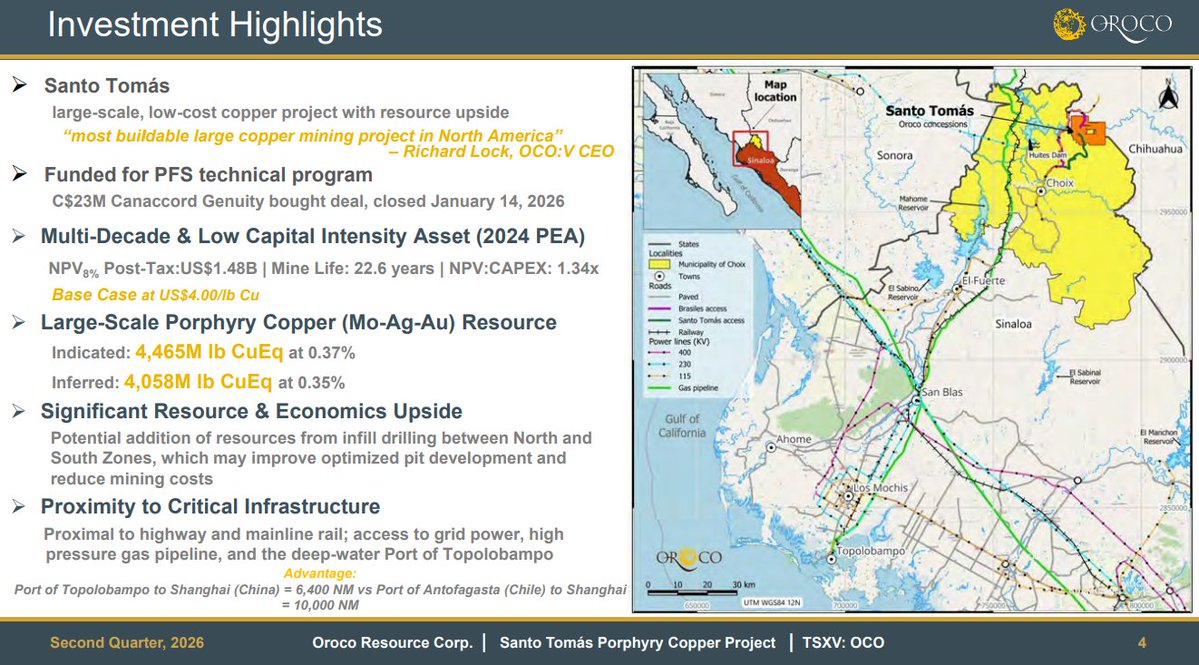

@the_analyst_24 And that doesn’t include the “harder to get to” resource that bumps these numbers by a lot!

Tons of added upside in Brassiles and outside the south zone

OH AND THEY HAVE VAINILLA CONCESSION NOW

English

A

338 posts

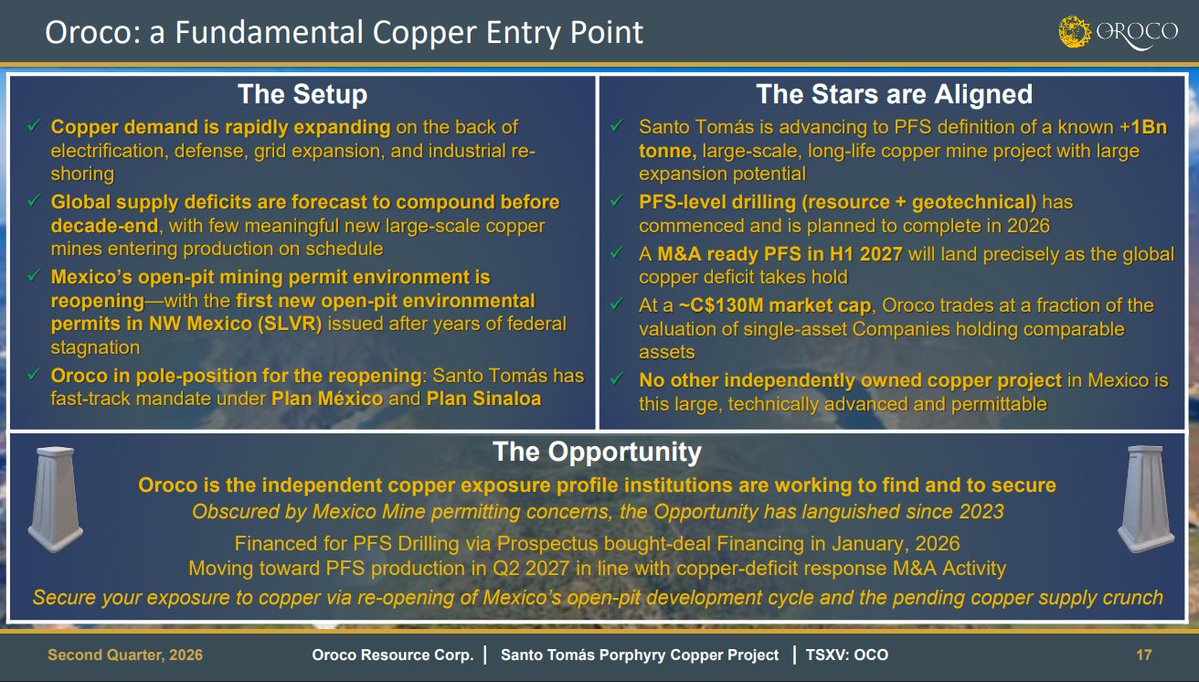

Specifically had it written up as headline catalyst coming last night lollll

Copper is no longer just a metal. It’s becoming the bottleneck of electrification and the market isn’t ready for it. “One of the key levers to address the copper supply challenge is increased investment upstream.” - Rosemary Katz, Senior Associate, Metals and Mining, BloombergNEF Bringing new copper supply forward will define the next phase of the market. In a tightening environment, the focus is shifting to projects that are not only large, but can be advanced. 🎥 Watch the full video: about.bnef.com/insights/commo… $OCO $ORRCF #Copper #EnergyTransition #Mining

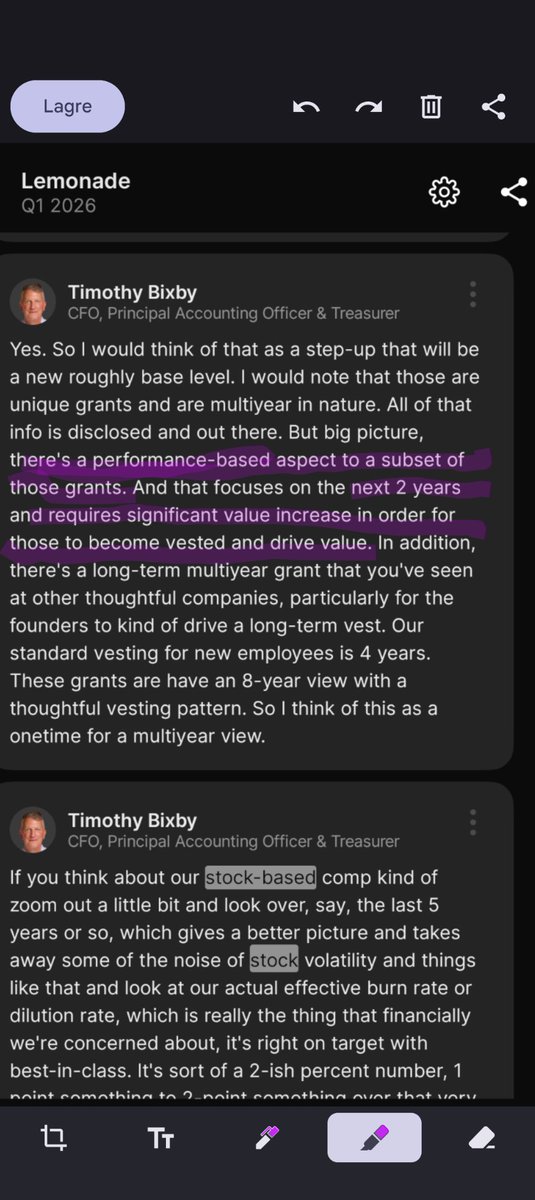

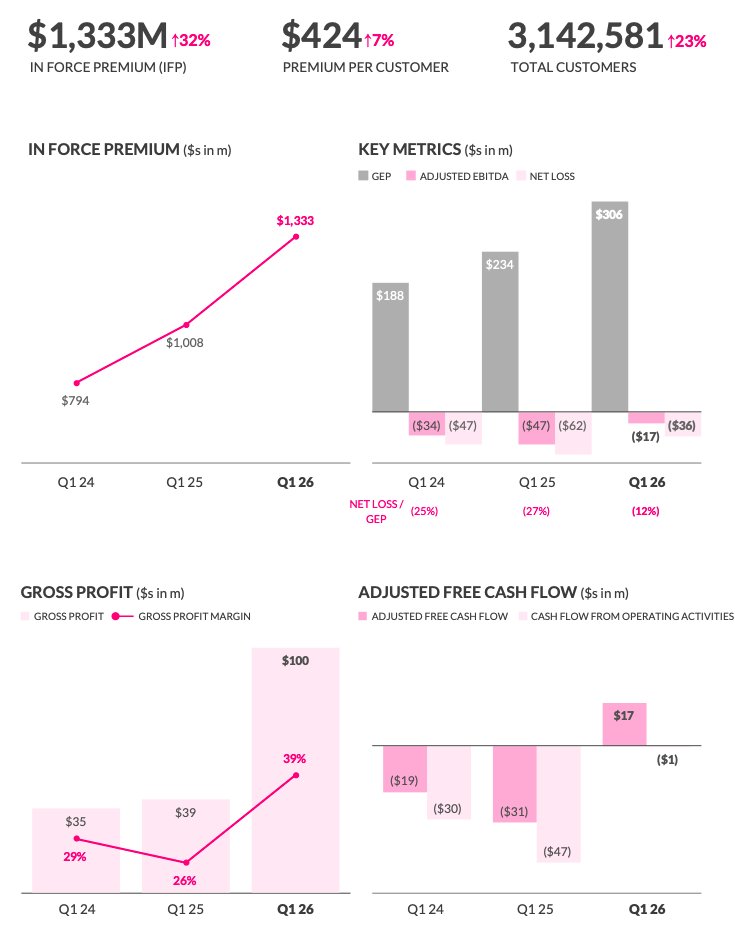

At the November 2024 $LMND Investor Day, CFO Tim Bixby conceptualized an NPV per share of $90+ Using Tim's same mental model, based on 2026 estimates, we get an NPV of $115+ Buying shares in the $60s today is significantly less than the 2024 fair value per share and dramatically less than the 2026 fair value per share ✅ Napkin Math: FY25 GEP guidance is around $1.047B, and @PaperBagInvest estimates FY26 GEP to be around $1.380B (subscribe to his Patreon for full access to the model) So, take $1.38B grown at 31% and apply a 12% ratio of Ajd. EBITDA and we get...... GEP year 7 ≈ 1.38B×(1.31)^7 ≈ $9.2B Apply 12% Adj. EBITDA Margin, 9.18B×12% ≈ $1.10B Tim’s original $90+ implied something around a 15x multiple on EBITDA, please correct me if you think otherwise. Market cap 7 years out = 1.10B×15 = $16.5B Discount 7 years at 10% (might be too low of a rate) NPV ≈ $8.5B or $115–120/share Reminders: EBITDA is expected to flip positive this year. CAGR has been accelerating and management hints at growth in the low 30s not up to and stopping at 30%. This could mean anywhere between 31-33% IMO. At investor day, management said that if total earned premium doubles from $1B to $2B, cash flow - adjusted FCF - will 20x from $15M to $285M. That is EXTREME operating leverage. In fall 2022 LMND’s loss ratios were 94%. In fall 2024 they were 62%, while the trailing twelve months (“TTM”) loss ratio was 67%. Cash flow break even was originally guided for 2025. LMND achieved it a year ahead of schedule in 2024. FY 2024 was cashflow positive as a whole. IRR with synthetic agent funding is 112% Over the past few years, $LMND kept up with their guidance and even out performed their guidance despite a generational inflation bout that rocked the insurance industry.

The biggest issue I see with $LMND is they are driving bigger growth simply by taking on more and more risk. Typically insurance companies reinsure the underwriting they do with other insurance companies. This is called "reinsurance". Up till 2025, Lemonade reinsured most of their underwriting making them a very safe play as all their partners bared the risk. Now, they are slashing the amount of reinsurance which means they make more revenues, but at the cost of taking on far more risk. This really concerns me vs a company like $LIFE which still manages to grow over 50% and take no risk as it uses all agents and partners to take the risk.

98% of all new lines of code at $LMND written by Ai. Let that sink in. Most companies are pushing to 25-30% - the processes, the policies, the automation required to operate at 98% is mind blowing! Full post from Adina on LinkedIn here linkedin.com/pulse/when-mis…