CavaSoTasty

151 posts

CavaSoTasty

@CavaSoTasty

Slop bowls & Sports @Cavasotasty on PM

Katılım Mayıs 2026

52 Takip Edilen31 Takipçiler

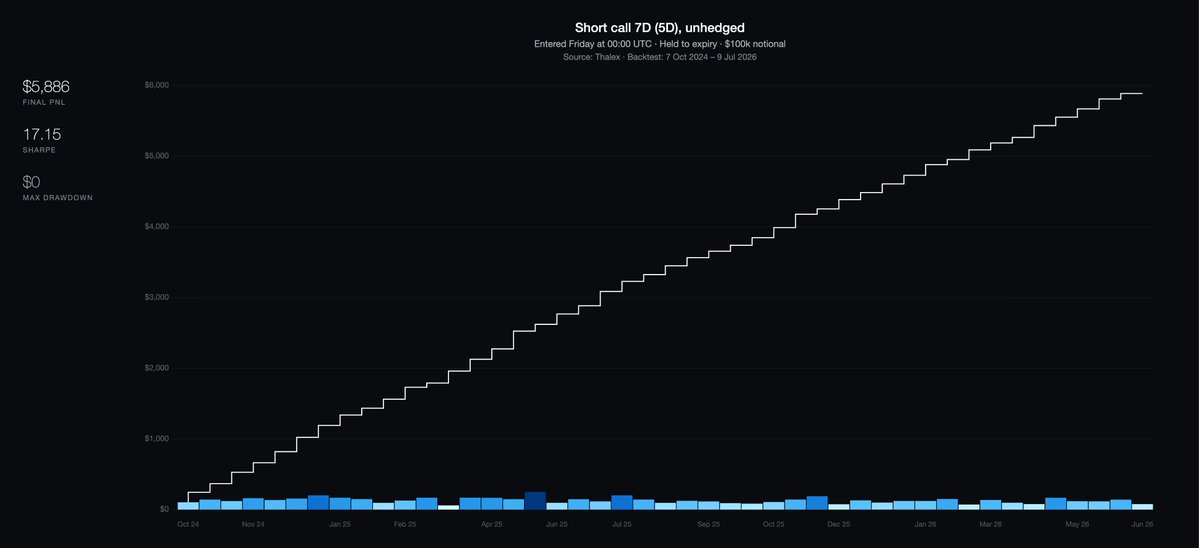

Our quants have identified a 17 sharpe strategy using options.

Backtest shows a 100% hit rate.

Leverage is advised.

Actually no, it's not.

This is an example of data mining. This backtests sells five-delta 7DTE calls each week. This apparently had a perfect zero-losses win streak if you sold every Friday at midnight, and held for a week until expiration.

But (a) this is an example of data mining. If you were to vary the time of day parameter, you'll get wildly different results. And b) the logical fallacy here is thinking you can backtest a tail risk selling strategy where the true loss rate and loss size are are nearly impossible to quantify.

English

Open weight models are ~15 months behind proprietary models

Kimi.ai@Kimi_Moonshot

Meet Kimi K3

English

@Hoodganster82 @HormuzLetter Yes but that’s also the only reason anyone bought twitter’s fast feed in 2017. Same thing!

English

@CavaSoTasty @HormuzLetter Its not as if anyone would pay for this to gain early acess to any account besides the president/truth social owner's one

English

BREAKING: Trump Media to sell "faster millisecond access" to Trump's Truth Social posts starting August 1, letting traders, hedge funds, and high-frequency trading firms pay for real-time millisecond access to Trump's Truth Social posts.

This comes a day after Iran calculated $9 billion in profits from market manipulation by Kushner and Witkoff through insider access to Iran negotiations.

English

@TheGreekTrader Hate to break it to you but twitter has been selling the exact same fast feeds for over a decade. The fastest cost $250k/month. This is a completely fair step for truth social as a social media company (coming from someone who agrees trump is a scammer)

English

Banks and big trading firms will be getting Trump's posts on Truth Social before anyone else.

Life is unfair.

English

@Autonomous_Chad Most important thing is having a retail stream, which they don’t have. Otherwise it’ll die.

English

Hyperliquid's HIP-4 is already dead.

Their Word Cup champion market made a pitiful 0.69% of Polymarket's volume

World Cup Winner (Polymarket) -> $4.26B volume

World Cup Winner (Kalshi) -> $1.2B volume

World Cup Winner (Hyperliquid) -> $29M volume ...

This is not what we expected from the "Polymarket Killer".

And this looks even worse when you consider that @polymarket and @kalshi both list thousands of markets while HIP-4 lists only 10 (ten).

Yet they can't even scratch 1% marketshare on the few markets that they have

This looks extremely bearish for their platform.

They may already have missed their critical take off opportunity with the World Cup.

They absolutely need to fix these 3 flaws if they want to survive :

1 - Prediction Market UI looks like trash (not retail friendly)

2 - Only validators can propose new markets

3 - No coherent liquidity incentive program

if they don't do it quickly it will be @hyperliquidx first failed product since their launch

English

Class, this is why we don’t accept everything we read on X! This 5d call selling strategy got absolutely rekt in April 2025 as volatility spiked and then the market ripped 10% in an afternoon, yet that doesn’t even show up in the picture.

Do your own research! And fact check what your AI assistant tells you!

Hendrik Ghys@minus1_12

If you grid search for high Sharpe vol strategies, you will inevitably end up at tail selling. The stairway to heaven P&L curve below is the result of selling 5-delta calls every week, no delta-hedging. Over 91 weeks, 2 losses. Let's critique this. First obvious point, you don't collect enough premium to make this strategy that compelling. Second obvious point, Sharpe ratio is not a good measure for a negative skew, high win rate strategy. But let's try to make a more fundamental point about P&L feedback - how could you know whether this strategy makes money in the long run? You have very few data points in the tail. At this rate, it would take 9 years to collect 10 samples, and even then do you have an idea of the potential loss size? Then there is uncertainty about the true loss rate. Maybe 2.2% was a lucky draw. GPT tells me that the confidence interval would be 0.4% - 7.7%, assuming i.i.d weeks, with higher loss rates if there's autocorrelation. This is where I like selling straddles. They feel much more risky, but they are much simpler to reason about and the feedback you get is much more honest and direct.

English

Recently I've been good at using this trading strategy called buy low sell high👍

English

@Autonomous_Chad “Sheldon H. Jacobson, Ph.D., is a professor of Computer Science at the University of Illinois Urbana-Champaign.” Actually so embarrassing for his department and school 😂

English

Another slop hit piece against Prediction Markets.

Straight into the trash.

Mainstream journalists just can't understand that prediction markets are NOT SportsBooks

1) "Polymarket and Kalshi are setting odds as to capture insider informations"

I don't know what this is supposed to mean in the best of case.

But Polymarket is not setting any odds anyway, the market does. They have no control over that.

2) "Prediction markets could incur financial losses if they let insiders win"

Prediction markets do not bet against their users. This is what SportsBooks do.

Prediction markets are a neutral platforms where users bet against other users. They do not care who loses or win a bet.

3) "Prediction markets give opportunities for world leaders to insider trade"

True but they didn't wait on Prediction Markets and they are not even good for that.

Every time Trump announced a ceasefire with Iran, we saw Billion dollars oil future trades hit the market a few minute before, making hundred of millions in profit.

Try to place a billion dollar order on Geopolitical prediction markets with a few hundred thousands of liquidity.

For some reason Mainstream media seems to absolutely hate prediction markets and churn out these trash hit pieces on the regular.

I would advise @polymarket to put a few dollars from their marketing budget into educating the wider public. Because this may seem very retarded to us, but so are the people reading it, and they vote.

TheHillOpinion@TheHillOpinion

The dark side of prediction markets is getting even darker tinyurl.com/2s4kewb6

English

@TheHillOpinion “Sheldon H. Jacobson, Ph.D., is a professor of Computer Science at the University of Illinois Urbana-Champaign.” Super embarrassing for UIUC that this guy would go spout embarrassingly false opinions

English

The dark side of prediction markets is getting even darker tinyurl.com/2s4kewb6

English

@PeterSchiff I mean, this is exactly what twitter does and has done since before the first trump presidency. They made a ton selling realtime feeds to trading firms

English

In the latest Trump grift, Truth Social will now sell faster access to Trump’s market-moving posts to institutional investors willing to pay for it. This is yet another example of Trump's unprecedented exploitation of the presidency for personal financial gain.

English

Election integrity is currently the most likely topic of Trump’s Address to the Nation tomorrow, with the SAVE America Act at 92%.

There hasn’t been much news about the speech yet, but Trump has been hyping it as “big news,” suggesting it may be more substantive than his typical “we are the hottest country” remarks.

Jennifer Jacobs@JenniferJJacobs

The @PressSec isn't revealing what Trump will say Thursday night, saying: "The truth is, nobody knows yet what President Trump will ultimately say, which is why everyone should tune in.”

English

@antpalkin More like finance bros enjoying watching retail increase their volume with slop ideas

English

every finance bro reading this realizing their $650k desk job just got cooked by a text box a guy runs from his couch for $99

cvxv666@antpalkin

"Long oil the second Trump says something bad about Iran" Someone typed that into an AI agent. It pulled the data, wrote the code, ran a 10-year backtest, and shipped it live to their broker. Minutes. Every trader has an idea like that rotting in their head - never tested, because coding it wasn't worth a weekend. One that got typed in: buy stocks that gap up 2%, hold 30 days. Backtest came back +562%, profit factor 3.27. One click, live on Alpaca. The $650k quant job, now a text box. First 10,000 traders. Go type the idea you've been sitting on for two years. Demo's below.

English

@PlusEVAnalytics Yes completely agree. They either are being deliberately disingenuous or they are outing themselves as total casual non-traders (and non-businesspeople)

English

PM people *love* talking like this. Here's the problem...they correctly list all kinds of examples where a business's revenue is correlated with a sporting event outcome. But that's not the correct trigger for a hedge transaction, because such transactions aren't free. You pay taker fees plus a bid/ask spread. PM hedges are much more expensive than hedges using stock markets or commodity futures. Businesses don't like to incur extra costs for no reason.

The correct trigger for a hedge transaction should be *significant* financial risk. As in, one game result swinging you between healthy profits and trouble paying your bills. Filtered this way, the set of use cases shrinks substantially.

I think deep down everyone knows this, and accepts that the only sustainable use case is as a substitute for sports betting, either a better mousetrap and/or a regulatory workaround depending on your point of view.

Aggie@BlondiePredicts

I must admit, when I first got into prediction markets, I wasn't too excited about sports markets (due to gambling concerns) so I was focused on event contracts for culture, economics, and financial events. (I did trade a few tennis markets for fun, as a former tennis player I think I have an edge.) It took me a while to realize that sports prediction markets are MUCH BIGGER than ‘’just for fun’’. They're a proper tool for hedging risk (for those who take it seriously). Think weather, playoff revenue, sponsorships, broadcasters, airlines, hotels, merchandise manufacturers, and countless other businesses whose revenues depend on sporting outcomes. So the opportunity isn't just millions of sports fans. It's institutions managing BILLIONS in exposure. We have heard about the sports bar offering free drinks if the Knicks win (and hedging that risk with prediction markets), but what other unexpected businesses could benefit from sports prediction markets?

English

@boazweinstein They’ll be directly behind the royal box or on the opposite side with a straight on view. Like being on 50yd like in football 👍

English

Given the 8 second TV delay, looking in the crowd for the Susquehanna and Jane St co-located traders!

English

@liquidatedxxx I think if you have an informational advantage you prefer liquidity (kalshi) and anonymity (Kalshi). That being said, jurisdiction is most important if you have informational advantage, as you are likely to be scrutinized

English

Generally speaking, I think traders with an informational advantage prefer Polymarket over Kalshi.

Which is very telling that for the same Maine Senate Nomination market, Troy Jackson trades for 70% on Polymarket and only 64-66% on Kalshi.

It's just not a thin orderbook, people are definitely willing to overpay on Polymarket for some reason.

I think who gets nominated depends heavily on how the county caucus/state convention will work. There are just too many cooks in the kitchen to keep the whole process a secret.

I could be wrong but it is an interesting phenomenon.

(btw Kalshi is so serious about insider trading/KYC that I almost got myself banned over a Platner insider joke and was threatened to remove it LOL)

English

@exec_sum Anyone with half a brain and any experience in finance AND prediction markets knows that no one (sig included) is hedging real financial exposure with World Cup outcomes

English

BREAKING: Quant trading firm Susquehanna committed $500M to hedge World Cup outcomes via prediction markets

For context, Morgan Stanley is forecasting a dent in Latin American beer sales from Brazil and Mexico's exits and SIG is looking to capitalize on such trends by selling brands insurance/hedges against upsets

English

@Rishibets Yes it happens frequently. But the $ account amount doesn’t change, so I just use that

English

Anyone else have this glitch where Kalshi tells you your portfolio is down a massive amount when it isn't? Not a joke tweet, real question. Says my portfolio is down 38% but it's up over the last day and week. And it's mostly cash not positions so can't be just position value

English

@evan_semet Do you think there’s actually enough liquidity in these 5m markets to hedge a btc buy (for example) that will have meaningful market impact?

English

anytime you place a trade, you will have some nonzero market impact which can have cascading effects to other markets that you are trading in, but who is to say what a “legitimate” delta view is for bitcoin? Is any one theory of BTC fundamentals (whatever that means lol) more real than another? I would argue no.

there’s nothing illegal about owning both the underlying and the derivative.

furthermore, these short term binaries are actually an amazing hedge for slippage. if you are going to buy a ton of BTC for some longer macro thesis, then like yeah you are positively exposed to the price of BTC, but actually in the short term you are kinda sad if the price of BTC spikes as you buy up since that means your DCA is quite bad. in that case, you want to have some additional short term positive exposure (which can be monetized) to the price of BTC to mitigate the loss from said slippage.

hedging is allowed, and slippage is a very real thing that people want to hedge against. obviously buying up BTC changes the odds of this side bet of paying out, but this is a very legitimate hedging use case, and idk some other mms that are too incompetent to model out flow are going to get burned, but that’s kind of a skill issue on their part imho.

Ruizhe Jia@RuizheJia

Binance is arguably the world's largest crypto exchange. Feb 2026: Polymarket lists a small 5-minute Bitcoin contract. Since then, Binance order flow spikes in the final seconds before settlement; prices revert soon after. New paper with David Dai and Shihao Yu ( @ShihaoY ): Settlement Manipulation in Prediction Markets (papers.ssrn.com/sol3/papers.cf…)🧵 The finding, up front: Traders push Bitcoin's price in the final seconds to decide the contract. That push makes the price less informative, yet Bitcoin's market more liquid. Market makers are largely insulated; ordinary traders lose $7.6M in two months.

English